Das könnte Ihnen auch gefallen

- Excel Crash CourseDokument3 SeitenExcel Crash CourseAniya SharmaNoch keine Bewertungen

- 3 A Sanitary Standards Quick Reference GuideDokument98 Seiten3 A Sanitary Standards Quick Reference GuideLorettaMayNoch keine Bewertungen

- Instruction Manual Twin Lobe CompressorDokument10 SeitenInstruction Manual Twin Lobe Compressorvsaagar100% (1)

- Management Science Chapter 10Dokument44 SeitenManagement Science Chapter 10Myuran SivarajahNoch keine Bewertungen

- Math 006B - Module 4 HypothesisDokument4 SeitenMath 006B - Module 4 Hypothesisaey de guzmanNoch keine Bewertungen

- Quiz Acctng 603Dokument10 SeitenQuiz Acctng 603LJ AggabaoNoch keine Bewertungen

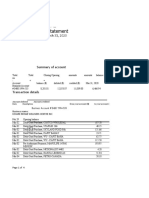

- Bank StatementDokument14 SeitenBank StatementLJ AggabaoNoch keine Bewertungen

- CPAR87 Final PB - AFARDokument15 SeitenCPAR87 Final PB - AFARLJ AggabaoNoch keine Bewertungen

- Best of The Photo DetectiveDokument55 SeitenBest of The Photo DetectiveSazeed Hossain100% (3)

- A Quantitative Method For Evaluation of CAT Tools Based On User Preferences. Anna ZaretskayaDokument5 SeitenA Quantitative Method For Evaluation of CAT Tools Based On User Preferences. Anna ZaretskayaplanetalinguaNoch keine Bewertungen

- INSTALLMENTDokument3 SeitenINSTALLMENTEdison L. ChuNoch keine Bewertungen

- AP Equity 1Dokument3 SeitenAP Equity 1Mark Michael Legaspi100% (1)

- 3.3 Exercise - Improperly Accumulated Earnings TaxDokument2 Seiten3.3 Exercise - Improperly Accumulated Earnings TaxRenzo KarununganNoch keine Bewertungen

- CA 04 - Job Order CostingDokument17 SeitenCA 04 - Job Order CostingJoshua UmaliNoch keine Bewertungen

- Repair Cost Probabilit yDokument2 SeitenRepair Cost Probabilit yNicole AguinaldoNoch keine Bewertungen

- D15Dokument12 SeitenD15neo14Noch keine Bewertungen

- Identify The Choice That Best Completes The Statement or Answers The QuestionDokument5 SeitenIdentify The Choice That Best Completes The Statement or Answers The QuestionErine ContranoNoch keine Bewertungen

- HW On Operating Segments BDokument3 SeitenHW On Operating Segments BJazehl Joy ValdezNoch keine Bewertungen

- Cost Quiz 3Dokument5 SeitenCost Quiz 3Jerric CristobalNoch keine Bewertungen

- Prelim Exam Aud Prob ReviewDokument2 SeitenPrelim Exam Aud Prob ReviewgbenjielizonNoch keine Bewertungen

- MAS - 1416 Profit Planning - CVP AnalysisDokument24 SeitenMAS - 1416 Profit Planning - CVP AnalysisAzureBlazeNoch keine Bewertungen

- Mas Drills Weeks 1 5Dokument28 SeitenMas Drills Weeks 1 5Hermz ComzNoch keine Bewertungen

- Standard Costs and Variance Analysis Standard Costs and Variance AnalysisDokument26 SeitenStandard Costs and Variance Analysis Standard Costs and Variance Analysischiji chzzzmeowNoch keine Bewertungen

- Cost Concepts, Classification and Segregation: M.S.M.CDokument7 SeitenCost Concepts, Classification and Segregation: M.S.M.CAllen CarlNoch keine Bewertungen

- 162 020Dokument5 Seiten162 020Angelli LamiqueNoch keine Bewertungen

- FinAcc 1 Quiz 6Dokument10 SeitenFinAcc 1 Quiz 6Kimbol Calingayan100% (1)

- Quiz No. 1 Part 3 Multiple Choice Problems Attempt ReviewDokument1 SeiteQuiz No. 1 Part 3 Multiple Choice Problems Attempt ReviewEly RiveraNoch keine Bewertungen

- Chapter 03Dokument30 SeitenChapter 03ajbalcitaNoch keine Bewertungen

- Audit of Inventory 2021 - ExamDokument9 SeitenAudit of Inventory 2021 - ExammoreNoch keine Bewertungen

- Practical Accounting 1doc PDF FreeDokument6 SeitenPractical Accounting 1doc PDF FreeRovern Keith Oro CuencaNoch keine Bewertungen

- Test 5Dokument2 SeitenTest 5Kim LimosneroNoch keine Bewertungen

- TOA03 04 Leases Income Tax Employee Benefits CharlenesDokument3 SeitenTOA03 04 Leases Income Tax Employee Benefits CharlenesMerliza JusayanNoch keine Bewertungen

- Interim Financial Reporting: Problem 45-1: True or FalseDokument7 SeitenInterim Financial Reporting: Problem 45-1: True or FalseMarjorieNoch keine Bewertungen

- Chapter 21 - Teacher's Manual - Far Part 1BDokument19 SeitenChapter 21 - Teacher's Manual - Far Part 1BPacifico HernandezNoch keine Bewertungen

- Cost Classifications As To Product and BehaviourDokument2 SeitenCost Classifications As To Product and BehaviourJimbo ManalastasNoch keine Bewertungen

- Abc Costing IllustratedDokument2 SeitenAbc Costing IllustratedBryan FloresNoch keine Bewertungen

- Lesson 4 Expenditure Cycle PDFDokument19 SeitenLesson 4 Expenditure Cycle PDFJoshua JunsayNoch keine Bewertungen

- RFBT Quiz 1: Forgery. After Giving A Notice of Dishonor, Which of The Following Is Not Correct?Dokument7 SeitenRFBT Quiz 1: Forgery. After Giving A Notice of Dishonor, Which of The Following Is Not Correct?cheni magsaelNoch keine Bewertungen

- Adms 2510 Winter 2007 Final ExaminationDokument11 SeitenAdms 2510 Winter 2007 Final ExaminationMohsin Rehman0% (1)

- MODULE 2 CVP AnalysisDokument8 SeitenMODULE 2 CVP Analysissharielles /Noch keine Bewertungen

- LTCC AnswerDokument4 SeitenLTCC AnswerRhina MagnawaNoch keine Bewertungen

- The Purchasing/ Accounts Payable/ Cash Disbursement (P/AP/CD) ProcessDokument17 SeitenThe Purchasing/ Accounts Payable/ Cash Disbursement (P/AP/CD) ProcessJonah Mark Tabuldan DebomaNoch keine Bewertungen

- Accounting For Joint Arrangements Material 1Dokument5 SeitenAccounting For Joint Arrangements Material 1Erika Mae BarizoNoch keine Bewertungen

- Pfrs 12 Disclosure of Interest in Other EntitiesDokument26 SeitenPfrs 12 Disclosure of Interest in Other EntitiesMeiNoch keine Bewertungen

- Applied Auditing Audit of Cash and ReceivablesDokument2 SeitenApplied Auditing Audit of Cash and ReceivablesCar Mae LaNoch keine Bewertungen

- COST ACCOUNTING 1 8 Final Allocation of Joint CostsDokument15 SeitenCOST ACCOUNTING 1 8 Final Allocation of Joint CostsZoe MendozaNoch keine Bewertungen

- 5share OptionsDokument21 Seiten5share OptionsnengNoch keine Bewertungen

- Global CompanyDokument1 SeiteGlobal Companydagohoy kennethNoch keine Bewertungen

- Ia FifoDokument5 SeitenIa FifoNadine SofiaNoch keine Bewertungen

- Defined Benefit Plan-Midnight CompanyDokument2 SeitenDefined Benefit Plan-Midnight CompanyDyenNoch keine Bewertungen

- Dhis Special Transactions 2019 by Millan Solman PDFDokument158 SeitenDhis Special Transactions 2019 by Millan Solman PDFQueeny Mae Cantre ReutaNoch keine Bewertungen

- CH 15Dokument20 SeitenCH 15grace guiuanNoch keine Bewertungen

- MODAUD2 Unit 4 Audit of Bonds Payable T31516 FINALDokument3 SeitenMODAUD2 Unit 4 Audit of Bonds Payable T31516 FINALmimi960% (2)

- Module #6Dokument20 SeitenModule #6Joy RadaNoch keine Bewertungen

- Auditing Problem 2Dokument1 SeiteAuditing Problem 2jhobs100% (1)

- Quiz - Acts PayableDokument2 SeitenQuiz - Acts PayableAna Mae HernandezNoch keine Bewertungen

- Requirement No. 1: PROBLEM NO. 1 - Heats CorporationDokument1 SeiteRequirement No. 1: PROBLEM NO. 1 - Heats CorporationjhobsNoch keine Bewertungen

- P 1Dokument4 SeitenP 1Kenneth Bryan Tegerero TegioNoch keine Bewertungen

- Chapter 1 Acctg 5Dokument11 SeitenChapter 1 Acctg 5Angelica MayNoch keine Bewertungen

- ACC5116 - Module 1Dokument6 SeitenACC5116 - Module 1Carl Dhaniel Garcia SalenNoch keine Bewertungen

- HW On INVESTMENT PROPERTY - 1Dokument2 SeitenHW On INVESTMENT PROPERTY - 1Charles TuazonNoch keine Bewertungen

- Intangible Assets Assignment - No Answers - For PostingDokument2 SeitenIntangible Assets Assignment - No Answers - For Postingemman neriNoch keine Bewertungen

- Abm QuizDokument5 SeitenAbm QuizCastleclash CastleclashNoch keine Bewertungen

- Module 1 InventoryDokument57 SeitenModule 1 InventoryA. MagnoNoch keine Bewertungen

- AFAR Assessment 2Dokument5 SeitenAFAR Assessment 2JoshelBuenaventuraNoch keine Bewertungen

- ReSA B44 AFAR First PB Exam Questions Answers SolutionsDokument22 SeitenReSA B44 AFAR First PB Exam Questions Answers SolutionsWes100% (1)

- Advance AccountingDokument5 SeitenAdvance AccountingChristopher PriceNoch keine Bewertungen

- ASSIGNMENTDokument4 SeitenASSIGNMENTLJ AggabaoNoch keine Bewertungen

- Income: Cancelled Checks For The Month of February 2022Dokument1 SeiteIncome: Cancelled Checks For The Month of February 2022LJ AggabaoNoch keine Bewertungen

- Government Accounting Exam PhilippinesDokument4 SeitenGovernment Accounting Exam PhilippinesLJ Aggabao100% (1)

- Hospital Revenues (1-32)Dokument13 SeitenHospital Revenues (1-32)LJ AggabaoNoch keine Bewertungen

- Statement of Management ResponsibilityDokument1 SeiteStatement of Management ResponsibilityLJ AggabaoNoch keine Bewertungen

- Republic of The Philippines Department of Health Southern Isabela Medical CenterDokument2 SeitenRepublic of The Philippines Department of Health Southern Isabela Medical CenterLJ AggabaoNoch keine Bewertungen

- Nature of Government AccountingDokument16 SeitenNature of Government AccountingLJ AggabaoNoch keine Bewertungen

- PLDT RecieptDokument2 SeitenPLDT RecieptLJ AggabaoNoch keine Bewertungen

- Age at The Onsent of Disease: GenderDokument5 SeitenAge at The Onsent of Disease: GenderLJ AggabaoNoch keine Bewertungen

- Law 101-The Law On Obligation and Contracts: Prelims Dterms FinalsDokument2 SeitenLaw 101-The Law On Obligation and Contracts: Prelims Dterms FinalsLJ AggabaoNoch keine Bewertungen

- Leave Revised FloricelDokument2 SeitenLeave Revised FloricelLJ AggabaoNoch keine Bewertungen

- Forced Leave LetterDokument1 SeiteForced Leave LetterLJ AggabaoNoch keine Bewertungen

- CDU MeetingDokument1 SeiteCDU MeetingLJ AggabaoNoch keine Bewertungen

- Govt. Accting QuizDokument5 SeitenGovt. Accting QuizLJ AggabaoNoch keine Bewertungen

- Advanced Accounting Chapter 19Dokument14 SeitenAdvanced Accounting Chapter 19LJ AggabaoNoch keine Bewertungen

- Advanced Accounting Chapter 21Dokument9 SeitenAdvanced Accounting Chapter 21LJ AggabaoNoch keine Bewertungen

- Ed Memo No. 93 Fy 2020 2021 Annex A Revised Dpa Picpa CandidateDokument9 SeitenEd Memo No. 93 Fy 2020 2021 Annex A Revised Dpa Picpa CandidateLJ AggabaoNoch keine Bewertungen

- Lorena Joy M. Aggabao 3/7/2022Dokument1 SeiteLorena Joy M. Aggabao 3/7/2022LJ AggabaoNoch keine Bewertungen

- Seatwork Joint ArrangementsDokument1 SeiteSeatwork Joint ArrangementsLJ AggabaoNoch keine Bewertungen

- Blistt Health Declaration FormDokument1 SeiteBlistt Health Declaration Formluningning0007100% (1)

- Advanced Accounting Chapter 22Dokument9 SeitenAdvanced Accounting Chapter 22LJ AggabaoNoch keine Bewertungen

- Advanced Accounting Chapter 22Dokument9 SeitenAdvanced Accounting Chapter 22LJ AggabaoNoch keine Bewertungen

- Advanced Accounting Chapter 21Dokument9 SeitenAdvanced Accounting Chapter 21LJ AggabaoNoch keine Bewertungen

- Advanced Accounting Chapter 20Dokument12 SeitenAdvanced Accounting Chapter 20LJ AggabaoNoch keine Bewertungen

- Illustrative Problem-Installment SalesDokument2 SeitenIllustrative Problem-Installment SalesLJ AggabaoNoch keine Bewertungen

- Advanced Accounting Chapter 19Dokument14 SeitenAdvanced Accounting Chapter 19LJ AggabaoNoch keine Bewertungen

- Final PB87 Sol. AFAR PDFDokument9 SeitenFinal PB87 Sol. AFAR PDFLJ AggabaoNoch keine Bewertungen

- A Short History of Denim: (C) Lynn Downey, Levi Strauss & Co. HistorianDokument11 SeitenA Short History of Denim: (C) Lynn Downey, Levi Strauss & Co. HistorianBoier Sesh PataNoch keine Bewertungen

- Module 4 How To Make Self-Rescue Evacuation Maps?Dokument85 SeitenModule 4 How To Make Self-Rescue Evacuation Maps?RejieNoch keine Bewertungen

- Enhancing Guest Experience and Operational Efficiency in Hotels Through Robotic Technology-A Comprehensive Review.Dokument8 SeitenEnhancing Guest Experience and Operational Efficiency in Hotels Through Robotic Technology-A Comprehensive Review.Chandigarh PhilosophersNoch keine Bewertungen

- Zkp8006 Posperu Inc SacDokument2 SeitenZkp8006 Posperu Inc SacANDREA BRUNO SOLANONoch keine Bewertungen

- The Consulting Industry and Its Transformations in WordDokument23 SeitenThe Consulting Industry and Its Transformations in Wordlei ann magnayeNoch keine Bewertungen

- Adhesive Film & TapeDokument6 SeitenAdhesive Film & TapeJothi Vel MuruganNoch keine Bewertungen

- Technical and Business WritingDokument3 SeitenTechnical and Business WritingMuhammad FaisalNoch keine Bewertungen

- ENG 102 Essay PromptDokument2 SeitenENG 102 Essay Promptarshia winNoch keine Bewertungen

- Micronet TMRDokument316 SeitenMicronet TMRHaithem BrebishNoch keine Bewertungen

- Wordbank 15 Youtube Writeabout1Dokument2 SeitenWordbank 15 Youtube Writeabout1Olga VaizburgNoch keine Bewertungen

- 12 Constructor and DistructorDokument15 Seiten12 Constructor and DistructorJatin BhasinNoch keine Bewertungen

- Matokeo CBDokument4 SeitenMatokeo CBHubert MubofuNoch keine Bewertungen

- One Foot in The Grave - Copy For PlayersDokument76 SeitenOne Foot in The Grave - Copy For Playerssveni meierNoch keine Bewertungen

- 762id - Development of Cluster-7 Marginal Field Paper To PetrotechDokument2 Seiten762id - Development of Cluster-7 Marginal Field Paper To PetrotechSATRIONoch keine Bewertungen

- Onco Case StudyDokument2 SeitenOnco Case StudyAllenNoch keine Bewertungen

- DS SX1280-1-2 V3.0Dokument143 SeitenDS SX1280-1-2 V3.0bkzzNoch keine Bewertungen

- MSDS Charcoal Powder PDFDokument3 SeitenMSDS Charcoal Powder PDFSelina VdexNoch keine Bewertungen

- Unit 2 Operations of PolynomialsDokument28 SeitenUnit 2 Operations of Polynomialsapi-287816312Noch keine Bewertungen

- Capital Structure and Leverage: Multiple Choice: ConceptualDokument53 SeitenCapital Structure and Leverage: Multiple Choice: ConceptualArya StarkNoch keine Bewertungen

- Sco 8th Class Paper - B Jee-Main Wtm-15 Key&Solutions Exam DT 17-12-2022Dokument4 SeitenSco 8th Class Paper - B Jee-Main Wtm-15 Key&Solutions Exam DT 17-12-2022Udaya PrathimaNoch keine Bewertungen

- Eco EssayDokument3 SeitenEco EssaymanthanNoch keine Bewertungen

- Fish Culture in Ponds: Extension Bulletin No. 103Dokument32 SeitenFish Culture in Ponds: Extension Bulletin No. 103Bagas IndiantoNoch keine Bewertungen

- When I Was A ChildDokument2 SeitenWhen I Was A Childapi-636173534Noch keine Bewertungen

- Maintenance Performance ToolboxDokument6 SeitenMaintenance Performance ToolboxMagda ScrobotaNoch keine Bewertungen

- Polyembryony &its ImportanceDokument17 SeitenPolyembryony &its ImportanceSURIYA PRAKASH GNoch keine Bewertungen

- Chapter 5 - Amino acids and Proteins: Trần Thị Minh ĐứcDokument59 SeitenChapter 5 - Amino acids and Proteins: Trần Thị Minh ĐứcNguyễn SunNoch keine Bewertungen