Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Running Head: Comparing Two State It PoliciesDokument7 SeitenRunning Head: Comparing Two State It PoliciesKashémNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Budgeting and PlanningDokument2 SeitenBudgeting and PlanningKashémNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Current EventsDokument4 SeitenCurrent EventsKashémNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Work InvoiceDokument1 SeiteWork InvoiceKashémNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Investment Risk and ReturnDokument2 SeitenInvestment Risk and ReturnKashémNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- After Tax 9incomeDokument4 SeitenAfter Tax 9incomeKashémNoch keine Bewertungen

- ReportDokument5 SeitenReportKashémNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Sellum Case Study-MemoDokument2 SeitenSellum Case Study-MemoKashémNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Revolutionary Addiction Treatment For The LGBT CommunityDokument8 SeitenRevolutionary Addiction Treatment For The LGBT CommunityKashémNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Running Head: Multiple Essay QuestionsDokument6 SeitenRunning Head: Multiple Essay QuestionsKashémNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Paradox of Electoral EconomicsDokument10 SeitenThe Paradox of Electoral EconomicsKashémNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Social Statistics AssignmentDokument4 SeitenSocial Statistics AssignmentKashémNoch keine Bewertungen

- DERIVATIVESDokument2 SeitenDERIVATIVESKashémNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Total Cost of OwnershipDokument1 SeiteTotal Cost of OwnershipKashémNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Decision Making in AccountingDokument4 SeitenDecision Making in AccountingKashémNoch keine Bewertungen

- Budgeting and Planning Papa Geo Restaurant Draft BudgetDokument2 SeitenBudgeting and Planning Papa Geo Restaurant Draft BudgetKashémNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Total Cost of OwnershipDokument2 SeitenTotal Cost of OwnershipKashémNoch keine Bewertungen

- Probability AnswersDokument2 SeitenProbability AnswersKashémNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- APCO-IASC 1P01 - Winter 2019Dokument8 SeitenAPCO-IASC 1P01 - Winter 2019KashémNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Running Head: FINAL PROJECTDokument11 SeitenRunning Head: FINAL PROJECTKashémNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Assignment 1Dokument1 SeiteAssignment 1KashémNoch keine Bewertungen

- Advanced Topics in Accounting ResearchDokument6 SeitenAdvanced Topics in Accounting ResearchKashémNoch keine Bewertungen

- SWOT Analysis Future PLCDokument6 SeitenSWOT Analysis Future PLCKashémNoch keine Bewertungen

- Mzizi 6 Pages 5 Pages Karuks Martin - 4 Pages Sly Project Alvin - 2019 Fy Report Bradley - 2pgsDokument1 SeiteMzizi 6 Pages 5 Pages Karuks Martin - 4 Pages Sly Project Alvin - 2019 Fy Report Bradley - 2pgsKashémNoch keine Bewertungen

- Business and ManagementDokument12 SeitenBusiness and ManagementKashémNoch keine Bewertungen

- Health & Safety Committee Meeting Minutes: Members PresentDokument3 SeitenHealth & Safety Committee Meeting Minutes: Members PresentKashémNoch keine Bewertungen

- Breakdown TTM 9/29/2019 9/29/2018 9/29/2017: Operating Income or LossDokument4 SeitenBreakdown TTM 9/29/2019 9/29/2018 9/29/2017: Operating Income or LossKashémNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Business StatisticsDokument7 SeitenBusiness StatisticsKashémNoch keine Bewertungen

- Running Head: The Extended MetaphorDokument3 SeitenRunning Head: The Extended MetaphorKashémNoch keine Bewertungen

- General QuestionsDokument26 SeitenGeneral Questionskumarbcomca0% (1)

- Pay Slip - 607043 - Jun-22Dokument1 SeitePay Slip - 607043 - Jun-22Supriya KandukuriNoch keine Bewertungen

- Illustration On Special Revenue FundDokument2 SeitenIllustration On Special Revenue FundJichang Hik0% (1)

- Chapter 2Dokument9 SeitenChapter 2Sheilamae Sernadilla GregorioNoch keine Bewertungen

- FIS Global Solutions Philippines Payslip For: 01 Apr 2019 To 15 Apr 2019Dokument1 SeiteFIS Global Solutions Philippines Payslip For: 01 Apr 2019 To 15 Apr 2019Zyrha ZelrineNoch keine Bewertungen

- IntxDokument6 SeitenIntxSophia KeratinNoch keine Bewertungen

- Worksheet 14 5.2 TaxationDokument2 SeitenWorksheet 14 5.2 TaxationMuhammad Fareed0% (1)

- AUDITOFINTANGIBLESDokument5 SeitenAUDITOFINTANGIBLESPar Cor0% (1)

- Itr 4 Sugam - Indian Income Tax Return: Acknowledgement Number: 986260850020121 Assessment Year: 2020-21Dokument10 SeitenItr 4 Sugam - Indian Income Tax Return: Acknowledgement Number: 986260850020121 Assessment Year: 2020-21PANKAJ KOTHARINoch keine Bewertungen

- CORRECTED (If Checked) : Nonemployee CompensationDokument2 SeitenCORRECTED (If Checked) : Nonemployee CompensationNathalin De IsoldiNoch keine Bewertungen

- The Imperial College of Australia: SIT60316 BSBFIM601 Advanced Diploma of Hospitality Management Manage FinancesDokument18 SeitenThe Imperial College of Australia: SIT60316 BSBFIM601 Advanced Diploma of Hospitality Management Manage Financesosama najmiNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Notification For Departmental Examination 2022 ITO Inspector 14-9-22Dokument12 SeitenNotification For Departmental Examination 2022 ITO Inspector 14-9-22Piyush GautamNoch keine Bewertungen

- Income Tax On Individuals Part 2Dokument22 SeitenIncome Tax On Individuals Part 2mmhNoch keine Bewertungen

- On June 15 201 1 A Second Hand Machine Was Purchased For 77 000Dokument1 SeiteOn June 15 201 1 A Second Hand Machine Was Purchased For 77 000Let's Talk With HassanNoch keine Bewertungen

- TaxDokument7 SeitenTaxSaloni Jain 1820343Noch keine Bewertungen

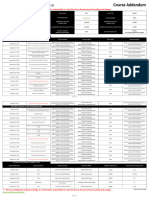

- Fall 2023 ACC400 NKK Course AddendumDokument2 SeitenFall 2023 ACC400 NKK Course AddendumGKNoch keine Bewertungen

- Maharshi ParikhDokument3 SeitenMaharshi Parikhsanket shahNoch keine Bewertungen

- TaxDokument6 SeitenTaxcathom100Noch keine Bewertungen

- Tds Challan 281 Nov'2021Dokument6 SeitenTds Challan 281 Nov'2021tojendra laltenNoch keine Bewertungen

- The Revenue/Receivables/Cash Cycle: HapterDokument48 SeitenThe Revenue/Receivables/Cash Cycle: HapterYukiNoch keine Bewertungen

- SAP US Payroll Tax - Well ExplainedDokument45 SeitenSAP US Payroll Tax - Well ExplainedSuren Reddy67% (15)

- 0 Control Sheet - Charge of Tax & 4 Key ConceptsDokument1 Seite0 Control Sheet - Charge of Tax & 4 Key ConceptsArman KhanNoch keine Bewertungen

- Santander - Brazil Fiscal Policy - Fiscal X-RayDokument9 SeitenSantander - Brazil Fiscal Policy - Fiscal X-RayIgor EnnesNoch keine Bewertungen

- Computations of VATDokument21 SeitenComputations of VATMikee TanNoch keine Bewertungen

- Tax2 - Estate Donors VAT ReviewerDokument3 SeitenTax2 - Estate Donors VAT ReviewercardeguzmanNoch keine Bewertungen

- Solved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)Dokument45 SeitenSolved Past Papers Income Tax Numericals of ICMAP STAGE IV - (2003 TO 2015)muneeb razaNoch keine Bewertungen

- Tax Finals Summative s01Dokument4 SeitenTax Finals Summative s01Von Andrei Medina100% (1)

- Some Important Aspects of HUF Under Income Tax, 1961Dokument16 SeitenSome Important Aspects of HUF Under Income Tax, 1961phani raja kumarNoch keine Bewertungen

- Imposto de Renda em InglesDokument5 SeitenImposto de Renda em InglesIago MartinsNoch keine Bewertungen

- Ghana Revenue Authority: Monthly Vat & Nhil Flat Rate ReturnDokument2 SeitenGhana Revenue Authority: Monthly Vat & Nhil Flat Rate Returnokatakyie1990Noch keine Bewertungen

- How to Estimate with RSMeans Data: Basic Skills for Building ConstructionVon EverandHow to Estimate with RSMeans Data: Basic Skills for Building ConstructionBewertung: 4.5 von 5 Sternen4.5/5 (2)

- A Place of My Own: The Architecture of DaydreamsVon EverandA Place of My Own: The Architecture of DaydreamsBewertung: 4 von 5 Sternen4/5 (242)

- The Complete Guide to Building Your Own Home and Saving Thousands on Your New HouseVon EverandThe Complete Guide to Building Your Own Home and Saving Thousands on Your New HouseBewertung: 5 von 5 Sternen5/5 (3)

- Welding for Beginners in Fabrication: The Essentials of the Welding CraftVon EverandWelding for Beginners in Fabrication: The Essentials of the Welding CraftBewertung: 5 von 5 Sternen5/5 (5)

- Field Guide for Construction Management: Management by Walking AroundVon EverandField Guide for Construction Management: Management by Walking AroundBewertung: 4.5 von 5 Sternen4.5/5 (3)

- The Everything Woodworking Book: A Beginner's Guide To Creating Great Projects From Start To FinishVon EverandThe Everything Woodworking Book: A Beginner's Guide To Creating Great Projects From Start To FinishBewertung: 4 von 5 Sternen4/5 (3)

- Pressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedVon EverandPressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedBewertung: 5 von 5 Sternen5/5 (1)