Das könnte Ihnen auch gefallen

- MODULE 6 - Audit PlanningDokument9 SeitenMODULE 6 - Audit PlanningRufina B VerdeNoch keine Bewertungen

- AC19 MODULE 5 - UpdatedDokument14 SeitenAC19 MODULE 5 - UpdatedMaricar PinedaNoch keine Bewertungen

- PSA 210 & 700 Audit Engagement TermsDokument17 SeitenPSA 210 & 700 Audit Engagement TermsMichelle de Guzman100% (1)

- Activity 4Dokument12 SeitenActivity 4Beatrice Ella DomingoNoch keine Bewertungen

- Planning Audit Risk AssessmentDokument8 SeitenPlanning Audit Risk AssessmentCiel ArvenNoch keine Bewertungen

- What Is The General Objective of Planning For An Audit?Dokument6 SeitenWhat Is The General Objective of Planning For An Audit?Chris JacksonNoch keine Bewertungen

- Plan and audit financial statementsDokument2 SeitenPlan and audit financial statementsbobo kaNoch keine Bewertungen

- Planning An Audit Of Financial Statements (ISA 300Dokument11 SeitenPlanning An Audit Of Financial Statements (ISA 300Khurram RashidNoch keine Bewertungen

- Unit IV Audit PlanningDokument24 SeitenUnit IV Audit PlanningMark GerwinNoch keine Bewertungen

- Reviewer Sa AuditDokument6 SeitenReviewer Sa Auditprincess manlangitNoch keine Bewertungen

- CH 2Dokument25 SeitenCH 2Harsh DaneNoch keine Bewertungen

- Module 6: Audit PlanningDokument15 SeitenModule 6: Audit PlanningMAG MAGNoch keine Bewertungen

- Audting Chapter4Dokument12 SeitenAudting Chapter4Getachew JoriyeNoch keine Bewertungen

- E BookDokument5 SeitenE BookSavit BansalNoch keine Bewertungen

- What Is The General Objective of Planning For An Audit?Dokument2 SeitenWhat Is The General Objective of Planning For An Audit?FuturamaramaNoch keine Bewertungen

- PSA 300 SummaryDokument3 SeitenPSA 300 SummaryAnonymous CH1RGj6h100% (1)

- At 05 - Auditor PlanningDokument8 SeitenAt 05 - Auditor PlanningRei-Anne ReaNoch keine Bewertungen

- Planning and Risk AssessmentDokument13 SeitenPlanning and Risk AssessmentLakmal KaushalyaNoch keine Bewertungen

- C2 Inter AuditDokument8 SeitenC2 Inter Auditbroabhi143Noch keine Bewertungen

- AT 05 Planning An Audit of FS and PSA 315Dokument4 SeitenAT 05 Planning An Audit of FS and PSA 315Princess Mary Joy LadagaNoch keine Bewertungen

- Lecture 3 Audit Planning and Internal ControlDokument20 SeitenLecture 3 Audit Planning and Internal ControlKaran RawatNoch keine Bewertungen

- Audit Planning AnswersDokument3 SeitenAudit Planning AnswersKathlene BalicoNoch keine Bewertungen

- CHAPTER5Dokument8 SeitenCHAPTER5Anjelika ViescaNoch keine Bewertungen

- Prepare an Audit Plan Before Commencing an AuditDokument27 SeitenPrepare an Audit Plan Before Commencing an AuditPrathyusha KorukuriNoch keine Bewertungen

- Stages of An AuditDokument4 SeitenStages of An AuditDerrick KimaniNoch keine Bewertungen

- Planning an Audit of Financial StatementsDokument8 SeitenPlanning an Audit of Financial StatementsVito CorleonNoch keine Bewertungen

- Chapter+7 Audit+PlanningDokument20 SeitenChapter+7 Audit+Planningmohazka hassanNoch keine Bewertungen

- Auditing Theory Review HO4: Psa 300 (Rev.) Planning An Audit of Financial Statements PSA 315Dokument4 SeitenAuditing Theory Review HO4: Psa 300 (Rev.) Planning An Audit of Financial Statements PSA 315Leigh GaranchonNoch keine Bewertungen

- Auditing Notes by Rehan Farhat ISA 300Dokument21 SeitenAuditing Notes by Rehan Farhat ISA 300Omar SiddiquiNoch keine Bewertungen

- Chapter 2 Risk Assessments and Internal ControlDokument16 SeitenChapter 2 Risk Assessments and Internal ControlSteffany RoqueNoch keine Bewertungen

- Ca Audit 2023 Unit IiDokument11 SeitenCa Audit 2023 Unit IiAntrew B2Noch keine Bewertungen

- The Audit ProcessDokument20 SeitenThe Audit ProcessmavhikalucksonprofaccNoch keine Bewertungen

- Lesson 5 Audit Planning and Audit RiskDokument13 SeitenLesson 5 Audit Planning and Audit Riskwambualucas74Noch keine Bewertungen

- Audit Strategy, Audit Planning and Audit Programme: Learning OutcomesDokument31 SeitenAudit Strategy, Audit Planning and Audit Programme: Learning OutcomesMayank JainNoch keine Bewertungen

- Review Notes On PSA 2Dokument9 SeitenReview Notes On PSA 2Barbie Saniel RamonesNoch keine Bewertungen

- Isa 300Dokument5 SeitenIsa 300sabeen ansariNoch keine Bewertungen

- Auditing Theory: Audit Planning: An OverviewDokument31 SeitenAuditing Theory: Audit Planning: An OverviewChristine NionesNoch keine Bewertungen

- At.1609 - Audit Planning - An OverviewDokument6 SeitenAt.1609 - Audit Planning - An Overviewnaztig_017Noch keine Bewertungen

- 04 Audit Planning and Risk AssessmentDokument12 Seiten04 Audit Planning and Risk AssessmentaibsNoch keine Bewertungen

- Project On Audit Plan and Programme & Special AuditDokument11 SeitenProject On Audit Plan and Programme & Special AuditPriyank SolankiNoch keine Bewertungen

- (At) 03 PlanningDokument14 Seiten(At) 03 PlanningCykee Hanna Quizo LumongsodNoch keine Bewertungen

- A. Purpose For Planning The EngagementDokument5 SeitenA. Purpose For Planning The EngagementJaniña Natividad100% (2)

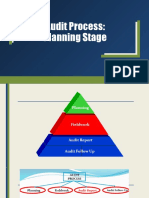

- Audit Process: Planning StageDokument25 SeitenAudit Process: Planning StageNelsie Grace PinedaNoch keine Bewertungen

- Audit ManualDokument80 SeitenAudit ManualhaninadiaNoch keine Bewertungen

- At Handouts 3Dokument18 SeitenAt Handouts 3Jake MandapNoch keine Bewertungen

- Hane G. Minasalbas Bsa 3Dokument2 SeitenHane G. Minasalbas Bsa 3Hane MinasalbasNoch keine Bewertungen

- IPCC Auditing Chapter II: Audit Strategy, Planning and ProgrammeDokument8 SeitenIPCC Auditing Chapter II: Audit Strategy, Planning and ProgrammeAlphy maria cherianNoch keine Bewertungen

- Objective of Audit PlanningDokument5 SeitenObjective of Audit PlanningJan Michael MirasolNoch keine Bewertungen

- Audit Planning ProcessDokument7 SeitenAudit Planning ProcessDelelegn AyalikeNoch keine Bewertungen

- Audit Planning & Documentation - Taxguru - inDokument8 SeitenAudit Planning & Documentation - Taxguru - inNino NakanoNoch keine Bewertungen

- Statement of Auditing StandardsDokument2 SeitenStatement of Auditing StandardsMikaela SalvadorNoch keine Bewertungen

- LESSON 5 - THE AUDIT PROCESS-Planning and Quality ControlDokument7 SeitenLESSON 5 - THE AUDIT PROCESS-Planning and Quality Controlkipngetich392100% (1)

- Auditing Planning Chapt 3Dokument8 SeitenAuditing Planning Chapt 3bhumika aggarwalNoch keine Bewertungen

- M6 - Audit Planning, Supervision, and MonitoringDokument8 SeitenM6 - Audit Planning, Supervision, and MonitoringAlain CopperNoch keine Bewertungen

- Audit Planning GuideDokument9 SeitenAudit Planning GuidegumiNoch keine Bewertungen

- Chapter No.2 OkDokument14 SeitenChapter No.2 OkRajshahi BoardNoch keine Bewertungen

- Comparison ChartDokument3 SeitenComparison ChartzenellebellaNoch keine Bewertungen

- Chap.3 Audit Plannng, Working Paper and Internal Control-1Dokument10 SeitenChap.3 Audit Plannng, Working Paper and Internal Control-1Himanshu MoreNoch keine Bewertungen

- Audit PlanningDokument16 SeitenAudit PlanningAnnieka PascualNoch keine Bewertungen

- Audit Risk Alert: Employee Benefit Plans Industry Developments, 2018Von EverandAudit Risk Alert: Employee Benefit Plans Industry Developments, 2018Noch keine Bewertungen

- Ty Btech syllabusIT Revision 2015 19 14june17 - withHSMC - 1 PDFDokument85 SeitenTy Btech syllabusIT Revision 2015 19 14june17 - withHSMC - 1 PDFMusadiqNoch keine Bewertungen

- ElasticityDokument27 SeitenElasticityJames Baryl GarceloNoch keine Bewertungen

- Intangible Capital: Key Factor of Sustainable Development in MoroccoDokument8 SeitenIntangible Capital: Key Factor of Sustainable Development in MoroccojournalNoch keine Bewertungen

- QUIZ - FinalsDokument5 SeitenQUIZ - FinalsFelsie Jane PenasoNoch keine Bewertungen

- Jabiru Inc S Senior Management Recently Obtained A New Decision Support DatabaseDokument1 SeiteJabiru Inc S Senior Management Recently Obtained A New Decision Support DatabaseDoreenNoch keine Bewertungen

- Vda. de Consuegra v. Government Service Insurance System (1971)Dokument1 SeiteVda. de Consuegra v. Government Service Insurance System (1971)Andre Philippe RamosNoch keine Bewertungen

- Certificate of IncorporationDokument1 SeiteCertificate of IncorporationVaseem ChauhanNoch keine Bewertungen

- Why The Bollard Pull Calculation Method For A Barge Won't Work For A Ship - TheNavalArchDokument17 SeitenWhy The Bollard Pull Calculation Method For A Barge Won't Work For A Ship - TheNavalArchFederico BabichNoch keine Bewertungen

- Breakdown Maintenance in SAP Asset ManagementDokument11 SeitenBreakdown Maintenance in SAP Asset ManagementHala TAMIMENoch keine Bewertungen

- Expressing Interest in NIBAV LiftsDokument9 SeitenExpressing Interest in NIBAV LiftsSetiawan RustandiNoch keine Bewertungen

- Speech ExamplesDokument6 SeitenSpeech Examplesjayz_mateo9762100% (1)

- A Case Study On Design of Ring Footing For Oil Storage Steel TankDokument6 SeitenA Case Study On Design of Ring Footing For Oil Storage Steel Tankknight1729Noch keine Bewertungen

- Ultrasonic Pulse Velocity or Rebound MeasurementDokument2 SeitenUltrasonic Pulse Velocity or Rebound MeasurementCristina CastilloNoch keine Bewertungen

- Comparison Between India and ChinaDokument92 SeitenComparison Between India and Chinaapi-3710029100% (3)

- E No Ad Release NotesDokument6 SeitenE No Ad Release NotesKostyantinBondarenkoNoch keine Bewertungen

- The Bedford Clanger May 2013 (The Beer Issue)Dokument12 SeitenThe Bedford Clanger May 2013 (The Beer Issue)Erica RoffeNoch keine Bewertungen

- 2.2 Access CT Networking Rev20150728Dokument5 Seiten2.2 Access CT Networking Rev20150728F CNoch keine Bewertungen

- Saurabh Pandey - Management Trainee - Recruitment - 5 Yrs 10 MonthsDokument2 SeitenSaurabh Pandey - Management Trainee - Recruitment - 5 Yrs 10 MonthsDevraj GurjjarNoch keine Bewertungen

- Long Vowel SoundsDokument15 SeitenLong Vowel SoundsRoselle Jane PasquinNoch keine Bewertungen

- Pe 1997 01Dokument108 SeitenPe 1997 01franciscocampoverde8224Noch keine Bewertungen

- Affidavit in Support of ComplaintDokument3 SeitenAffidavit in Support of ComplaintTrevor DrewNoch keine Bewertungen

- Final Eligible Voters List North Zone 2017 118 1Dokument12 SeitenFinal Eligible Voters List North Zone 2017 118 1Bilal AhmedNoch keine Bewertungen

- Memorandum of AgreementDokument4 SeitenMemorandum of AgreementMarvel FelicityNoch keine Bewertungen

- FSK Demodulator With PLLDokument5 SeitenFSK Demodulator With PLLHema100% (1)

- Manufacturing of Turbo GenratorsDokument27 SeitenManufacturing of Turbo Genratorspavan6754Noch keine Bewertungen

- List of Yale University GraduatesDokument158 SeitenList of Yale University GraduatesWilliam Litynski100% (1)

- Advance NewsletterDokument14 SeitenAdvance Newsletterapi-206881299Noch keine Bewertungen

- Valuing Common and Preferred SharesDokument31 SeitenValuing Common and Preferred SharesAdam Mo AliNoch keine Bewertungen

- Fmi-Hd BR PDFDokument16 SeitenFmi-Hd BR PDFmin thantNoch keine Bewertungen

- DATEM Capture For AutoCADDokument195 SeitenDATEM Capture For AutoCADmanuelNoch keine Bewertungen