Das könnte Ihnen auch gefallen

- India's Growing FinTech EcosystemDokument69 SeitenIndia's Growing FinTech EcosystemGarvit Garg100% (1)

- IVCA Bain India VC Report 2018Dokument50 SeitenIVCA Bain India VC Report 2018ishan66666Noch keine Bewertungen

- Geo - India TechDokument41 SeitenGeo - India TechKaustubh SinghNoch keine Bewertungen

- NBFC SectorDokument23 SeitenNBFC Sectorpriya.sunder100% (2)

- Indian Banking in Next 5 Years - BCG ReportDokument17 SeitenIndian Banking in Next 5 Years - BCG ReportNirav ShahNoch keine Bewertungen

- Fintech 101 PDFDokument8 SeitenFintech 101 PDFjitenNoch keine Bewertungen

- Kalaari Logistics ReportDokument18 SeitenKalaari Logistics ReportNavin JollyNoch keine Bewertungen

- (ASTRA) Tantangan Digital Leadership Di Era Transformasi DigitalDokument10 Seiten(ASTRA) Tantangan Digital Leadership Di Era Transformasi DigitalSigit PoernomoNoch keine Bewertungen

- BCG ConsumatoreDokument37 SeitenBCG ConsumatoreAdriano ManiscalcoNoch keine Bewertungen

- Bain Digest India Venture Capital Report 2023Dokument45 SeitenBain Digest India Venture Capital Report 2023HarishNoch keine Bewertungen

- AgFunder Agrifood Tech Investing Report 2018Dokument60 SeitenAgFunder Agrifood Tech Investing Report 2018KritiNoch keine Bewertungen

- Map of Active VCs in Southeast AsiaDokument175 SeitenMap of Active VCs in Southeast AsiaAnonymous iA90mve4rNoch keine Bewertungen

- BCG Rai Report Retail Resurgence in IndiaDokument66 SeitenBCG Rai Report Retail Resurgence in IndiaakashNoch keine Bewertungen

- CSP Cost Roadmap We Finally Made It !Dokument20 SeitenCSP Cost Roadmap We Finally Made It !Emily7959Noch keine Bewertungen

- RealEstateTech TracxnFeedReport 07feb2020 - 1581314460268 PDFDokument228 SeitenRealEstateTech TracxnFeedReport 07feb2020 - 1581314460268 PDFRohan SanejaNoch keine Bewertungen

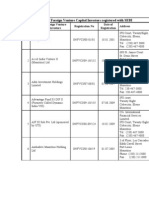

- A-List of Foreign Venture Capital Investors Registered With SEBIDokument24 SeitenA-List of Foreign Venture Capital Investors Registered With SEBIVipul ParekhNoch keine Bewertungen

- Roland Berger's global automotive supplier study highlights key trendsDokument40 SeitenRoland Berger's global automotive supplier study highlights key trendsvishansNoch keine Bewertungen

- BCG Perspectives - Mobile Payments in Africa: Graphics For ArticleDokument13 SeitenBCG Perspectives - Mobile Payments in Africa: Graphics For ArticleJean ClavelNoch keine Bewertungen

- SandeepDokument17 SeitenSandeepmerly chermonNoch keine Bewertungen

- Festival Belanja Cantik 17-20 Oct 2021Dokument15 SeitenFestival Belanja Cantik 17-20 Oct 2021Meyliana TaslimNoch keine Bewertungen

- BPO in Chile - 2007Dokument29 SeitenBPO in Chile - 2007bgngggggNoch keine Bewertungen

- MA Transaction Services TombstonesDokument101 SeitenMA Transaction Services TombstonesvramalhoNoch keine Bewertungen

- Investment and Industrial Policy: A Perspective on the FutureDokument23 SeitenInvestment and Industrial Policy: A Perspective on the FutureBagus EfendiNoch keine Bewertungen

- Online Category Management - AT Kearney ThinkWithGoogleDokument22 SeitenOnline Category Management - AT Kearney ThinkWithGooglemuhammad hamzaNoch keine Bewertungen

- CB Insights Digital Healthcare WebinarDokument80 SeitenCB Insights Digital Healthcare WebinarMohammed KhairyNoch keine Bewertungen

- B2B Marketplace Landscape India 2018Dokument3 SeitenB2B Marketplace Landscape India 2018ADITYANoch keine Bewertungen

- BCG Reigniting Radical Growth June 2019 Tcm9 222638Dokument33 SeitenBCG Reigniting Radical Growth June 2019 Tcm9 222638sdadaaNoch keine Bewertungen

- Bernstein India Strategy Are We On The Cusp of A Multi YearDokument16 SeitenBernstein India Strategy Are We On The Cusp of A Multi YeardanishNoch keine Bewertungen

- Perspectives On Manufacturing, Disruptive Technologies, and Industry 4.0Dokument17 SeitenPerspectives On Manufacturing, Disruptive Technologies, and Industry 4.0Andrey PritulyukNoch keine Bewertungen

- DEF (Luxury Lifestyle Leather) - Information Memorandum - Confidential Data HiddenDokument45 SeitenDEF (Luxury Lifestyle Leather) - Information Memorandum - Confidential Data Hiddenarijit nayakNoch keine Bewertungen

- Investment Teaser or Information Memorandum (CIM) TemplateDokument9 SeitenInvestment Teaser or Information Memorandum (CIM) TemplateAvinash JamiNoch keine Bewertungen

- Start Up Catalysts Incubators and AcceleratorsDokument89 SeitenStart Up Catalysts Incubators and Acceleratorsvenkata.krishnanNoch keine Bewertungen

- Hurun India Future Unicorn 2021 Fina Press ReleaselDokument14 SeitenHurun India Future Unicorn 2021 Fina Press ReleaselnikunjbubnaNoch keine Bewertungen

- Forecasting & Scenario Planning in Times of ChangeDokument35 SeitenForecasting & Scenario Planning in Times of ChangeMayank MishraNoch keine Bewertungen

- BCG-CII Big Picture Final Report Dec 2020Dokument114 SeitenBCG-CII Big Picture Final Report Dec 2020Meet Mukesh PaswanNoch keine Bewertungen

- BCG PerspectivesDokument40 SeitenBCG PerspectivescjchuaNoch keine Bewertungen

- Mudit Saxena - Genpact SeedDokument2 SeitenMudit Saxena - Genpact SeedParas SatijaNoch keine Bewertungen

- Gc-Presentation Manyika 10nov14Dokument11 SeitenGc-Presentation Manyika 10nov14c_bhanNoch keine Bewertungen

- TMT Predictions 202 - Deloitte IndiaDokument150 SeitenTMT Predictions 202 - Deloitte IndiaAakash MalhotraNoch keine Bewertungen

- The State of European Food Tech 2018Dokument20 SeitenThe State of European Food Tech 2018Taupik Ismail100% (1)

- Armenia's Economic Growth and Future PotentialDokument104 SeitenArmenia's Economic Growth and Future PotentialGUINoch keine Bewertungen

- ECO222 Lect Week9 2020 UDokument39 SeitenECO222 Lect Week9 2020 UKarina SNoch keine Bewertungen

- Ipengen PITCH DECK 011720 SeminarDokument22 SeitenIpengen PITCH DECK 011720 SeminarSyahrial SidikNoch keine Bewertungen

- I. Pre-Merger Insights - 1 Acquisition FactoryDokument12 SeitenI. Pre-Merger Insights - 1 Acquisition FactoryRadoslav RobertNoch keine Bewertungen

- HealthTech IndiaDokument204 SeitenHealthTech IndiaRohit Rsnwala75% (4)

- The Single Family Office Funds in IndiaDokument4 SeitenThe Single Family Office Funds in IndiagandhiannexNoch keine Bewertungen

- Belarusian Grocery Retail Market BCG - July2018 - English - tcm26 196435 PDFDokument158 SeitenBelarusian Grocery Retail Market BCG - July2018 - English - tcm26 196435 PDFmaxNoch keine Bewertungen

- 2017-11 AID Milan Fintech, How Financial Institutions McKinsey PDFDokument21 Seiten2017-11 AID Milan Fintech, How Financial Institutions McKinsey PDFHieu Nguyen MinhNoch keine Bewertungen

- Varanium 11042019Dokument25 SeitenVaranium 11042019Rahul JainNoch keine Bewertungen

- BCG Cardekho Digital Garage Feb 2017Dokument28 SeitenBCG Cardekho Digital Garage Feb 2017AshitSharmaNoch keine Bewertungen

- Bain CapitalDokument11 SeitenBain CapitalRaf SanchezNoch keine Bewertungen

- BOLD Investor PresentationDokument110 SeitenBOLD Investor PresentationSerge Olivier Atchu YudomNoch keine Bewertungen

- Making Decisions: 5 Fundamental Questions 1) Have Time? Ask Yourself About The Time RequirementsDokument1 SeiteMaking Decisions: 5 Fundamental Questions 1) Have Time? Ask Yourself About The Time RequirementsAl VelNoch keine Bewertungen

- 2019 Asia Insurance Market ReportDokument44 Seiten2019 Asia Insurance Market ReportFarraz RadityaNoch keine Bewertungen

- TechUK McKinseyPresentation VFDokument15 SeitenTechUK McKinseyPresentation VFfwfsdNoch keine Bewertungen

- DVB IIMA Case StudyDokument56 SeitenDVB IIMA Case StudyMitesh KumarNoch keine Bewertungen

- Consumer SectorDokument136 SeitenConsumer SectorYohannie LinggasariNoch keine Bewertungen

- People and business iconsDokument14 SeitenPeople and business iconsChing, Quennel YoenNoch keine Bewertungen

- Agriculture February 2017Dokument51 SeitenAgriculture February 2017Piyush SawantNoch keine Bewertungen

- India's Advantage in Agriculture SectorDokument51 SeitenIndia's Advantage in Agriculture Sectordineshjain11Noch keine Bewertungen

- Marketing Transformation of BJP CaseDokument23 SeitenMarketing Transformation of BJP Casecitrus100% (1)

- The F Quiz: #Women'SdayDokument51 SeitenThe F Quiz: #Women'SdayVaishnaviRaviNoch keine Bewertungen

- Revenue Management & Dynamic Pricing OptimizationDokument15 SeitenRevenue Management & Dynamic Pricing OptimizationVaishnaviRaviNoch keine Bewertungen

- Edelweiss Financial ServicesDokument3 SeitenEdelweiss Financial ServicesVaishnaviRaviNoch keine Bewertungen

- KC Devarajan 2020Dokument122 SeitenKC Devarajan 2020VaishnaviRaviNoch keine Bewertungen

- FINAL - Revised - Calendar - July 12, 2020Dokument1 SeiteFINAL - Revised - Calendar - July 12, 2020VaishnaviRaviNoch keine Bewertungen

- ICQC Karuna QuizDokument32 SeitenICQC Karuna QuizVaishnaviRaviNoch keine Bewertungen

- Popcultureprelimsanswers 180312134204Dokument43 SeitenPopcultureprelimsanswers 180312134204VaishnaviRaviNoch keine Bewertungen

- Sphinx - The General Quiz (Finals)Dokument151 SeitenSphinx - The General Quiz (Finals)VaishnaviRaviNoch keine Bewertungen

- 7850-Article Text-18236-1-10-20180627 PDFDokument21 Seiten7850-Article Text-18236-1-10-20180627 PDFjuaenelviraNoch keine Bewertungen

- Revenue Management & Dynamic PricingDokument10 SeitenRevenue Management & Dynamic PricingVaishnaviRaviNoch keine Bewertungen

- Booking Limit ExsDokument2 SeitenBooking Limit ExsVaishnaviRaviNoch keine Bewertungen

- Edelweiss Financial ServicesDokument3 SeitenEdelweiss Financial ServicesVaishnaviRaviNoch keine Bewertungen

- Company Website AboutDokument4 SeitenCompany Website AboutVaishnaviRaviNoch keine Bewertungen

- Batteries: Characterisation of A 200 Kw/400 KWH Vanadium Redox Flow BatteryDokument16 SeitenBatteries: Characterisation of A 200 Kw/400 KWH Vanadium Redox Flow BatteryJohnNoch keine Bewertungen

- NRI - Nomura Research InstituteDokument2 SeitenNRI - Nomura Research InstituteVaishnaviRaviNoch keine Bewertungen

- Salvini 2017Dokument8 SeitenSalvini 2017Vedhish HalkhariNoch keine Bewertungen

- Company NameDokument3 SeitenCompany NameVaishnaviRaviNoch keine Bewertungen

- Case Study Re-Lead 3.0Dokument6 SeitenCase Study Re-Lead 3.0yashi mittalNoch keine Bewertungen

- Applied Sciences: A Review of Flywheel Energy Storage System Technologies and Their ApplicationsDokument21 SeitenApplied Sciences: A Review of Flywheel Energy Storage System Technologies and Their ApplicationsRavi GoyalNoch keine Bewertungen

- Neo and Challenger Bank Market: Author (S) : Sheetanshu Upadhyay and Anshuman BudhirajaDokument40 SeitenNeo and Challenger Bank Market: Author (S) : Sheetanshu Upadhyay and Anshuman BudhirajaVaishnaviRaviNoch keine Bewertungen

- Grid Scale Battery StorageDokument8 SeitenGrid Scale Battery StoragetyaskartikaNoch keine Bewertungen

- FinTechnicolor The New Picture in Finance PDFDokument84 SeitenFinTechnicolor The New Picture in Finance PDFalex.kestner384Noch keine Bewertungen

- Study: People Matter, Results CountDokument3 SeitenStudy: People Matter, Results CountVaishnaviRaviNoch keine Bewertungen

- Study: People Matter, Results CountDokument3 SeitenStudy: People Matter, Results CountVaishnaviRaviNoch keine Bewertungen

- Framing New Futures: Challenger Banking Report 2017Dokument24 SeitenFraming New Futures: Challenger Banking Report 2017VaishnaviRaviNoch keine Bewertungen

- Explore Innovate DisruptDokument5 SeitenExplore Innovate DisruptVaishnaviRaviNoch keine Bewertungen

- FT Partners Research - The Rise of Challenger BanksDokument217 SeitenFT Partners Research - The Rise of Challenger BanksnguoinhenvnNoch keine Bewertungen

- Fintech in Asia Pacific: Digital Payment Platforms: October 2019Dokument42 SeitenFintech in Asia Pacific: Digital Payment Platforms: October 2019VaishnaviRaviNoch keine Bewertungen

- Backbase The ROI of Omni Channel WhitepaperDokument21 SeitenBackbase The ROI of Omni Channel Whitepaperpk8barnesNoch keine Bewertungen

- S Poddar and Co ProfileDokument35 SeitenS Poddar and Co ProfileasassasaaNoch keine Bewertungen

- Report On PresentationDokument23 SeitenReport On PresentationKishore Thomas JohnNoch keine Bewertungen

- Natwarlal & CompanyDokument17 SeitenNatwarlal & Companysunil jadhavNoch keine Bewertungen

- E-Way BillDokument1 SeiteE-Way BillShriyans DaftariNoch keine Bewertungen

- STOCK PRICESDokument51 SeitenSTOCK PRICESBellwetherSataraNoch keine Bewertungen

- Evaluation of Indian RetailDokument71 SeitenEvaluation of Indian Retaildr_tripathineeraj100% (1)

- Saraswat Co-op Bank HistoryDokument4 SeitenSaraswat Co-op Bank HistoryVishal YadavNoch keine Bewertungen

- Psu Contact ListDokument5 SeitenPsu Contact ListSiddharth Dua0% (1)

- Exp KDL Feb-15 (Excel)Dokument44 SeitenExp KDL Feb-15 (Excel)vivek_domadiaNoch keine Bewertungen

- Bharatiy Arthvyavstha Sankat Me: Covid-19 Ka Prabhav Eanv ChunotiyaDokument8 SeitenBharatiy Arthvyavstha Sankat Me: Covid-19 Ka Prabhav Eanv ChunotiyaAnonymous CwJeBCAXpNoch keine Bewertungen

- Employee Details SpreadsheetDokument63 SeitenEmployee Details SpreadsheetiKix 3dprints100% (1)

- R P Goenka EditedDokument22 SeitenR P Goenka EditedSharmishtha RajakNoch keine Bewertungen

- ShitalDokument114 SeitenShitalShital PatilNoch keine Bewertungen

- IT ParksDokument6 SeitenIT ParksShahab Z AhmedNoch keine Bewertungen

- Understanding Public, Private and Global EnterprisesDokument23 SeitenUnderstanding Public, Private and Global EnterprisesDev Krishna GoyalNoch keine Bewertungen

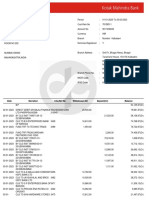

- Icici Bank StatementDokument22 SeitenIcici Bank StatementVIJAY BHASAKAR100% (1)

- Nippon FundsDokument33 SeitenNippon FundsArmstrong CapitalNoch keine Bewertungen

- SI Classes for WBCS ExamDokument8 SeitenSI Classes for WBCS ExamSudipto RoyNoch keine Bewertungen

- Pranav Jewellery ReportDokument59 SeitenPranav Jewellery ReportAkash KapoorNoch keine Bewertungen

- causelistALL2023 07 12Dokument11 SeitencauselistALL2023 07 12wotitNoch keine Bewertungen

- 501 Stocks Filtered 23-09-2022Dokument26 Seiten501 Stocks Filtered 23-09-2022MohammadRahemanNoch keine Bewertungen

- Impactof Coronaon Textile SectorDokument9 SeitenImpactof Coronaon Textile SectorKanchan AgarwalNoch keine Bewertungen

- Onlyias-Indian EconomyDokument444 SeitenOnlyias-Indian EconomyAnkurNoch keine Bewertungen

- List of AP Names for IDBI Bank LimitedDokument711 SeitenList of AP Names for IDBI Bank LimitedmalumaatNoch keine Bewertungen

- Salary Calculator 6 CPC (Civ and Def)Dokument3 SeitenSalary Calculator 6 CPC (Civ and Def)gaikwad_avi100% (9)

- Time Table W43-Ad (17-October-22 - 23-October-22)Dokument1 SeiteTime Table W43-Ad (17-October-22 - 23-October-22)Piyush kumarNoch keine Bewertungen

- Classification of Industries Based on Various FactorsDokument12 SeitenClassification of Industries Based on Various FactorsBhagyashree Dhimmar100% (2)

- List of Insurance Companies (India)Dokument8 SeitenList of Insurance Companies (India)pradeepk6640Noch keine Bewertungen

- NABARD Strengthens Rural RoadsDokument2 SeitenNABARD Strengthens Rural RoadsKarunamoorthi PonnuswamyNoch keine Bewertungen

- DatabaseDokument8 SeitenDatabaseMangeshRudrawarNoch keine Bewertungen