Das könnte Ihnen auch gefallen

- PUBLIC FINANCE MACRODokument8 SeitenPUBLIC FINANCE MACROAchik Che RahimiNoch keine Bewertungen

- Banking Sample Paper - Key Audit ProceduresDokument32 SeitenBanking Sample Paper - Key Audit Procedurescima2k15Noch keine Bewertungen

- Design and Analysis of Low Cost Multi Stored Building Using Staad ProDokument131 SeitenDesign and Analysis of Low Cost Multi Stored Building Using Staad ProShaik ZuberNoch keine Bewertungen

- Eco211 210 164 219Dokument10 SeitenEco211 210 164 219RazakSengkoNoch keine Bewertungen

- TC Tie Back Staad Pro AnalysisDokument13 SeitenTC Tie Back Staad Pro AnalysisyipchenghongNoch keine Bewertungen

- Inflation & Unemploy Ment: Lecturer: Pn. Azizah Isa 1Dokument50 SeitenInflation & Unemploy Ment: Lecturer: Pn. Azizah Isa 1hariprem26100% (1)

- Contract law: Postal rule and revocation of offerDokument42 SeitenContract law: Postal rule and revocation of offerMuhammad Rezza Ghazali50% (4)

- STAADDokument51 SeitenSTAADsravanNoch keine Bewertungen

- Prep Suggested Answer 1Dokument5 SeitenPrep Suggested Answer 1xjfdfjdjdNoch keine Bewertungen

- Thursday, August 06, 2020, 02:29 PM: Page 1 of 135 C:/Users/Rose/Desktop/work/Structure1.anlDokument135 SeitenThursday, August 06, 2020, 02:29 PM: Page 1 of 135 C:/Users/Rose/Desktop/work/Structure1.anlKamille Anne GabaynoNoch keine Bewertungen

- Sample Answer LAWDokument3 SeitenSample Answer LAWIzzat AsyrafNoch keine Bewertungen

- Staad OutputDokument7 SeitenStaad OutputRobbyTeresaNoch keine Bewertungen

- Computer Aided Analysis of Building StructuresDokument49 SeitenComputer Aided Analysis of Building StructuresAHSANNoch keine Bewertungen

- STAAD Pro Training Chandigarh - StaadDokument2 SeitenSTAAD Pro Training Chandigarh - StaadGaurav BargujarNoch keine Bewertungen

- Convergence Towards Ifrs in Malaysia Issues Challenges and OpportunitiesDokument5 SeitenConvergence Towards Ifrs in Malaysia Issues Challenges and OpportunitiesElaine NewNoch keine Bewertungen

- Facade design structural analysis reportDokument22 SeitenFacade design structural analysis reportsravanNoch keine Bewertungen

- Forces in Statically Determinate TrussDokument10 SeitenForces in Statically Determinate TrussFarrukhNoch keine Bewertungen

- ABC Company Year-End Trial BalanceDokument8 SeitenABC Company Year-End Trial Balancetom quevreuxNoch keine Bewertungen

- 8 - Structural WallsDokument37 Seiten8 - Structural Wallskenny lie100% (1)

- Eco211 210 164 219Dokument10 SeitenEco211 210 164 219Ana MuslimahNoch keine Bewertungen

- Faculty of Science Computer and MathematicsDokument29 SeitenFaculty of Science Computer and MathematicsNabilah Musri98Noch keine Bewertungen

- Industrial Building Design FactorsDokument59 SeitenIndustrial Building Design FactorsPhuong ThaoNoch keine Bewertungen

- Historical Development of AccountingDokument25 SeitenHistorical Development of AccountingstrifehartNoch keine Bewertungen

- Training Manual - 2 - 3 Workshop - 1Dokument54 SeitenTraining Manual - 2 - 3 Workshop - 1tigersronnieNoch keine Bewertungen

- Bukit Villa Design ReportDokument23 SeitenBukit Villa Design ReportKevin LowNoch keine Bewertungen

- Impact of FDI On Indian Economy: Term Paper On Financial SystemDokument19 SeitenImpact of FDI On Indian Economy: Term Paper On Financial SystempintuNoch keine Bewertungen

- Procedure For Water Submission - 010515Dokument21 SeitenProcedure For Water Submission - 010515mushroom0320Noch keine Bewertungen

- Difference BTW Micro & Macro EconDokument5 SeitenDifference BTW Micro & Macro EconshyasirNoch keine Bewertungen

- High Rise1Dokument18 SeitenHigh Rise1Annamalai VaidyanathanNoch keine Bewertungen

- ECS478 CHAPTER 3-Flat SlabDokument40 SeitenECS478 CHAPTER 3-Flat SlabAmron Abubakar0% (1)

- Client'S Portfolio Management: ASB KochiDokument17 SeitenClient'S Portfolio Management: ASB KochiDeepa RaghuNoch keine Bewertungen

- Staad Pro Level 1 - Ecc IndiaDokument3 SeitenStaad Pro Level 1 - Ecc IndiaMitaNoch keine Bewertungen

- Assignment 2 - FramesDokument12 SeitenAssignment 2 - FramesZazliana Izatti100% (1)

- Lecture:1&2 (Reinforced Concrete Structures) : Introduction To The SubjectDokument16 SeitenLecture:1&2 (Reinforced Concrete Structures) : Introduction To The SubjectMuhammad UmarNoch keine Bewertungen

- Introduction to Wavelets -part 2: Wavelet Transform, CWT, DWT, 2D SignalsDokument59 SeitenIntroduction to Wavelets -part 2: Wavelet Transform, CWT, DWT, 2D Signalssm-malikNoch keine Bewertungen

- Learn Flat Slab Software Step-by-Step GuideDokument128 SeitenLearn Flat Slab Software Step-by-Step GuideMohammad FawwazNoch keine Bewertungen

- Shallow FoundationDokument80 SeitenShallow FoundationMasyitah IrfanNoch keine Bewertungen

- Analysis of a G+30 Building Using STAAD.PRODokument4 SeitenAnalysis of a G+30 Building Using STAAD.PROShaikh Muhammad AteeqNoch keine Bewertungen

- Applied Mechanics CH 1Dokument11 SeitenApplied Mechanics CH 1Tushar KiranNoch keine Bewertungen

- Staad Pro-Different Floor LoadsDokument28 SeitenStaad Pro-Different Floor LoadsV.m. Rajan100% (1)

- Pricol Limited - Broker Research - 2017 PDFDokument25 SeitenPricol Limited - Broker Research - 2017 PDFnishthaNoch keine Bewertungen

- Shipping Container 2 14.04.2022Dokument45 SeitenShipping Container 2 14.04.2022Atul Kumar EngineerNoch keine Bewertungen

- Concrete DesignDokument78 SeitenConcrete Designongora geoffreyNoch keine Bewertungen

- Bus Stop Steel FinalDokument33 SeitenBus Stop Steel FinalanuarNoch keine Bewertungen

- Chapter 2.0 - Structural AnalysisDokument31 SeitenChapter 2.0 - Structural Analysisfaraeiin57Noch keine Bewertungen

- EQTip 22Dokument2 SeitenEQTip 22boubressNoch keine Bewertungen

- Topic2 - Force Method of Analysis FramesDokument19 SeitenTopic2 - Force Method of Analysis FramesMary Joanne Capacio AniñonNoch keine Bewertungen

- Column Design - As Per BS8110Dokument16 SeitenColumn Design - As Per BS8110Parthiban ArivazhaganNoch keine Bewertungen

- Analysis and Design of A Combined Triangular Shaped Pile Cap Due To Pile EccentricityDokument7 SeitenAnalysis and Design of A Combined Triangular Shaped Pile Cap Due To Pile Eccentricityazhar ahmad100% (1)

- Surau As SyddiqDokument1 SeiteSurau As SyddiqAnas SuhaibNoch keine Bewertungen

- Coupling BeamDokument45 SeitenCoupling Beamgreen77parkNoch keine Bewertungen

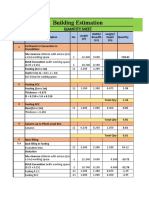

- Building EstimationDokument22 SeitenBuilding EstimationMelkamu AmusheNoch keine Bewertungen

- MTIDokument14 SeitenMTIavinas@333Noch keine Bewertungen

- Eco-Friendly Raft Pile System, Innovative Solution For Soft Soil Problem (2012) - DID PDFDokument16 SeitenEco-Friendly Raft Pile System, Innovative Solution For Soft Soil Problem (2012) - DID PDFDuan YuNoch keine Bewertungen

- Credit Creation: Balance Sheet 1Dokument5 SeitenCredit Creation: Balance Sheet 1Tanim BegNoch keine Bewertungen

- Notes - Unit 2 - Money and BankingDokument3 SeitenNotes - Unit 2 - Money and Banking0mega YTNoch keine Bewertungen

- Money and Financial SystemDokument37 SeitenMoney and Financial SystemTheresiaNoch keine Bewertungen

- Mankiw - Money and Finansial SystemDokument37 SeitenMankiw - Money and Finansial SystemBRYAN SIANDRYNoch keine Bewertungen

- Frictional & Instrumen Kebij MoneterDokument41 SeitenFrictional & Instrumen Kebij MoneterBagus GilangNoch keine Bewertungen

- (Lecture 8.1) Chapter 11 Money and Financial System (L8)Dokument28 Seiten(Lecture 8.1) Chapter 11 Money and Financial System (L8)Chen Yee KhooNoch keine Bewertungen

- Central Banking and The Effects of Its Monetary Policies in Our EconomyDokument42 SeitenCentral Banking and The Effects of Its Monetary Policies in Our EconomyHannah LegaspiNoch keine Bewertungen

- Money and the Economy: Understanding Financial Assets and IntermediationDokument4 SeitenMoney and the Economy: Understanding Financial Assets and IntermediationJoshua CortezNoch keine Bewertungen

- Teaching Money Creation and Monetary PolicyDokument21 SeitenTeaching Money Creation and Monetary PolicyJuan Diego González Bustillo100% (1)

- Tche 303 - Money and Banking Tutorial 9: CurrencyDokument4 SeitenTche 303 - Money and Banking Tutorial 9: CurrencyNguyen VyNoch keine Bewertungen

- Monetary Policy Review in PakistanDokument2 SeitenMonetary Policy Review in PakistanLaiba EjazNoch keine Bewertungen

- Reserve Bank of IndiaDokument21 SeitenReserve Bank of IndiaAcchu BajajNoch keine Bewertungen

- Economics Money and Banking Worksheet Set BDokument6 SeitenEconomics Money and Banking Worksheet Set Bdennis greenNoch keine Bewertungen

- Monetary Policy Meaning, Types, and ToolsDokument6 SeitenMonetary Policy Meaning, Types, and ToolsVenkat SaiNoch keine Bewertungen

- Role of Rbi in Controlling Money Supply in IndiaDokument18 SeitenRole of Rbi in Controlling Money Supply in Indiaarpita banerjeeNoch keine Bewertungen

- State Bank of PakistanDokument27 SeitenState Bank of PakistanAbdul MoizNoch keine Bewertungen

- Personal Investments and Monetary PolicyDokument45 SeitenPersonal Investments and Monetary PolicySikandar KhattakNoch keine Bewertungen

- BFB4133 Financial Markets and Institutions Course NotesDokument101 SeitenBFB4133 Financial Markets and Institutions Course NotesMakisha NishaNoch keine Bewertungen

- The Monetary System: Solutions To Textbook ProblemsDokument9 SeitenThe Monetary System: Solutions To Textbook ProblemsMainland FounderNoch keine Bewertungen

- The Fed and Monetary PolicyDokument27 SeitenThe Fed and Monetary PolicyAnonymous taCBG1AKaNoch keine Bewertungen

- Bank LiquidityDokument17 SeitenBank Liquidityahsan habibNoch keine Bewertungen

- Central Bank Functions and Monetary Policy ToolsDokument9 SeitenCentral Bank Functions and Monetary Policy ToolsBushra HaqueNoch keine Bewertungen

- BankingDokument49 SeitenBankingRitu BhatiyaNoch keine Bewertungen

- Econ 100.1 - Problem Set 5 - AnswerDokument2 SeitenEcon 100.1 - Problem Set 5 - AnsweryebbakarlNoch keine Bewertungen

- Extra Materials To Topic4Dokument3 SeitenExtra Materials To Topic4КатеринаNoch keine Bewertungen

- State Bank of Pakistan Central Bank Role, Functions & Monetary Policy ToolsDokument25 SeitenState Bank of Pakistan Central Bank Role, Functions & Monetary Policy ToolsTariq Abbasi50% (2)

- The Economics of Money, Banking, and Financial Markets: Twelfth Edition, Global EditionDokument34 SeitenThe Economics of Money, Banking, and Financial Markets: Twelfth Edition, Global Editionsawmon myintNoch keine Bewertungen

- Monetary Policy and Role of Its InstrumentsDokument23 SeitenMonetary Policy and Role of Its Instrumentsbhargavchotu15534Noch keine Bewertungen

- Final Project On WCMDokument51 SeitenFinal Project On WCMAnup KulkarniNoch keine Bewertungen

- Topic-5-The Monetary SystemDokument15 SeitenTopic-5-The Monetary Systemlehahai1802Noch keine Bewertungen

- Money, Banking and International TradeDokument228 SeitenMoney, Banking and International TradeRashmiNoch keine Bewertungen

- G1 Determinants of Bank Lending in NepalDokument24 SeitenG1 Determinants of Bank Lending in NepalSuman PoudelNoch keine Bewertungen

- ND 2 BFN Financial Institutions Lectures 2023Dokument20 SeitenND 2 BFN Financial Institutions Lectures 2023sanusi bello bakuraNoch keine Bewertungen

- Test Bank For Busn 11th Edition Marcella Kelly Chuck WilliamsDokument30 SeitenTest Bank For Busn 11th Edition Marcella Kelly Chuck WilliamsJoseph Ellison100% (33)

- Practice Final Winter 2014Dokument38 SeitenPractice Final Winter 2014Locklaim CardinozaNoch keine Bewertungen