Das könnte Ihnen auch gefallen

- PT - Nutp 2014Dokument11 SeitenPT - Nutp 2014Akhila KanakapodiNoch keine Bewertungen

- Transport Economics: Topic: Nutp 2014 - Public TransportDokument11 SeitenTransport Economics: Topic: Nutp 2014 - Public TransportAkhila KanakapodiNoch keine Bewertungen

- BRT vs MRT/LRT: Comparing Project Costs and Service CoverageDokument2 SeitenBRT vs MRT/LRT: Comparing Project Costs and Service CoverageroslinekmatNoch keine Bewertungen

- Facing Challenge With TODDokument32 SeitenFacing Challenge With TODkhusnul hakimNoch keine Bewertungen

- DFCC Project Status OpportunitiesDokument34 SeitenDFCC Project Status OpportunitiesFaiyaz KhanNoch keine Bewertungen

- PPP Arrangements in Urban Transport - HMS and Gautam PatelDokument30 SeitenPPP Arrangements in Urban Transport - HMS and Gautam Patelnikki14156Noch keine Bewertungen

- India'S Internal Trade Infrastructure: - NAME: Nikita Kishan Kumar Das. APPLICATION NO.:211510003197Dokument6 SeitenIndia'S Internal Trade Infrastructure: - NAME: Nikita Kishan Kumar Das. APPLICATION NO.:211510003197Nikita DasNoch keine Bewertungen

- Transforming India's LogisticsDokument7 SeitenTransforming India's LogisticsmgmtNoch keine Bewertungen

- Rail Transport as Backbone of Efficient Multimodal NetworksDokument23 SeitenRail Transport as Backbone of Efficient Multimodal NetworksKendra TerryNoch keine Bewertungen

- Mayors Transit One PagerDokument2 SeitenMayors Transit One PagerJay King MindenNoch keine Bewertungen

- Dedicated Freight CorridorDokument8 SeitenDedicated Freight CorridorNirman DuttaNoch keine Bewertungen

- Transit Oriented - Resource PersonDokument45 SeitenTransit Oriented - Resource PersonSuvithaNoch keine Bewertungen

- BRT Project - Brief InfoDokument6 SeitenBRT Project - Brief InforutairengNoch keine Bewertungen

- Planning for efficient transit networksDokument11 SeitenPlanning for efficient transit networksSURYA NARAYANAN SNoch keine Bewertungen

- Urban Transport - How To Address The Commercial Road BlocksDokument20 SeitenUrban Transport - How To Address The Commercial Road BlocksBasant KumarNoch keine Bewertungen

- Railways - Brochure - For WebDokument9 SeitenRailways - Brochure - For WebSanyaNoch keine Bewertungen

- Deepak Upadhyay, Abhishek Tiwari, Praveen Mayer, Rohit Patel, Namrata VajpaiDokument21 SeitenDeepak Upadhyay, Abhishek Tiwari, Praveen Mayer, Rohit Patel, Namrata VajpaiAbhishek TiwariNoch keine Bewertungen

- India's Internal Trade Infrastructure: Pre-Induction Assignment 1Dokument6 SeitenIndia's Internal Trade Infrastructure: Pre-Induction Assignment 1anshulNoch keine Bewertungen

- DFCDokument12 SeitenDFCSulbha Mathur100% (1)

- Lifelines of National EconomyDokument13 SeitenLifelines of National Economychhayamaskare.3Noch keine Bewertungen

- Ch4-Operationa Based Railway PlanningDokument40 SeitenCh4-Operationa Based Railway PlanningMaalmalan KeekiyyaaNoch keine Bewertungen

- Mass Transit SystemDokument25 SeitenMass Transit SystemAmul ShresthaNoch keine Bewertungen

- Trade and Transport KZNDokument18 SeitenTrade and Transport KZNNomkhitha MinyaNoch keine Bewertungen

- DFC - Key Partner in Transportation: Biplav Kumar Group General ManagerDokument45 SeitenDFC - Key Partner in Transportation: Biplav Kumar Group General ManagerSiddi Ramulu100% (1)

- Lifelines of National Economy - Shobhit NirwanDokument10 SeitenLifelines of National Economy - Shobhit Nirwanalok nayakNoch keine Bewertungen

- Road Transport - India & Global: Group 1Dokument18 SeitenRoad Transport - India & Global: Group 1Su_NeilNoch keine Bewertungen

- Bus Rapid Transit System: Case Studies: at Dr. MCR HRDI, HyderabadDokument115 SeitenBus Rapid Transit System: Case Studies: at Dr. MCR HRDI, HyderabadsatishsajjaNoch keine Bewertungen

- LRT&MRTDokument12 SeitenLRT&MRTFathima jamalNoch keine Bewertungen

- Bus Rapid Transit System Case Study On Indore BRTS Route & Gaunghou, China BRTS RouteDokument18 SeitenBus Rapid Transit System Case Study On Indore BRTS Route & Gaunghou, China BRTS Routesimran deo100% (3)

- IR ReportDokument41 SeitenIR ReportNeel AsharNoch keine Bewertungen

- Light Rail TransitDokument17 SeitenLight Rail TransitAman singhNoch keine Bewertungen

- Updated Infrastructure and Urban Planning MatrixDokument4 SeitenUpdated Infrastructure and Urban Planning MatrixPhilip ONoch keine Bewertungen

- Light Rail Transit: An Efficient Urban Transport SolutionDokument16 SeitenLight Rail Transit: An Efficient Urban Transport Solutionmukunth eshwaranNoch keine Bewertungen

- MRTDokument38 SeitenMRTJigar Raval100% (1)

- Colombo Suburban Railway Project ; Transport Project Preparatory Facility 3425 SRIDokument43 SeitenColombo Suburban Railway Project ; Transport Project Preparatory Facility 3425 SRIManoj Thushara WimalarathneNoch keine Bewertungen

- Recommendations to boost EXIM cargo on RailDokument1 SeiteRecommendations to boost EXIM cargo on RailAmitNoch keine Bewertungen

- Bus Rapid Transit SystemDokument8 SeitenBus Rapid Transit SystemEkta AgarwalNoch keine Bewertungen

- Ahmedabad MetroDokument12 SeitenAhmedabad MetroMahima VaruNoch keine Bewertungen

- Transportation Engineering NotesDokument58 SeitenTransportation Engineering NotesAlyssa Marie AsuncionNoch keine Bewertungen

- Public - Information - Brochure - Feb2012 Dfccil Land Acquisition Process PDFDokument12 SeitenPublic - Information - Brochure - Feb2012 Dfccil Land Acquisition Process PDFmanish goyalNoch keine Bewertungen

- CementDokument6 SeitenCementSantosh DamaleNoch keine Bewertungen

- Policies On Railways InfrastructureDokument12 SeitenPolicies On Railways InfrastructureHighwayHoundNoch keine Bewertungen

- SWOT AnalysisDokument3 SeitenSWOT Analysisakhil-4108100% (5)

- Transportation Engineering I CE 304Dokument37 SeitenTransportation Engineering I CE 304Vibhanshu MishraNoch keine Bewertungen

- Transportation: PGDM (2019-21) : Term IVDokument32 SeitenTransportation: PGDM (2019-21) : Term IVaditya nemaNoch keine Bewertungen

- Nonfare Revenue MetroDokument26 SeitenNonfare Revenue MetroIshita P. VyasNoch keine Bewertungen

- Metro Public Transit Planning #2Dokument6 SeitenMetro Public Transit Planning #2nextSTL.comNoch keine Bewertungen

- Supply Chain Management of Coal in India: Veermata Jijabai Technological Institute, MatungaDokument25 SeitenSupply Chain Management of Coal in India: Veermata Jijabai Technological Institute, MatungaDipeshPatilNoch keine Bewertungen

- (A4) MORGONSZTREN - 2012 Transport Forum - Presentation GDSUTPDokument5 Seiten(A4) MORGONSZTREN - 2012 Transport Forum - Presentation GDSUTPAsian Development Bank ConferencesNoch keine Bewertungen

- Lifelines of National EconomyDokument8 SeitenLifelines of National EconomyNakshatra PaliwalNoch keine Bewertungen

- Railway Budget 2010-11 AnalysisDokument12 SeitenRailway Budget 2010-11 Analysisagrawalrohit_228384Noch keine Bewertungen

- Us Apid Ransit Ystem: B R T SDokument58 SeitenUs Apid Ransit Ystem: B R T SDivya VarshneyNoch keine Bewertungen

- 3 - G Raghuram-IIMDokument36 Seiten3 - G Raghuram-IIMPranshu JainNoch keine Bewertungen

- Assignment 1: Name: Ashwini A Palan Roll No. MH04010266 Appl. No. 211510005913Dokument6 SeitenAssignment 1: Name: Ashwini A Palan Roll No. MH04010266 Appl. No. 211510005913AshwiniNoch keine Bewertungen

- Project Identification ReportDokument269 SeitenProject Identification ReportnalakasaNoch keine Bewertungen

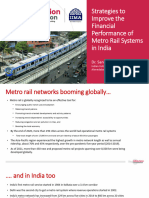

- Strategies To Improve Financial Performance of Metro Systems in IndiaDokument23 SeitenStrategies To Improve Financial Performance of Metro Systems in IndiaPayas GokhaleNoch keine Bewertungen

- CIVE 542 Lecture 5Dokument27 SeitenCIVE 542 Lecture 5Mervana MograbyNoch keine Bewertungen

- A Case Study of Janmarg BRTS, Ahmedabad, IndiaDokument18 SeitenA Case Study of Janmarg BRTS, Ahmedabad, IndiatarekyousryNoch keine Bewertungen

- Emily Johnson Milos Mladenovic SPT-E1020 Transport Systems Planning 14 December 2019 Assignment 4Dokument11 SeitenEmily Johnson Milos Mladenovic SPT-E1020 Transport Systems Planning 14 December 2019 Assignment 4Emily JohnsonNoch keine Bewertungen

- Transforming Cities with Transit: Transit and Land-Use Integration for Sustainable Urban DevelopmentVon EverandTransforming Cities with Transit: Transit and Land-Use Integration for Sustainable Urban DevelopmentBewertung: 3.5 von 5 Sternen3.5/5 (3)

- Formulation of BR Masterplan PDFDokument47 SeitenFormulation of BR Masterplan PDFCurious RajNoch keine Bewertungen

- Traffic Projection & Its BasisDokument12 SeitenTraffic Projection & Its BasisCurious RajNoch keine Bewertungen

- Assessment of Current SituationDokument12 SeitenAssessment of Current SituationCurious RajNoch keine Bewertungen

- Chapter43 PDFDokument20 SeitenChapter43 PDFyhproNoch keine Bewertungen

- Global Housing Competition RFPVol1Dokument201 SeitenGlobal Housing Competition RFPVol1Raman IyerNoch keine Bewertungen

- File On Indian Market PDFDokument53 SeitenFile On Indian Market PDFCurious RajNoch keine Bewertungen

- Work flow pre-project sanctioning ULBDokument2 SeitenWork flow pre-project sanctioning ULBishanhbmehtaNoch keine Bewertungen

- Steel Bridges - INSDAG PDFDokument15 SeitenSteel Bridges - INSDAG PDFsuman33Noch keine Bewertungen

- Urban Rail Transit SystemDokument3 SeitenUrban Rail Transit SystemCurious RajNoch keine Bewertungen

- Aws A5.9 PDFDokument42 SeitenAws A5.9 PDFAllen Roson75% (8)

- Planning and Designing of Bridge Over Solani RiverDokument5 SeitenPlanning and Designing of Bridge Over Solani RiverCurious RajNoch keine Bewertungen

- CBE Seminar Minutes 2018Dokument22 SeitenCBE Seminar Minutes 2018Curious RajNoch keine Bewertungen

- Loss - Income On Let Out House Property TemplateDokument2 SeitenLoss - Income On Let Out House Property TemplateCurious RajNoch keine Bewertungen

- p420 Structural Stainless Steel Design Tables 22 Nov 2017 With Watermark PDFDokument387 Seitenp420 Structural Stainless Steel Design Tables 22 Nov 2017 With Watermark PDFCurious RajNoch keine Bewertungen

- A1010 WeldingDokument20 SeitenA1010 WeldingCurious RajNoch keine Bewertungen

- Design Guide For Steel Railway Bridges: Sci Publication P318Dokument136 SeitenDesign Guide For Steel Railway Bridges: Sci Publication P318MarcoFranchinottiNoch keine Bewertungen

- Steel Structure Fabrication For RailwaysDokument192 SeitenSteel Structure Fabrication For RailwaysCurious RajNoch keine Bewertungen

- A Comparison of Structural Stainless Steel Design StandarDokument20 SeitenA Comparison of Structural Stainless Steel Design StandarLiviu IonNoch keine Bewertungen

- Financing of Rail Infrastructure Through State JVs - 1405Dokument70 SeitenFinancing of Rail Infrastructure Through State JVs - 1405Curious RajNoch keine Bewertungen

- IT Initiatives Transform Indian RailwaysDokument45 SeitenIT Initiatives Transform Indian RailwaysRobin Mukesh GuptaNoch keine Bewertungen

- Baddoo - EN Comparison of StandardsDokument4 SeitenBaddoo - EN Comparison of StandardsCurious RajNoch keine Bewertungen

- Detailed Lesson PlanDokument13 SeitenDetailed Lesson Plananamarie olaguerNoch keine Bewertungen

- QuestionnaireDokument3 SeitenQuestionnaireFatulousNoch keine Bewertungen

- Air Augmented Rocket (285pages) Propulsion ConceptsDokument285 SeitenAir Augmented Rocket (285pages) Propulsion ConceptsAlexandre PereiraNoch keine Bewertungen

- Course Offer 2020-2021 - Edito 2-1Dokument18 SeitenCourse Offer 2020-2021 - Edito 2-1Jessica Jeongah ChoiNoch keine Bewertungen

- Two Part QuestionDokument6 SeitenTwo Part QuestionMihaela GîdeiuNoch keine Bewertungen

- Starbucks: Is It A Discourse Community?Dokument9 SeitenStarbucks: Is It A Discourse Community?api-281150539Noch keine Bewertungen

- Class 10 History - Chapter 2: The Nationalist Movement in Indo-China Social ScienceDokument4 SeitenClass 10 History - Chapter 2: The Nationalist Movement in Indo-China Social ScienceParidhiNoch keine Bewertungen

- Indian MuslimsDokument12 SeitenIndian MuslimsNazeer AhmadNoch keine Bewertungen

- The African Charter On Human and Peoples' Rights: A Legal AnalysisDokument25 SeitenThe African Charter On Human and Peoples' Rights: A Legal AnalysisAkanksha SinghNoch keine Bewertungen

- Tatva SST Volume 1Dokument53 SeitenTatva SST Volume 1Farsin MuhammedNoch keine Bewertungen

- Homeroom Lesson Plan IntergrityDokument5 SeitenHomeroom Lesson Plan IntergrityIchaac VeracruzNoch keine Bewertungen

- Role of Trade Associations On Entrepreneurial DevelopmentDokument9 SeitenRole of Trade Associations On Entrepreneurial Developmentwanafrnd19Noch keine Bewertungen

- André Antoine's Passion for Realism in the Théâtre-LibreDokument31 SeitenAndré Antoine's Passion for Realism in the Théâtre-LibretibNoch keine Bewertungen

- Workbook: 7 Habits of Highly EffectiveDokument12 SeitenWorkbook: 7 Habits of Highly EffectiveStephanie UteschNoch keine Bewertungen

- Letter-to-MR NEIL V DALANON President Balud Municipal College Poblacion Balud MasbateDokument2 SeitenLetter-to-MR NEIL V DALANON President Balud Municipal College Poblacion Balud MasbateNeil DalanonNoch keine Bewertungen

- Project Report Format PDFDokument7 SeitenProject Report Format PDFPradhumna AdhikariNoch keine Bewertungen

- Hughes to Connect 5,000 Panchayats via ISRO SatellitesDokument2 SeitenHughes to Connect 5,000 Panchayats via ISRO SatellitesMEENA J RCBSNoch keine Bewertungen

- Cyberactivism and Citizen Journalism in Egypt Digital Dissidence and Political Change by Courtney C. Radsch (Auth.)Dokument364 SeitenCyberactivism and Citizen Journalism in Egypt Digital Dissidence and Political Change by Courtney C. Radsch (Auth.)gregmooooNoch keine Bewertungen

- Conveyancing and Its ImportanceDokument2 SeitenConveyancing and Its ImportanceElated TarantulaNoch keine Bewertungen

- Venice Art and ArchitectureDokument21 SeitenVenice Art and ArchitectureCora DragutNoch keine Bewertungen

- Bar Matter No DigestDokument5 SeitenBar Matter No DigestJia ChuaNoch keine Bewertungen

- Smart Classroom Management: Why You Should Ignore Difficult Students The First Week of SchoolDokument34 SeitenSmart Classroom Management: Why You Should Ignore Difficult Students The First Week of SchoolHansel VillasorNoch keine Bewertungen

- Pilgrim Case Sales Territory SplitDokument10 SeitenPilgrim Case Sales Territory SplitPaige LaurenNoch keine Bewertungen

- Cobing - Work Experience SheetDokument3 SeitenCobing - Work Experience SheetKatherine Herza CobingNoch keine Bewertungen

- Week-18 - New Kinder-Dll From New TG 2017Dokument8 SeitenWeek-18 - New Kinder-Dll From New TG 2017Marie banhaonNoch keine Bewertungen

- Women at 2021 - Final Print - (2021) - 3Dokument321 SeitenWomen at 2021 - Final Print - (2021) - 3Jitendra AhirraoNoch keine Bewertungen

- The No Child Left Behind Act of 2001-1Dokument23 SeitenThe No Child Left Behind Act of 2001-1api-503235879Noch keine Bewertungen

- Market Overview: Source: Mordor IntelligenceDokument6 SeitenMarket Overview: Source: Mordor IntelligenceNamit BaserNoch keine Bewertungen

- Civil War Vocab Lesson - Differentiated 2Dokument4 SeitenCivil War Vocab Lesson - Differentiated 2api-502287851Noch keine Bewertungen

- Conference Paper: Mustapha Mokhtari Gharbi Yacine Si LakhdarDokument21 SeitenConference Paper: Mustapha Mokhtari Gharbi Yacine Si LakhdarLamia Nour Ben abdelrahmenNoch keine Bewertungen