Das könnte Ihnen auch gefallen

- EWI Q2-2019 ResultsDokument27 SeitenEWI Q2-2019 ResultskimNoch keine Bewertungen

- EWI Q2-2018 ResultsDokument20 SeitenEWI Q2-2018 ResultskimNoch keine Bewertungen

- Eco World International Berhad (Company No: 1059850-A) (Incorporated in Malaysia)Dokument24 SeitenEco World International Berhad (Company No: 1059850-A) (Incorporated in Malaysia)kimNoch keine Bewertungen

- 5657 Parkson QR 2020-12-31 PHB-2021Q2 - 1014898452Dokument14 Seiten5657 Parkson QR 2020-12-31 PHB-2021Q2 - 1014898452Tengku Ajmal (Thunder)Noch keine Bewertungen

- Interim Results For The Six Months Ended 30 June 2020: Chairman'S StatementDokument24 SeitenInterim Results For The Six Months Ended 30 June 2020: Chairman'S Statementin resNoch keine Bewertungen

- Glomac Berhad: (Incorporated in Malaysia)Dokument8 SeitenGlomac Berhad: (Incorporated in Malaysia)Shungchau WongNoch keine Bewertungen

- Renuka Foods PLC: Interim Financial Statements - For The Period Ended 31 December 2021Dokument11 SeitenRenuka Foods PLC: Interim Financial Statements - For The Period Ended 31 December 2021hvalolaNoch keine Bewertungen

- EWIB - Q1-2018 ResultsDokument18 SeitenEWIB - Q1-2018 ResultskimNoch keine Bewertungen

- Guorui Properties Limited 國瑞置業有限公司: Interim Results Announcement For The Six Months Ended June 30, 2020Dokument38 SeitenGuorui Properties Limited 國瑞置業有限公司: Interim Results Announcement For The Six Months Ended June 30, 2020in resNoch keine Bewertungen

- Announcement of Interim Results For The Six Months Ended 30 June 2020Dokument19 SeitenAnnouncement of Interim Results For The Six Months Ended 30 June 2020in resNoch keine Bewertungen

- Q1 2023 Puma Energy Results ReportDokument11 SeitenQ1 2023 Puma Energy Results ReportKA-11 Єфіменко ІванNoch keine Bewertungen

- Iris Corporation Berhad: Interim Financial Report For The Fourth Quarter Ended 31 March 2018Dokument26 SeitenIris Corporation Berhad: Interim Financial Report For The Fourth Quarter Ended 31 March 2018Myeo HudsonNoch keine Bewertungen

- 0202 - RGTECH - QR - 2020-12-31 - Radiant Globaltech Berhad - Quarterly Results - 31.12.2020 - 670632592Dokument20 Seiten0202 - RGTECH - QR - 2020-12-31 - Radiant Globaltech Berhad - Quarterly Results - 31.12.2020 - 670632592Iqbal YusufNoch keine Bewertungen

- 5210 - ARMADA - QR - 2018-12-31 - Bumi Armada Q4 2018 - Quarterly Report - 638583370Dokument32 Seiten5210 - ARMADA - QR - 2018-12-31 - Bumi Armada Q4 2018 - Quarterly Report - 638583370Chee Meng TeowNoch keine Bewertungen

- Sapnrg-Fs q4 31 Jan 2023Dokument33 SeitenSapnrg-Fs q4 31 Jan 2023Mohd Faizal Mohd IbrahimNoch keine Bewertungen

- DRB HICOM Berhad Interim Report 31 December 2020 1Dokument30 SeitenDRB HICOM Berhad Interim Report 31 December 2020 1hayatiammadNoch keine Bewertungen

- Rmh Holdings Limited 德 斯 控 股 有 限 公 司Dokument37 SeitenRmh Holdings Limited 德 斯 控 股 有 限 公 司aalalalNoch keine Bewertungen

- Unaudited Interim Results For The Six Months Ended 30 June 2020Dokument27 SeitenUnaudited Interim Results For The Six Months Ended 30 June 2020in resNoch keine Bewertungen

- Q4 2022 Bursa Announcement - 2Dokument13 SeitenQ4 2022 Bursa Announcement - 2Quint WongNoch keine Bewertungen

- INTERIM REPORT YA2021 QUARTER 1 (01 AUG 2020 Until 31 OCT 2020)Dokument15 SeitenINTERIM REPORT YA2021 QUARTER 1 (01 AUG 2020 Until 31 OCT 2020)pes myNoch keine Bewertungen

- Imperial Pacific International Holdings Limited: Interim Results For The Six Months Ended 30 June 2020Dokument26 SeitenImperial Pacific International Holdings Limited: Interim Results For The Six Months Ended 30 June 2020in resNoch keine Bewertungen

- PMCORP QR 30 June 2022Dokument12 SeitenPMCORP QR 30 June 2022zul hakifNoch keine Bewertungen

- EWM Results - 3Q 2019Dokument24 SeitenEWM Results - 3Q 2019kimNoch keine Bewertungen

- GAR02 28 02 2024 FY2023 Results ReleaseDokument29 SeitenGAR02 28 02 2024 FY2023 Results Releasedesifatimah87Noch keine Bewertungen

- INTERIM REPORT YA2022 QUARTER 1 (01 AUG 2021 Until 31 OCT 2021)Dokument15 SeitenINTERIM REPORT YA2022 QUARTER 1 (01 AUG 2021 Until 31 OCT 2021)pes myNoch keine Bewertungen

- A04 Xgpr15n5xduon8yb.1Dokument30 SeitenA04 Xgpr15n5xduon8yb.1Hiya ByeNoch keine Bewertungen

- Superlon Holdings Berhad (Incorporated in Malaysia)Dokument12 SeitenSuperlon Holdings Berhad (Incorporated in Malaysia)Gan ZhiHanNoch keine Bewertungen

- INTERIM REPORT YA2021 QUARTER 4 (01 MAY 2021 Until 31 JUL 2021)Dokument16 SeitenINTERIM REPORT YA2021 QUARTER 4 (01 MAY 2021 Until 31 JUL 2021)pes myNoch keine Bewertungen

- DPIH - 4Q Results FYE2022 - 20220531Dokument24 SeitenDPIH - 4Q Results FYE2022 - 20220531家星Noch keine Bewertungen

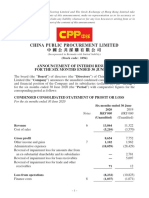

- China Public Procurement Limited 中 國 公 共 採 購 有 限 公 司Dokument37 SeitenChina Public Procurement Limited 中 國 公 共 採 購 有 限 公 司in resNoch keine Bewertungen

- Unaudited Condensed Consolidated Income Statement: Misc BerhadDokument20 SeitenUnaudited Condensed Consolidated Income Statement: Misc BerhadAzizi JaisNoch keine Bewertungen

- Cocoaland Holdings Berhad: (Incorporated in Malaysia)Dokument15 SeitenCocoaland Holdings Berhad: (Incorporated in Malaysia)Sajeetha MadhavanNoch keine Bewertungen

- Financial Results EWM 1Q 2024Dokument18 SeitenFinancial Results EWM 1Q 2024Najib SaadNoch keine Bewertungen

- Emaar Consolidated EAS Dec 20 English FSsDokument38 SeitenEmaar Consolidated EAS Dec 20 English FSsAly A. SamyNoch keine Bewertungen

- ZHI Announcement - 1H 2020Dokument25 SeitenZHI Announcement - 1H 2020Kang Xian WongNoch keine Bewertungen

- Careplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomeDokument16 SeitenCareplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomethamNoch keine Bewertungen

- Announcement of Interim Results For The Six Months Ended 30 June 2020Dokument45 SeitenAnnouncement of Interim Results For The Six Months Ended 30 June 2020in resNoch keine Bewertungen

- Apollo Ar19Dokument72 SeitenApollo Ar19Wen Xin GanNoch keine Bewertungen

- INTERIM REPORT YA2021 QUARTER 2 (01 NOV 2020 Until 31 JAN 2021)Dokument15 SeitenINTERIM REPORT YA2021 QUARTER 2 (01 NOV 2020 Until 31 JAN 2021)pes myNoch keine Bewertungen

- PPBInt RPT 2003Dokument15 SeitenPPBInt RPT 2003Gan ZhiHanNoch keine Bewertungen

- Bangladesh q3 Report 2020 Tcm244 556009 enDokument8 SeitenBangladesh q3 Report 2020 Tcm244 556009 entdebnath_3Noch keine Bewertungen

- Half Year Financial Statement and Dividend AnnouncementDokument16 SeitenHalf Year Financial Statement and Dividend AnnouncementKennardNoch keine Bewertungen

- CHB Sep19 PDFDokument14 SeitenCHB Sep19 PDFSajeetha MadhavanNoch keine Bewertungen

- Annual: Etfx Uk Group LLCDokument70 SeitenAnnual: Etfx Uk Group LLCeliasNoch keine Bewertungen

- MR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Dokument15 SeitenMR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Mzm Zahir MzmNoch keine Bewertungen

- Techna-X Berhad: Incorporated in MalaysiaDokument17 SeitenTechna-X Berhad: Incorporated in MalaysiaChoon Wei WongNoch keine Bewertungen

- Bursa Announcement DIYQ12022Dokument13 SeitenBursa Announcement DIYQ12022Quint WongNoch keine Bewertungen

- Airasia Quarter ReportDokument34 SeitenAirasia Quarter ReportChee Meng TeowNoch keine Bewertungen

- Adventa Sofp & Sopl 2021Dokument3 SeitenAdventa Sofp & Sopl 2021ariash mohdNoch keine Bewertungen

- Sofp, Sopl Adventa&uem 20-21Dokument14 SeitenSofp, Sopl Adventa&uem 20-21ariash mohdNoch keine Bewertungen

- FGV - Quarterly Report Q3 2018Dokument38 SeitenFGV - Quarterly Report Q3 2018Richard OonNoch keine Bewertungen

- 1Q 20 - Bursa (PMMA) FinalDokument12 Seiten1Q 20 - Bursa (PMMA) FinalGan ZhiHanNoch keine Bewertungen

- Characteristics of Gem of The Stock Exchange of Hong Kong Limited (The "Stock Exchange")Dokument23 SeitenCharacteristics of Gem of The Stock Exchange of Hong Kong Limited (The "Stock Exchange")DrNoch keine Bewertungen

- (A) Nature of Business of Cepatwawasan Group BerhadDokument16 Seiten(A) Nature of Business of Cepatwawasan Group BerhadTan Rou YingNoch keine Bewertungen

- Chin Hin - Quarter Announcement Q4 2021 (Final)Dokument31 SeitenChin Hin - Quarter Announcement Q4 2021 (Final)KentNoch keine Bewertungen

- ENX - URD2022 - Financial Statements and Auditors ReportDokument99 SeitenENX - URD2022 - Financial Statements and Auditors ReportRaghunathNoch keine Bewertungen

- CHB Jun19 PDFDokument14 SeitenCHB Jun19 PDFSajeetha MadhavanNoch keine Bewertungen

- Amsteel Corp 2 Q 06Dokument13 SeitenAmsteel Corp 2 Q 06amir amirahNoch keine Bewertungen

- Interim Financial Statement - 3rd Quarter: Aitken Spence Hotel Holdings PLCDokument16 SeitenInterim Financial Statement - 3rd Quarter: Aitken Spence Hotel Holdings PLCnowfazNoch keine Bewertungen

- List of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosVon EverandList of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosNoch keine Bewertungen

- SCB BursaAnnFSNotes 4th Quarter Ended 30.6.2022Dokument13 SeitenSCB BursaAnnFSNotes 4th Quarter Ended 30.6.2022kimNoch keine Bewertungen

- 2Q 2023 Bursa (PMMA)Dokument15 Seiten2Q 2023 Bursa (PMMA)kimNoch keine Bewertungen

- No Longer Available - Archive Entry: Product CharacteristicsDokument2 SeitenNo Longer Available - Archive Entry: Product CharacteristicskimNoch keine Bewertungen

- Investors Fiesta 2022 - Guaranteed Gift Winners' ListingDokument3 SeitenInvestors Fiesta 2022 - Guaranteed Gift Winners' ListingkimNoch keine Bewertungen

- Dräger REGARD 2400 / 2410: 4-Kanal GaswarnzentraleDokument34 SeitenDräger REGARD 2400 / 2410: 4-Kanal GaswarnzentralekimNoch keine Bewertungen

- Jtiasa Q1FY2018 ResultsDokument15 SeitenJtiasa Q1FY2018 ResultskimNoch keine Bewertungen

- Jtiasa 4Q 30 June 2017 Results PDFDokument13 SeitenJtiasa 4Q 30 June 2017 Results PDFkimNoch keine Bewertungen

- JTH - 3Q 31 Mar 2016 ResultsDokument12 SeitenJTH - 3Q 31 Mar 2016 ResultskimNoch keine Bewertungen

- Presentation 1QFY17Dokument42 SeitenPresentation 1QFY17kimNoch keine Bewertungen

- Jtiasa 1Q 30 June 2017 ResultsDokument11 SeitenJtiasa 1Q 30 June 2017 ResultskimNoch keine Bewertungen

- EWM Results - 1Q 2018Dokument16 SeitenEWM Results - 1Q 2018kimNoch keine Bewertungen

- Jtiasa 4Q 30 June 2016 ResultsDokument12 SeitenJtiasa 4Q 30 June 2016 ResultskimNoch keine Bewertungen

- EWIB - Q1-2018 ResultsDokument18 SeitenEWIB - Q1-2018 ResultskimNoch keine Bewertungen

- Eco World Development Group Berhad (Company No: 17777-V) (Incorporated in Malaysia)Dokument20 SeitenEco World Development Group Berhad (Company No: 17777-V) (Incorporated in Malaysia)kimNoch keine Bewertungen

- EWM Results - 1Q 2019Dokument22 SeitenEWM Results - 1Q 2019kimNoch keine Bewertungen

- EWM Results - 3Q 2019Dokument24 SeitenEWM Results - 3Q 2019kimNoch keine Bewertungen

- Eco World - Corporate Governance Report 2018Dokument49 SeitenEco World - Corporate Governance Report 2018kimNoch keine Bewertungen

- FRS 25Dokument13 SeitenFRS 25distratisgiuNoch keine Bewertungen

- IAS 18 Workshop RevisedDokument13 SeitenIAS 18 Workshop Revisedsohail merchantNoch keine Bewertungen

- M&a Twitter and Elon MuskDokument18 SeitenM&a Twitter and Elon MuskKosHanNoch keine Bewertungen

- SEC Form 23A JDG Yap 01.2021Dokument3 SeitenSEC Form 23A JDG Yap 01.2021Raine PiliinNoch keine Bewertungen

- Financial Statements MIS and Financial KPIsDokument67 SeitenFinancial Statements MIS and Financial KPIsDevanand TayadeNoch keine Bewertungen

- Section 35 Transition To The: Ifrs For SmesDokument35 SeitenSection 35 Transition To The: Ifrs For SmesAdenrele SalakoNoch keine Bewertungen

- Jan Mark Castillo - BSA 1 Chapter-6-Business-Transactions-And-Their-AnalysisDokument8 SeitenJan Mark Castillo - BSA 1 Chapter-6-Business-Transactions-And-Their-AnalysisJan Mark CastilloNoch keine Bewertungen

- Equity Securities Market Final05272023Dokument39 SeitenEquity Securities Market Final05272023Bea Bianca MadlaNoch keine Bewertungen

- Tata CorusDokument98 SeitenTata Corussandeepjaiswal2403Noch keine Bewertungen

- Air AsiaDokument8 SeitenAir AsiaKhai EmanNoch keine Bewertungen

- Michael Jackson Bill GatesDokument1 SeiteMichael Jackson Bill GatesThe WrapNoch keine Bewertungen

- Gemini ElectronicsDokument1 SeiteGemini ElectronicsSreeda PerikamanaNoch keine Bewertungen

- MBA MCI Case StudyDokument16 SeitenMBA MCI Case StudyThomas Innocenti50% (2)

- UntitledDokument7 SeitenUntitledMaharishi AguirreNoch keine Bewertungen

- Accts Imp QnsDokument4 SeitenAccts Imp QnsnishabilochiNoch keine Bewertungen

- Chap 3 MCQDokument30 SeitenChap 3 MCQchiukhohockhongsocucnhocNoch keine Bewertungen

- Chap 005Dokument8 SeitenChap 005Anass BNoch keine Bewertungen

- Instruction To Use This Worksheet: WWW - Screener.inDokument18 SeitenInstruction To Use This Worksheet: WWW - Screener.inRasulNoch keine Bewertungen

- Webinar PPT SMEspptxDokument34 SeitenWebinar PPT SMEspptxChristine Joyce MagoteNoch keine Bewertungen

- Real Estate Investment AnalysisDokument1 SeiteReal Estate Investment AnalysisJoelleCabasaNoch keine Bewertungen

- Fundamental of Corporate Finance, chpt2Dokument8 SeitenFundamental of Corporate Finance, chpt2YIN SOKHENGNoch keine Bewertungen

- Transnational CorporationsDokument6 SeitenTransnational CorporationsOty LyaNoch keine Bewertungen

- Wrong. The Correct Answer Is False.: You Answered Correctly!Dokument17 SeitenWrong. The Correct Answer Is False.: You Answered Correctly!Jem BalanoNoch keine Bewertungen

- PFRS 11-Joint ArrangementsDokument93 SeitenPFRS 11-Joint ArrangementsStephiel Sump100% (5)

- Unit 4 Discussion - Investment AppraisalDokument5 SeitenUnit 4 Discussion - Investment AppraisalMerlia KumdanaNoch keine Bewertungen

- ABM - BF12 IIIb 8Dokument4 SeitenABM - BF12 IIIb 8Raffy Jade SalazarNoch keine Bewertungen

- CFP Mock Test Investment PlanningDokument7 SeitenCFP Mock Test Investment PlanningDeep Shikha100% (4)

- Financial Engineering Class Sesi 1 Ver 2.0Dokument16 SeitenFinancial Engineering Class Sesi 1 Ver 2.0Davis FojemNoch keine Bewertungen

- Du Pont AnalysisDokument6 SeitenDu Pont AnalysisprashantNoch keine Bewertungen

- Comprehensive Income and EquityDokument2 SeitenComprehensive Income and EquityLouiseNoch keine Bewertungen