Das könnte Ihnen auch gefallen

- My Part 1,2,3Dokument3 SeitenMy Part 1,2,3Aniruddha RantuNoch keine Bewertungen

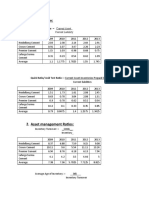

- Liquidity Ratio:: Current Ratio: Current AssetDokument6 SeitenLiquidity Ratio:: Current Ratio: Current AssetAniruddha RantuNoch keine Bewertungen

- Brand Strategy:: "Batting Like A Gentleman"Dokument3 SeitenBrand Strategy:: "Batting Like A Gentleman"Aniruddha RantuNoch keine Bewertungen

- Accounting: Making Sound Decisions: Non-Current AssetsDokument2 SeitenAccounting: Making Sound Decisions: Non-Current AssetsAniruddha Rantu40% (5)

- Riyad PC DraftDokument1 SeiteRiyad PC DraftAniruddha RantuNoch keine Bewertungen

- Political Communications: Pressure GroupsDokument16 SeitenPolitical Communications: Pressure GroupsAniruddha RantuNoch keine Bewertungen

- North South University: MGT-210 Submitted To: Nusrat Nabi (NBI)Dokument9 SeitenNorth South University: MGT-210 Submitted To: Nusrat Nabi (NBI)Aniruddha RantuNoch keine Bewertungen

- Fin435 1Dokument3 SeitenFin435 1Aniruddha RantuNoch keine Bewertungen

- CV Writing bootcampFinActDokument35 SeitenCV Writing bootcampFinActAniruddha RantuNoch keine Bewertungen

- Section 2 Mid 2 ScoresDokument1 SeiteSection 2 Mid 2 ScoresAniruddha RantuNoch keine Bewertungen

- Fin435 2Dokument3 SeitenFin435 2Aniruddha RantuNoch keine Bewertungen

- Company Law PPT 2Dokument8 SeitenCompany Law PPT 2Aniruddha RantuNoch keine Bewertungen

- Fin435 1Dokument2 SeitenFin435 1Aniruddha RantuNoch keine Bewertungen

- Chapter 03 - How Securities Are TradedDokument47 SeitenChapter 03 - How Securities Are TradedAniruddha RantuNoch keine Bewertungen

- Lecture Note - 11 Advertising & Sales Promotion: (Chapter 15 & 16, Kotler &amstrong 14 Ed.)Dokument40 SeitenLecture Note - 11 Advertising & Sales Promotion: (Chapter 15 & 16, Kotler &amstrong 14 Ed.)Aniruddha RantuNoch keine Bewertungen

- Tender Offer: I. Ii. Iii. Iv. VDokument12 SeitenTender Offer: I. Ii. Iii. Iv. VAniruddha RantuNoch keine Bewertungen

- You Either Come HereDokument1 SeiteYou Either Come HereAniruddha RantuNoch keine Bewertungen

- Trade Union: (I) Every Worker Has The Right To Constitute A Trade Union and ToDokument23 SeitenTrade Union: (I) Every Worker Has The Right To Constitute A Trade Union and ToAniruddha RantuNoch keine Bewertungen

- Eco PresDokument2 SeitenEco PresAniruddha RantuNoch keine Bewertungen

- Importance of A College DegreeDokument4 SeitenImportance of A College DegreeAniruddha RantuNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Management Review in 2020Dokument13 SeitenManagement Review in 2020Giang Luu100% (1)

- RESUME SAP Financing Unit 3Dokument3 SeitenRESUME SAP Financing Unit 3Fishara AdhaNoch keine Bewertungen

- Module 4 Construction and Real Estate IndustryDokument14 SeitenModule 4 Construction and Real Estate IndustryChelsea ConcepcionNoch keine Bewertungen

- Pashupati Singh (C.V)Dokument3 SeitenPashupati Singh (C.V)Pashupati SinghNoch keine Bewertungen

- Module 2 Cg. 2022Dokument39 SeitenModule 2 Cg. 2022Parikshit MishraNoch keine Bewertungen

- EG PRACTICE EXAM 1 Course Outline KnowledgEquity PDFDokument47 SeitenEG PRACTICE EXAM 1 Course Outline KnowledgEquity PDFmeeteshlalNoch keine Bewertungen

- Germany SpainDokument18 SeitenGermany SpainsriramNoch keine Bewertungen

- Compliance ForumDokument76 SeitenCompliance ForumMary RoseNoch keine Bewertungen

- Sec Contact Center: Matters of Concern Email Address/ Website Phone NumberDokument7 SeitenSec Contact Center: Matters of Concern Email Address/ Website Phone NumberJerome FlojoNoch keine Bewertungen

- Hul Annual ReportDokument228 SeitenHul Annual Reportrintu somanNoch keine Bewertungen

- 201702fraud Responsibility MatrixDokument4 Seiten201702fraud Responsibility MatrixChinh Lê ĐìnhNoch keine Bewertungen

- Final Fraud ReportDokument27 SeitenFinal Fraud Reportpvchandu100% (1)

- Chap 1 - MAS Practice StandardsDokument13 SeitenChap 1 - MAS Practice StandardsCamille Francisco AgustinNoch keine Bewertungen

- Audit Case StudyDokument255 SeitenAudit Case Studyshan alisuperiorNoch keine Bewertungen

- ASS1-14 March 2022 - ACC2ADokument6 SeitenASS1-14 March 2022 - ACC2AThemba Patrick MolefeNoch keine Bewertungen

- Commission On Audit Circular No. 92-125A March 4, 1992 TO: All Heads of Departments, Bureaus and Offices of The National GovernmentDokument6 SeitenCommission On Audit Circular No. 92-125A March 4, 1992 TO: All Heads of Departments, Bureaus and Offices of The National GovernmentJade Darping KarimNoch keine Bewertungen

- NYRA Interim Report - TakeoutDokument20 SeitenNYRA Interim Report - TakeoutNick Reisman100% (1)

- Save Coconut Multipurpose Cooperative By-LawsDokument20 SeitenSave Coconut Multipurpose Cooperative By-LawsMario Vergel OcampoNoch keine Bewertungen

- Ps 44011Dokument10 SeitenPs 44011manuelNoch keine Bewertungen

- Accounting For Governmental & Nonprofit Entities: of Mcgraw HillDokument39 SeitenAccounting For Governmental & Nonprofit Entities: of Mcgraw HillJosef Galileo SibalaNoch keine Bewertungen

- Curriculum Vitae of KothandramanDokument8 SeitenCurriculum Vitae of KothandramanKothandaraman Thodur MadapusiNoch keine Bewertungen

- 2010 - RL Burritt, S Schaltegger - Ustainability Accounting and Reporting Fad or Trend PDFDokument18 Seiten2010 - RL Burritt, S Schaltegger - Ustainability Accounting and Reporting Fad or Trend PDFahmed sharkasNoch keine Bewertungen

- Bakhtyar Stanikzai CVDokument3 SeitenBakhtyar Stanikzai CVBakhtyar StanikzaiNoch keine Bewertungen

- Is Enhanced Audit Quality Associated With Greater Real Earnings Management?Dokument22 SeitenIs Enhanced Audit Quality Associated With Greater Real Earnings Management?Darvin AnanthanNoch keine Bewertungen

- Settlement of ND and NCDokument2 SeitenSettlement of ND and NCTeam R12-01 Cotabato ProvinceNoch keine Bewertungen

- Republic of The Philippines Court of Tax Appeals Quezon City First DivisionDokument55 SeitenRepublic of The Philippines Court of Tax Appeals Quezon City First DivisionYna YnaNoch keine Bewertungen

- BBC Ar Online 2009 10Dokument101 SeitenBBC Ar Online 2009 10Pornthep KamonpetchNoch keine Bewertungen

- Unit 2Dokument25 SeitenUnit 2FantayNoch keine Bewertungen

- Auditing Expense CycleDokument1 SeiteAuditing Expense CycleMelvin Jan SujedeNoch keine Bewertungen

- What Is Cost AccountingDokument3 SeitenWhat Is Cost AccountingWajahat BhattiNoch keine Bewertungen