Das könnte Ihnen auch gefallen

- Letters of Credit and Documentary Collections: An Export and Import GuideVon EverandLetters of Credit and Documentary Collections: An Export and Import GuideBewertung: 1 von 5 Sternen1/5 (1)

- Discrepancies (Business Credit)Dokument7 SeitenDiscrepancies (Business Credit)Dr M R aggarwaalNoch keine Bewertungen

- Credit Restore Secrets They Never Wanted You to KnowVon EverandCredit Restore Secrets They Never Wanted You to KnowBewertung: 4 von 5 Sternen4/5 (3)

- Dealing With LC DiscrepanciesDokument6 SeitenDealing With LC Discrepanciesmahmudratul85Noch keine Bewertungen

- Letters of CreditDokument8 SeitenLetters of CreditCzarPaguioNoch keine Bewertungen

- Merc1 CaseDokument17 SeitenMerc1 CaseaypodNoch keine Bewertungen

- Letter of CreditDokument14 SeitenLetter of Creditswapnilnaik2001100% (1)

- KNJLKM LDokument23 SeitenKNJLKM LYrra LimchocNoch keine Bewertungen

- From A to UCP: Key Documentary Credit concepts explainedVon EverandFrom A to UCP: Key Documentary Credit concepts explainedNoch keine Bewertungen

- Letter of CreditDokument9 SeitenLetter of CreditPrith GajbhiyeNoch keine Bewertungen

- Letter of CreditDokument7 SeitenLetter of CreditprasadbpotdarNoch keine Bewertungen

- Letters of Credit in Banking Transactions by Severiano S. Tabios I. IntroductionDokument3 SeitenLetters of Credit in Banking Transactions by Severiano S. Tabios I. IntroductionMaisie ZabalaNoch keine Bewertungen

- Marx Notes - Special Commercial Laws (Divina) PDFDokument67 SeitenMarx Notes - Special Commercial Laws (Divina) PDFjica GulaNoch keine Bewertungen

- LOC CasesDokument60 SeitenLOC Casesi AcadsNoch keine Bewertungen

- Letter of CreditDokument19 SeitenLetter of CreditPrashant Pawar100% (1)

- Chapter 11Dokument29 SeitenChapter 11Yên LêNoch keine Bewertungen

- LOC and TR Primer UP 2001Dokument21 SeitenLOC and TR Primer UP 2001cathydavaoNoch keine Bewertungen

- Doctrine of Strict Compliance - MillarDokument18 SeitenDoctrine of Strict Compliance - MillarKiber TemesgenNoch keine Bewertungen

- How Does A Letter of Credit WorkDokument9 SeitenHow Does A Letter of Credit WorkAnju KumariNoch keine Bewertungen

- Letter of Credit - IB&FDokument10 SeitenLetter of Credit - IB&FRetika PunjabiNoch keine Bewertungen

- Bank of America v. CADokument19 SeitenBank of America v. CAMersheen RiriNoch keine Bewertungen

- To Break The ImpasseDokument10 SeitenTo Break The ImpassePS PngnbnNoch keine Bewertungen

- Letter of CreditDokument10 SeitenLetter of Creditmukesh12345678Noch keine Bewertungen

- Letter of CreditDokument7 SeitenLetter of CreditSujith S NairNoch keine Bewertungen

- Letter of CreditDokument34 SeitenLetter of CreditpweelengNoch keine Bewertungen

- Petitioner Respondents Agcaoili & Associates Valenzuela Law Center, Victor Fernandez Ramon M. GuevaraDokument15 SeitenPetitioner Respondents Agcaoili & Associates Valenzuela Law Center, Victor Fernandez Ramon M. GuevaraLiene Lalu NadongaNoch keine Bewertungen

- Assignment in Credit TransactionsDokument17 SeitenAssignment in Credit TransactionsNica09_forever100% (1)

- Letter of CreditDokument4 SeitenLetter of Creditrapols9100% (1)

- 2015 GN Mercantile Law - 27 July PDFDokument396 Seiten2015 GN Mercantile Law - 27 July PDFZyki Zamora LacdaoNoch keine Bewertungen

- Letters of CreditDokument2 SeitenLetters of CredityvonnebioyoNoch keine Bewertungen

- Trade Finance ManualDokument8 SeitenTrade Finance ManualgautamnarulaNoch keine Bewertungen

- Letter of CreditDokument10 SeitenLetter of Creditkhare_deepNoch keine Bewertungen

- Letter of Credit (LC)Dokument6 SeitenLetter of Credit (LC)giangnam45Noch keine Bewertungen

- De Leon - LeaseDokument7 SeitenDe Leon - LeaseGelo MVNoch keine Bewertungen

- Interview QuestionsDokument14 SeitenInterview QuestionsRohit AsthanaNoch keine Bewertungen

- Petitioner vs. vs. Respondents Agcaoili & Associates Valenzuela Law Center, Victor Fernandez Ramon M. GuevaraDokument14 SeitenPetitioner vs. vs. Respondents Agcaoili & Associates Valenzuela Law Center, Victor Fernandez Ramon M. Guevaraaspiringlawyer1234Noch keine Bewertungen

- 08 Bank of America vs. CADokument2 Seiten08 Bank of America vs. CALouise Bolivar DadivasNoch keine Bewertungen

- BANK OF AMERICA, NT & SA Vs CADokument10 SeitenBANK OF AMERICA, NT & SA Vs CAMaria VictoriaNoch keine Bewertungen

- Notes On Letter of CreditDokument6 SeitenNotes On Letter of Creditsandeepgawade100% (1)

- SPCL Case DigestsDokument107 SeitenSPCL Case DigestsMahaize TayawaNoch keine Bewertungen

- Trade Finance 1Dokument59 SeitenTrade Finance 1Mohiddin ghouseNoch keine Bewertungen

- 011 Bank of America V CADokument2 Seiten011 Bank of America V CAPatrick Manalo100% (1)

- LC DocsDokument5 SeitenLC DocsDeepak MishraNoch keine Bewertungen

- Letter of CreditDokument35 SeitenLetter of CreditYash AdukiaNoch keine Bewertungen

- NEGO - Letters of Credit - (3) Bank of America v. CA (228 SCRA 357)Dokument12 SeitenNEGO - Letters of Credit - (3) Bank of America v. CA (228 SCRA 357)Choi ChoiNoch keine Bewertungen

- Mercantile Law Bar QDokument106 SeitenMercantile Law Bar QMark Joseph DelimaNoch keine Bewertungen

- Chapter Three Modes of Payments in Foreign PurchasingDokument15 SeitenChapter Three Modes of Payments in Foreign PurchasingTariku AsmamawNoch keine Bewertungen

- Letters of CreditDokument25 SeitenLetters of Creditshamim1102100% (1)

- A Letter of Credit Is A Promise To PayDokument4 SeitenA Letter of Credit Is A Promise To PayJake Liboon100% (1)

- Letter of CreditDokument15 SeitenLetter of CreditudjosNoch keine Bewertungen

- Letter of Credit GuideDokument50 SeitenLetter of Credit GuideMohamed Naji100% (5)

- Letter of Credit1Dokument11 SeitenLetter of Credit1joshipathik18Noch keine Bewertungen

- Bank of America, NT & SA vs. Court of AppealDokument26 SeitenBank of America, NT & SA vs. Court of AppealNelNoch keine Bewertungen

- LTC Annotation 1Dokument4 SeitenLTC Annotation 1John Fredrick BucuNoch keine Bewertungen

- ProcurementDokument44 SeitenProcurementtahaNoch keine Bewertungen

- Supplier PerceptionDokument48 SeitenSupplier PerceptionsutomoNoch keine Bewertungen

- 70-2837B - Best Practice GuideDokument218 Seiten70-2837B - Best Practice GuideSamanway DasNoch keine Bewertungen

- Forwarder SRBDokument1 SeiteForwarder SRBsutomoNoch keine Bewertungen

- Freight Forwarding Legal Aspect SscribdDokument1 SeiteFreight Forwarding Legal Aspect SscribdsutomoNoch keine Bewertungen

- 1 WCOKARoOJuly2014Dokument60 Seiten1 WCOKARoOJuly2014sutomoNoch keine Bewertungen

- Understanding The Main Characteristics and Usage Understanding The Main Characteristics and UsageDokument7 SeitenUnderstanding The Main Characteristics and Usage Understanding The Main Characteristics and UsagesutomoNoch keine Bewertungen

- THCDokument1 SeiteTHCsutomoNoch keine Bewertungen

- Reliance General Insurance Company Limited: Reliance Two Wheeler Package Policy - ScheduleDokument6 SeitenReliance General Insurance Company Limited: Reliance Two Wheeler Package Policy - ScheduleJaya ChandranNoch keine Bewertungen

- Federal Taxpayer AgreementDokument10 SeitenFederal Taxpayer Agreementgordon scottNoch keine Bewertungen

- CT6 QP 0416Dokument6 SeitenCT6 QP 0416Shubham JainNoch keine Bewertungen

- Talent Management of Agency Managers in BHARTI AXADokument66 SeitenTalent Management of Agency Managers in BHARTI AXAfarazalam08Noch keine Bewertungen

- Accumulated Depreciation: EquipmentDokument9 SeitenAccumulated Depreciation: EquipmentAndrewVazNoch keine Bewertungen

- BOOKSHOPINHYDERABADDokument3 SeitenBOOKSHOPINHYDERABADakshayibsNoch keine Bewertungen

- Konnect SOBC - July To Dec 2022Dokument6 SeitenKonnect SOBC - July To Dec 2022Muhammad FawadNoch keine Bewertungen

- CV - Posriko Diegantera 2018 - EnglishDokument2 SeitenCV - Posriko Diegantera 2018 - EnglishShony ErdinalNoch keine Bewertungen

- FM LaDokument115 SeitenFM LaSamNoch keine Bewertungen

- Money, Banking, and FinanceDokument348 SeitenMoney, Banking, and Financeaveros12100% (4)

- Letter To The Governor, Reserve Bank of IndiaDokument209 SeitenLetter To The Governor, Reserve Bank of IndiaSivasubramanian Muthusamy100% (6)

- Assessing The Risk of Material Misstatement: Concept Checks P. 242Dokument23 SeitenAssessing The Risk of Material Misstatement: Concept Checks P. 242hsingting yuNoch keine Bewertungen

- Fee Information Document: General Account ServicesDokument7 SeitenFee Information Document: General Account Servicesdaryl30011996Noch keine Bewertungen

- RFP Process at GlanceDokument1 SeiteRFP Process at GlanceArpit KhandelwalNoch keine Bewertungen

- Intro To Aviation Ins (Fahamkan Je Tau)Dokument4 SeitenIntro To Aviation Ins (Fahamkan Je Tau)Anisah NiesNoch keine Bewertungen

- HR10J6570 - Acko Insurance Policy PDFDokument5 SeitenHR10J6570 - Acko Insurance Policy PDFRitesh KumarNoch keine Bewertungen

- Financial Advisory and Research of Mutual FundsDokument42 SeitenFinancial Advisory and Research of Mutual FundsJobin GeorgeNoch keine Bewertungen

- Aeb SM CH14 1Dokument28 SeitenAeb SM CH14 1fitriNoch keine Bewertungen

- Nifras CVDokument3 SeitenNifras CVmamzameer7Noch keine Bewertungen

- Global Ime Bank 2013Dokument34 SeitenGlobal Ime Bank 2013Keshab PandeyNoch keine Bewertungen

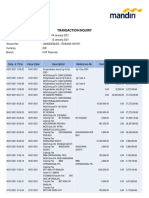

- Transaction Inquiry: Date & Time Value Date Description Debit Credit Reference No. SaldoDokument2 SeitenTransaction Inquiry: Date & Time Value Date Description Debit Credit Reference No. SaldoIntan BinalandNoch keine Bewertungen

- Credit Co-Operative SocietiesDokument31 SeitenCredit Co-Operative SocietiesGurpreet Singh Deol100% (1)

- Basic RHB User Guide FA2Dokument74 SeitenBasic RHB User Guide FA2Teoh Chee Tze50% (2)

- 2011 AFR LGUs Vol3ADokument475 Seiten2011 AFR LGUs Vol3ANom-de PlumeNoch keine Bewertungen

- Currency Futures and Options - FinalDokument107 SeitenCurrency Futures and Options - FinalRavindra BabuNoch keine Bewertungen

- Irr Ra 8291 PDFDokument110 SeitenIrr Ra 8291 PDFZannyRyanQuirozNoch keine Bewertungen

- Funds - Transfer V1 PDFDokument46 SeitenFunds - Transfer V1 PDFTanaka MachanaNoch keine Bewertungen

- Topic: Shinhan: Financial GroupDokument13 SeitenTopic: Shinhan: Financial GroupSabitkhattakNoch keine Bewertungen

- Febtc v. Gold PalaceDokument1 SeiteFebtc v. Gold PalaceKL NavNoch keine Bewertungen

- Fundamental Notes and Conceptual Problem of Journal Ledger Trial Balance and Cash BookDokument7 SeitenFundamental Notes and Conceptual Problem of Journal Ledger Trial Balance and Cash BookShekhar TNoch keine Bewertungen

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideVon Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideBewertung: 2.5 von 5 Sternen2.5/5 (2)

- A Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowVon EverandA Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowNoch keine Bewertungen

- Internal Audit Checklists: Guide to Effective AuditingVon EverandInternal Audit Checklists: Guide to Effective AuditingNoch keine Bewertungen

- Guide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyVon EverandGuide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyNoch keine Bewertungen

- Business Process Mapping: Improving Customer SatisfactionVon EverandBusiness Process Mapping: Improving Customer SatisfactionBewertung: 5 von 5 Sternen5/5 (1)

- Bribery and Corruption Casebook: The View from Under the TableVon EverandBribery and Corruption Casebook: The View from Under the TableNoch keine Bewertungen

- Frequently Asked Questions in International Standards on AuditingVon EverandFrequently Asked Questions in International Standards on AuditingBewertung: 1 von 5 Sternen1/5 (1)

- Financial Statement Fraud: Prevention and DetectionVon EverandFinancial Statement Fraud: Prevention and DetectionNoch keine Bewertungen

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekVon EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNoch keine Bewertungen

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersVon EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersBewertung: 4.5 von 5 Sternen4.5/5 (11)

- Financial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksVon EverandFinancial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksBewertung: 4 von 5 Sternen4/5 (1)

- Audit. Review. Compilation. What's the Difference?Von EverandAudit. Review. Compilation. What's the Difference?Bewertung: 5 von 5 Sternen5/5 (1)

- Scrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsVon EverandScrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsNoch keine Bewertungen

- The Layman's Guide GDPR Compliance for Small Medium BusinessVon EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessBewertung: 5 von 5 Sternen5/5 (1)

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceVon EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceBewertung: 4 von 5 Sternen4/5 (1)

- GDPR for DevOp(Sec) - The laws, Controls and solutionsVon EverandGDPR for DevOp(Sec) - The laws, Controls and solutionsBewertung: 5 von 5 Sternen5/5 (1)

- Audit and Assurance Essentials: For Professional Accountancy ExamsVon EverandAudit and Assurance Essentials: For Professional Accountancy ExamsNoch keine Bewertungen

- Musings on Internal Quality Audits: Having a Greater ImpactVon EverandMusings on Internal Quality Audits: Having a Greater ImpactNoch keine Bewertungen

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachVon EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachBewertung: 4 von 5 Sternen4/5 (1)