Das könnte Ihnen auch gefallen

- Possible Non-Indo-European Elements in HittiteDokument16 SeitenPossible Non-Indo-European Elements in HittitelastofthelastNoch keine Bewertungen

- List of English Verbs in All TensesDokument33 SeitenList of English Verbs in All TensesRamanNoch keine Bewertungen

- Fast-Track Tax Reform: Lessons from the MaldivesVon EverandFast-Track Tax Reform: Lessons from the MaldivesNoch keine Bewertungen

- Brigham Chap 11 Practice Questions Solution For Chap 11Dokument11 SeitenBrigham Chap 11 Practice Questions Solution For Chap 11robin.asterNoch keine Bewertungen

- Assignment 01: Audit of Property, Plant and Equipment Problem SolvingDokument2 SeitenAssignment 01: Audit of Property, Plant and Equipment Problem SolvingDan Andrei BongoNoch keine Bewertungen

- Pup-Ppe5-Src 2-1Dokument15 SeitenPup-Ppe5-Src 2-1Jerome BaluseroNoch keine Bewertungen

- Case Digest (Complete)Dokument7 SeitenCase Digest (Complete)Shailah Leilene Arce Briones100% (1)

- Capital Budgeting DCFDokument38 SeitenCapital Budgeting DCFNadya Rizkita100% (4)

- Barriga Vs Sandiganbayan - Case DigestDokument3 SeitenBarriga Vs Sandiganbayan - Case DigestXeem LeenNoch keine Bewertungen

- Confidential 1 AC/TEST MAY 2021/FAR270Dokument5 SeitenConfidential 1 AC/TEST MAY 2021/FAR270Lampard AimanNoch keine Bewertungen

- Cash+flow+estimation (14-1759)Dokument9 SeitenCash+flow+estimation (14-1759)M shahjamal QureshiNoch keine Bewertungen

- T 4Dokument3 SeitenT 4Muntasir AhmmedNoch keine Bewertungen

- Mid-Semester Exam: Af 302 - Information SystemsDokument14 SeitenMid-Semester Exam: Af 302 - Information SystemsChand DivneshNoch keine Bewertungen

- Far Tutor 3Dokument4 SeitenFar Tutor 3Rian RorresNoch keine Bewertungen

- Topic 4 Revaluation Property Plant and EquipmentDokument6 SeitenTopic 4 Revaluation Property Plant and Equipmentjinman bongNoch keine Bewertungen

- Tutorial 4 SolutionsDokument5 SeitenTutorial 4 SolutionsnaboumilikaNoch keine Bewertungen

- Depreciation CalculationDokument29 SeitenDepreciation CalculationRavineahNoch keine Bewertungen

- ACCT2201 Chapter 9Dokument8 SeitenACCT2201 Chapter 9erinNoch keine Bewertungen

- Tutorial 3 Tutorial 3Dokument13 SeitenTutorial 3 Tutorial 3Andrei Nicole RiveraNoch keine Bewertungen

- Chapter 10 Exercises Acc101Dokument6 SeitenChapter 10 Exercises Acc101Nguyen Thi Van Anh (K17 HL)Noch keine Bewertungen

- CapbdgtDokument25 SeitenCapbdgtmajidNoch keine Bewertungen

- Chapter: Non-Current Assets and Depreciation Answers For Model QuestionDokument4 SeitenChapter: Non-Current Assets and Depreciation Answers For Model QuestionRAJIB HOSSAINNoch keine Bewertungen

- Chapter 20Dokument6 SeitenChapter 20Dasun LakshithNoch keine Bewertungen

- 10 Non-Current AssetsDokument25 Seiten10 Non-Current AssetsDayaan ANoch keine Bewertungen

- 2014 Final Exam SolutionsDokument6 Seiten2014 Final Exam SolutionsAyaan Ahaan Malik-WilliamsNoch keine Bewertungen

- ACC1100 S1 2018 Exam SolutionDokument15 SeitenACC1100 S1 2018 Exam SolutionFarah PatelNoch keine Bewertungen

- Sem 7Dokument84 SeitenSem 7Bình QuốcNoch keine Bewertungen

- ACC-ACF2100 Lecture 5 HandoutDokument7 SeitenACC-ACF2100 Lecture 5 HandoutDanNoch keine Bewertungen

- Presentation On Internal ReconstructionDokument23 SeitenPresentation On Internal Reconstructionneeru79200040% (5)

- ACW2491 Financial Accounting Tutorial Solution Semester 2 2018 Topic 5: Property, Plant and Equipment-RevaluationDokument8 SeitenACW2491 Financial Accounting Tutorial Solution Semester 2 2018 Topic 5: Property, Plant and Equipment-RevaluationAhsan MasoodNoch keine Bewertungen

- Answer Key 3Dokument8 SeitenAnswer Key 3Hari prakarsh NimiNoch keine Bewertungen

- PA1 Group1 P10Dokument8 SeitenPA1 Group1 P10Phuong Nguyen MinhNoch keine Bewertungen

- A1. Fm-2018-Sepdec-Sample-ADokument4 SeitenA1. Fm-2018-Sepdec-Sample-ANirmal ShresthaNoch keine Bewertungen

- Solution - B124 - FTHE - V2 Summer 2020-2021 2 - V1Dokument13 SeitenSolution - B124 - FTHE - V2 Summer 2020-2021 2 - V1AhmEd GhayasNoch keine Bewertungen

- A Profit and Loss Budget For The 6 Months Ending 31/12/2020Dokument6 SeitenA Profit and Loss Budget For The 6 Months Ending 31/12/2020Miral AqelNoch keine Bewertungen

- PA1 Group1 Week8Dokument8 SeitenPA1 Group1 Week8Phuong Nguyen MinhNoch keine Bewertungen

- Jawaban Soal Quiz No 2 Dan 3Dokument4 SeitenJawaban Soal Quiz No 2 Dan 3Anthony indrahalimNoch keine Bewertungen

- This Study Resource Was: Question 3. Blindfold Technologies Inc. (BTI) Is Considering Whether To Introduce A NewDokument2 SeitenThis Study Resource Was: Question 3. Blindfold Technologies Inc. (BTI) Is Considering Whether To Introduce A NewFaradibaNoch keine Bewertungen

- Accounting For Long Term Assets Property Plant and Equipment (Ias 16)Dokument7 SeitenAccounting For Long Term Assets Property Plant and Equipment (Ias 16)ZAKAYO NJONYNoch keine Bewertungen

- CPA 14-Public Sector Accounting & ReportingDokument15 SeitenCPA 14-Public Sector Accounting & ReportingManit MehtaNoch keine Bewertungen

- Accts Imp QnsDokument4 SeitenAccts Imp QnsnishabilochiNoch keine Bewertungen

- Problems Problem 10.1: © John Wiley and Sons Australia, LTD 2010 10.21Dokument5 SeitenProblems Problem 10.1: © John Wiley and Sons Australia, LTD 2010 10.21alfaressNoch keine Bewertungen

- Answer BE9-2 Explanation:: Calculation of Book Value and Accumulated Depreciation For Each of The AssetsDokument2 SeitenAnswer BE9-2 Explanation:: Calculation of Book Value and Accumulated Depreciation For Each of The AssetsYousuf SiyamNoch keine Bewertungen

- Category Cost of Asset Accumulated DepreciationDokument10 SeitenCategory Cost of Asset Accumulated DepreciationAaliyah ManuelNoch keine Bewertungen

- Case 3.7Dokument7 SeitenCase 3.7Thái SơnNoch keine Bewertungen

- Solution Aassignments CH 9Dokument10 SeitenSolution Aassignments CH 9RuturajPatilNoch keine Bewertungen

- Solution Practice 5 Consolidations 2Dokument7 SeitenSolution Practice 5 Consolidations 2Mya Hmuu KhinNoch keine Bewertungen

- Paper14 Strategic Financial ManagementDokument34 SeitenPaper14 Strategic Financial ManagementKumar SAPNoch keine Bewertungen

- ALACDokument18 SeitenALACshruthisreehkNoch keine Bewertungen

- December 2019Dokument20 SeitenDecember 2019Kunal GargNoch keine Bewertungen

- Suggested Answer CAP II December 2016Dokument88 SeitenSuggested Answer CAP II December 2016Nirmal ShresthaNoch keine Bewertungen

- Ex08 Capital Budgeting XXDokument16 SeitenEx08 Capital Budgeting XXbrmo.amatorio.uiNoch keine Bewertungen

- Tutorial Pack On PpeDokument14 SeitenTutorial Pack On PpeAyandiswa NdebeleNoch keine Bewertungen

- Madaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Dokument17 SeitenMadaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Maryjoy KilonzoNoch keine Bewertungen

- Class Exercise CH 10Dokument5 SeitenClass Exercise CH 10Iftekhar AhmedNoch keine Bewertungen

- MS Xii Accountancy Set 1Dokument10 SeitenMS Xii Accountancy Set 1arikoff07Noch keine Bewertungen

- ACCY200 Tutorial Solutions Week 8Dokument10 SeitenACCY200 Tutorial Solutions Week 8duraton94Noch keine Bewertungen

- ACC 3003-Key Revision For Test 1Dokument7 SeitenACC 3003-Key Revision For Test 1falnuaimi001Noch keine Bewertungen

- Ch.12 Part 2 ManagrialDokument3 SeitenCh.12 Part 2 ManagrialAhmed TahaNoch keine Bewertungen

- Bv2018 Revised Conceptual FrameworkDokument18 SeitenBv2018 Revised Conceptual FrameworkTeneswari RadhaNoch keine Bewertungen

- 108A W23++Homework+8Dokument8 Seiten108A W23++Homework+8Julius SuhermanNoch keine Bewertungen

- FINA 3330 - Notes CH 9Dokument2 SeitenFINA 3330 - Notes CH 9fische100% (1)

- Marginal Costing MCQDokument55 SeitenMarginal Costing MCQMuhammad Shabbar BukhariNoch keine Bewertungen

- Answer Keys & Marking Scheme Acc XiiDokument8 SeitenAnswer Keys & Marking Scheme Acc XiiGHOST FFNoch keine Bewertungen

- Economics of Climate Change Mitigation in Central and West AsiaVon EverandEconomics of Climate Change Mitigation in Central and West AsiaNoch keine Bewertungen

- Af201 Mid-Test-S2 2019 - FINALDokument10 SeitenAf201 Mid-Test-S2 2019 - FINALChand DivneshNoch keine Bewertungen

- Week 2 Tutorial QuestionsDokument2 SeitenWeek 2 Tutorial QuestionsChand DivneshNoch keine Bewertungen

- AF201 Final Exam s2, 2019 - Suggested Solution Q3 Q4Dokument2 SeitenAF201 Final Exam s2, 2019 - Suggested Solution Q3 Q4Chand DivneshNoch keine Bewertungen

- AF201 REVISION PACKAGE s1, 2021Dokument4 SeitenAF201 REVISION PACKAGE s1, 2021Chand DivneshNoch keine Bewertungen

- Af302 Semester 1 - 2017 Mid-Test Solutions: Question 1 Multiple Choice SolutionsDokument9 SeitenAf302 Semester 1 - 2017 Mid-Test Solutions: Question 1 Multiple Choice SolutionsChand DivneshNoch keine Bewertungen

- Tutorial 09: Questions With Possible SolutionsDokument4 SeitenTutorial 09: Questions With Possible SolutionsChand DivneshNoch keine Bewertungen

- Week 9: Tutorial 08 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Dokument3 SeitenWeek 9: Tutorial 08 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Chand DivneshNoch keine Bewertungen

- AF201 Final Exam - Suggested Solution - s1, 2018 - Final Qs 1, 2, 3Dokument2 SeitenAF201 Final Exam - Suggested Solution - s1, 2018 - Final Qs 1, 2, 3Chand DivneshNoch keine Bewertungen

- Af201 Final Exam Revision Package - S2, 2020 Face-to-Face & Blended Modes Suggested Partial SolutionsDokument9 SeitenAf201 Final Exam Revision Package - S2, 2020 Face-to-Face & Blended Modes Suggested Partial SolutionsChand DivneshNoch keine Bewertungen

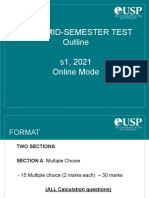

- Af201 Mid-Semester Test Outline s1, 2021 Online ModeDokument4 SeitenAf201 Mid-Semester Test Outline s1, 2021 Online ModeChand DivneshNoch keine Bewertungen

- Af201 Final Exam Revision PackageDokument12 SeitenAf201 Final Exam Revision PackageChand DivneshNoch keine Bewertungen

- Tutorial 05 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Dokument3 SeitenTutorial 05 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Chand DivneshNoch keine Bewertungen

- Tutorial 07: Project ManagementDokument1 SeiteTutorial 07: Project ManagementChand DivneshNoch keine Bewertungen

- AF302chapter 4 Tutorial SolutionsDokument7 SeitenAF302chapter 4 Tutorial SolutionsChand DivneshNoch keine Bewertungen

- Tutorial 03: Questions With Partial SolutionsDokument4 SeitenTutorial 03: Questions With Partial SolutionsChand DivneshNoch keine Bewertungen

- Tutorial 04 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Dokument2 SeitenTutorial 04 Questions With Possible Solutions: IS333: Project Management - Semester I 2021Chand DivneshNoch keine Bewertungen

- Is226 Tutorial 6 Problems For Week 7: Modeling Systems Requirements - DfdsDokument4 SeitenIs226 Tutorial 6 Problems For Week 7: Modeling Systems Requirements - DfdsChand DivneshNoch keine Bewertungen

- Chapter 3 Tutorial SolutionsDokument8 SeitenChapter 3 Tutorial SolutionsChand DivneshNoch keine Bewertungen

- Tutorial 01 Questions With Possible SolutionsDokument3 SeitenTutorial 01 Questions With Possible SolutionsChand DivneshNoch keine Bewertungen

- AF302chapter 5 Tutorial SolutionsDokument10 SeitenAF302chapter 5 Tutorial SolutionsChand DivneshNoch keine Bewertungen

- AF302 Chapter-2-SolutionsDokument6 SeitenAF302 Chapter-2-SolutionsChand DivneshNoch keine Bewertungen

- The University of The South Pacific: School of Computing, Information and Mathematical SciencesDokument8 SeitenThe University of The South Pacific: School of Computing, Information and Mathematical SciencesChand DivneshNoch keine Bewertungen

- AF302 Ch01-Tutorial-Answers-For-Chapter-01Dokument18 SeitenAF302 Ch01-Tutorial-Answers-For-Chapter-01Chand DivneshNoch keine Bewertungen

- Tutorial 5 - Sols - Modeling System RequirementsDokument6 SeitenTutorial 5 - Sols - Modeling System RequirementsChand Divnesh100% (1)

- AF121 Week 4 - Fraud Ethics NewDokument18 SeitenAF121 Week 4 - Fraud Ethics NewChand DivneshNoch keine Bewertungen

- Fraud, Ethics & Internal Controls: Chapter 3 Cont' Week 4: Lecture # 2Dokument27 SeitenFraud, Ethics & Internal Controls: Chapter 3 Cont' Week 4: Lecture # 2Chand DivneshNoch keine Bewertungen

- AF121 Week 3-UNIT 2 Cont....Dokument10 SeitenAF121 Week 3-UNIT 2 Cont....Chand DivneshNoch keine Bewertungen

- Happiness Level 1 - Exercises PDFDokument2 SeitenHappiness Level 1 - Exercises PDFMohamed Amine AkouhNoch keine Bewertungen

- Electrical Electronic Devices ShabbatDokument79 SeitenElectrical Electronic Devices Shabbatמאירה הדרNoch keine Bewertungen

- JudiciaryDokument21 SeitenJudiciaryAdityaNoch keine Bewertungen

- Creative Works - Main Report - ABCDDokument65 SeitenCreative Works - Main Report - ABCDvenkatesh subbaiyaNoch keine Bewertungen

- ME 457 Experimental Solid Mechanics (Lab) Torsion Test: Solid and Hollow ShaftsDokument5 SeitenME 457 Experimental Solid Mechanics (Lab) Torsion Test: Solid and Hollow Shaftsanon-735529100% (2)

- 3 Angels NepalDokument46 Seiten3 Angels Nepalविवेक शर्माNoch keine Bewertungen

- ADL Audit of Anti-Semitic Incidents 2021Dokument38 SeitenADL Audit of Anti-Semitic Incidents 2021Michael_Roberts2019Noch keine Bewertungen

- Asaba FSE Site Distribution - Week 20 FY12Dokument115 SeitenAsaba FSE Site Distribution - Week 20 FY12Adetayo OnanugaNoch keine Bewertungen

- ME 261 Numerical Analysis: System of Linear EquationsDokument15 SeitenME 261 Numerical Analysis: System of Linear EquationsTahmeed HossainNoch keine Bewertungen

- Full Download Introduction To Operations and Supply Chain Management 3rd Edition Bozarth Test BankDokument36 SeitenFull Download Introduction To Operations and Supply Chain Management 3rd Edition Bozarth Test Bankcoraleementgen1858100% (42)

- The Birth of The Bipolar Disorder: Historical ReviewDokument10 SeitenThe Birth of The Bipolar Disorder: Historical ReviewFELIPE ABREONoch keine Bewertungen

- Human Medicinal Agents From PlantsDokument358 SeitenHuman Medicinal Agents From Plantsamino12451100% (1)

- MKT216SL - Business and Market Research: To Introduce Designer Jeans To The Young Generation in Sri LankaDokument32 SeitenMKT216SL - Business and Market Research: To Introduce Designer Jeans To The Young Generation in Sri Lankajey456Noch keine Bewertungen

- Answer Key: Cumulative TestDokument2 SeitenAnswer Key: Cumulative TestTeodora MitrovicNoch keine Bewertungen

- Are Indian Tribals Hindus by Shrikant TalageriDokument40 SeitenAre Indian Tribals Hindus by Shrikant TalagerirahulchicNoch keine Bewertungen

- Favoritism Bad Habbit of Some TeacherDokument2 SeitenFavoritism Bad Habbit of Some TeacherQasim TapsiNoch keine Bewertungen

- Nguyễn Thành Tín SPA-K42B Robinson Crusoe 1. Tell briefly of Enlightenment and Daniel Defoe. - The Age of EnlightenmentDokument4 SeitenNguyễn Thành Tín SPA-K42B Robinson Crusoe 1. Tell briefly of Enlightenment and Daniel Defoe. - The Age of EnlightenmentnguyenthanhtinNoch keine Bewertungen

- Application of Aging Theories To NursingDokument3 SeitenApplication of Aging Theories To NursingArvin LabradaNoch keine Bewertungen

- Haunted Castles IrelandDokument3 SeitenHaunted Castles IrelandRenata TatomirNoch keine Bewertungen

- Kelulusan Nso 2010Dokument49 SeitenKelulusan Nso 2010Sanny NurbhaktiNoch keine Bewertungen

- Chapter 8 Accounts Receivable and Further Record-Keeping: Discussion QuestionsDokument3 SeitenChapter 8 Accounts Receivable and Further Record-Keeping: Discussion Questionskiet100% (1)

- Bachelor Series 7 His TemptressDokument275 SeitenBachelor Series 7 His Temptresscam UyangurenNoch keine Bewertungen

- Unit 3 - 1 PDFDokument3 SeitenUnit 3 - 1 PDFyngrid czNoch keine Bewertungen

- The Basics of Systems Geology: British Geological Survey, 2012. HTTP://WWW - Bgs.ac - Uk/systemsgeology/basics PDFDokument0 SeitenThe Basics of Systems Geology: British Geological Survey, 2012. HTTP://WWW - Bgs.ac - Uk/systemsgeology/basics PDFivica_918613161Noch keine Bewertungen

- Test - SchoolDokument3 SeitenTest - SchoolAna MateusNoch keine Bewertungen

- Designing Organizational Structure: Authority and ControlDokument48 SeitenDesigning Organizational Structure: Authority and ControlArvind DawarNoch keine Bewertungen