Das könnte Ihnen auch gefallen

- Basics of SyscohadaDokument5 SeitenBasics of Syscohadapg0utamNoch keine Bewertungen

- Chapter 11 Test Bank PDFDokument29 SeitenChapter 11 Test Bank PDFYing LiuNoch keine Bewertungen

- Auditibg Problems Purchase CommitmentDokument1 SeiteAuditibg Problems Purchase Commitmentnivea gumayagay0% (1)

- QUIZ REVIEW Homework Tutorial Chapter 5Dokument5 SeitenQUIZ REVIEW Homework Tutorial Chapter 5Cody TarantinoNoch keine Bewertungen

- CFAS Module 1 - ReviewerRRRDokument4 SeitenCFAS Module 1 - ReviewerRRRAthena LedesmaNoch keine Bewertungen

- Identify The Choice That Best Completes The Statement or Answers The QuestionDokument5 SeitenIdentify The Choice That Best Completes The Statement or Answers The QuestionErwin Labayog MedinaNoch keine Bewertungen

- Afar IcpaDokument6 SeitenAfar IcpaAndrea Lyn Salonga CacayNoch keine Bewertungen

- Q06A Audit of Non Cash AssetsDokument7 SeitenQ06A Audit of Non Cash AssetsChristine Jane ParroNoch keine Bewertungen

- Accounting ProbDokument2 SeitenAccounting ProbLino GumpalNoch keine Bewertungen

- Use The Following Information For The Next Four QuestionsDokument1 SeiteUse The Following Information For The Next Four QuestionsTine Vasiana DuermeNoch keine Bewertungen

- Gialogo, Jessie Lyn San Sebastian College - Recoletos Quiz: Required: Answer The FollowingDokument12 SeitenGialogo, Jessie Lyn San Sebastian College - Recoletos Quiz: Required: Answer The FollowingMeidrick Rheeyonie Gialogo AlbaNoch keine Bewertungen

- MAS - Group 5Dokument7 SeitenMAS - Group 5beleky watersNoch keine Bewertungen

- Practical Accounting 1Dokument21 SeitenPractical Accounting 1Christine Nicole BacoNoch keine Bewertungen

- Saint Joseph College of Sindangan Incorporated College of AccountancyDokument18 SeitenSaint Joseph College of Sindangan Incorporated College of AccountancyRendall Craig Refugio0% (1)

- Cel 1 Prac 1 Answer KeyDokument15 SeitenCel 1 Prac 1 Answer KeyNJ MondigoNoch keine Bewertungen

- 162 005Dokument1 Seite162 005Angelli LamiqueNoch keine Bewertungen

- Coursehero 12Dokument2 SeitenCoursehero 12nhbNoch keine Bewertungen

- Audit of IntangiblesDokument2 SeitenAudit of IntangiblesJaycee FabriagNoch keine Bewertungen

- Prac 1Dokument9 SeitenPrac 1rayNoch keine Bewertungen

- QuizDokument2 SeitenQuizAlyssa CamposNoch keine Bewertungen

- Audit ProbDokument36 SeitenAudit ProbSheena BaylosisNoch keine Bewertungen

- Acctg 121Dokument3 SeitenAcctg 121YricaNoch keine Bewertungen

- Chapter 31SMEs Property Plant and EquipmentDokument2 SeitenChapter 31SMEs Property Plant and EquipmentDez ZaNoch keine Bewertungen

- Seatwork in Audit 2-3Dokument8 SeitenSeatwork in Audit 2-3Shr BnNoch keine Bewertungen

- 1911 Investments Investment in Associate and Bond InvestmentDokument13 Seiten1911 Investments Investment in Associate and Bond InvestmentCykee Hanna Quizo LumongsodNoch keine Bewertungen

- 2016 Vol 1 CH 8 Answers - Fin Acc SolManDokument7 Seiten2016 Vol 1 CH 8 Answers - Fin Acc SolManPamela Cruz100% (1)

- Practical Accounting 1: 2011 National Cpa Mock Board ExaminationDokument7 SeitenPractical Accounting 1: 2011 National Cpa Mock Board Examinationcacho cielo graceNoch keine Bewertungen

- Problem 17-1, ContinuedDokument6 SeitenProblem 17-1, ContinuedJohn Carlo D MedallaNoch keine Bewertungen

- AP Problems 2015Dokument20 SeitenAP Problems 2015Rodette Adajar Pajanonot100% (1)

- ADV2 Chapter12 QADokument4 SeitenADV2 Chapter12 QAMa Alyssa DelmiguezNoch keine Bewertungen

- ConsignmentDokument2 SeitenConsignmentJenica Joyce BautistaNoch keine Bewertungen

- Final 17ncDokument10 SeitenFinal 17ncKevin James Sedurifa OledanNoch keine Bewertungen

- Q Manacc1 Bep 2019Dokument5 SeitenQ Manacc1 Bep 2019Deniece RonquilloNoch keine Bewertungen

- DocxDokument10 SeitenDocxAiziel OrenseNoch keine Bewertungen

- Comprehensive Topics HandoutsDokument16 SeitenComprehensive Topics HandoutsGrace CorpoNoch keine Bewertungen

- Competency AssessmentDokument5 SeitenCompetency AssessmentMiracle FlorNoch keine Bewertungen

- Operational Performance Measurement: Further Analysis of Productivity and SalesDokument201 SeitenOperational Performance Measurement: Further Analysis of Productivity and SalesFernando III Perez0% (1)

- Apllied Auditing Q&ADokument10 SeitenApllied Auditing Q&APeterJorgeVillarante100% (2)

- Cup 3 Questions Answer KeyDokument34 SeitenCup 3 Questions Answer KeyDenmarc John AragosNoch keine Bewertungen

- What A ProblemDokument4 SeitenWhat A ProblemEleazar SalazarNoch keine Bewertungen

- FAR.2845 Statement of Profit or Loss and OCI PDFDokument6 SeitenFAR.2845 Statement of Profit or Loss and OCI PDFGabriel OrolfoNoch keine Bewertungen

- ReviewerDokument9 SeitenReviewerMarielle JoyceNoch keine Bewertungen

- On January 1Dokument3 SeitenOn January 1Jude Santos0% (1)

- Morales, Jonalyn M.Dokument7 SeitenMorales, Jonalyn M.Jonalyn MoralesNoch keine Bewertungen

- Cost To CostDokument1 SeiteCost To CostAnirban Roy ChowdhuryNoch keine Bewertungen

- National Mock Board Examination 2017 Financial Accounting and ReportingDokument9 SeitenNational Mock Board Examination 2017 Financial Accounting and ReportingSam0% (1)

- Cash BasisDokument4 SeitenCash BasisMark DiezNoch keine Bewertungen

- Estimating Ending InventoryDokument1 SeiteEstimating Ending InventorywarsidiNoch keine Bewertungen

- Multiple Choice: Choose The Best Answer Among The Choices. Write Your Answers in CAPITAL Letters. (2 Points Per Requirement)Dokument3 SeitenMultiple Choice: Choose The Best Answer Among The Choices. Write Your Answers in CAPITAL Letters. (2 Points Per Requirement)Kimmy ShawwyNoch keine Bewertungen

- (Use The Below Problem To Answers The Succeeding Four (4) Questions.)Dokument3 Seiten(Use The Below Problem To Answers The Succeeding Four (4) Questions.)Janine LerumNoch keine Bewertungen

- Chapter 3 - Seat Work - Assignment #3 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDokument5 SeitenChapter 3 - Seat Work - Assignment #3 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDonise Ronadel SantosNoch keine Bewertungen

- Equity YyyDokument33 SeitenEquity YyyJude SantosNoch keine Bewertungen

- 2018 - 2019 MAS 01 70mcqDokument30 Seiten2018 - 2019 MAS 01 70mcqMarc Allen Anthony GanNoch keine Bewertungen

- I Am Sharing 'SIM-ANSWERS - 6th-Exam-Topics - Hyperinflation - PABRES' With YouDokument9 SeitenI Am Sharing 'SIM-ANSWERS - 6th-Exam-Topics - Hyperinflation - PABRES' With YouJeric TorionNoch keine Bewertungen

- PDF ReceivablesDokument6 SeitenPDF ReceivablesJanine SarzaNoch keine Bewertungen

- AccountingDokument5 SeitenAccountingMoira C. VilogNoch keine Bewertungen

- Events After The Reporting Period NCA Held For Disposal Discontinued OperationsDokument2 SeitenEvents After The Reporting Period NCA Held For Disposal Discontinued OperationsJeremiah DavidNoch keine Bewertungen

- OPT QuizDokument5 SeitenOPT QuizAngeline VergaraNoch keine Bewertungen

- Ifrs 5 (2021)Dokument9 SeitenIfrs 5 (2021)Tawanda Tatenda HerbertNoch keine Bewertungen

- Ifr 3 1Dokument52 SeitenIfr 3 1Meo MeoNoch keine Bewertungen

- MODULE-Midterm-FAR-3-NCHFS, DO &ACDokument18 SeitenMODULE-Midterm-FAR-3-NCHFS, DO &ACJohn Mark FernandoNoch keine Bewertungen

- IA3Dokument21 SeitenIA3Jane ManahanNoch keine Bewertungen

- 162 003Dokument4 Seiten162 003Angelli LamiqueNoch keine Bewertungen

- Financial Analysis: Current Assets Current Liabilities Current RatioDokument11 SeitenFinancial Analysis: Current Assets Current Liabilities Current RatioAngelli LamiqueNoch keine Bewertungen

- 162 020Dokument5 Seiten162 020Angelli LamiqueNoch keine Bewertungen

- Accounting 162 - Material 002Dokument2 SeitenAccounting 162 - Material 002Angelli LamiqueNoch keine Bewertungen

- 162 005Dokument1 Seite162 005Angelli LamiqueNoch keine Bewertungen

- 162 019Dokument4 Seiten162 019Angelli LamiqueNoch keine Bewertungen

- 162 009Dokument2 Seiten162 009Angelli Lamique75% (4)

- 162.material.011 InventoryDokument7 Seiten162.material.011 InventoryAngelli LamiqueNoch keine Bewertungen

- Projected Statement of Financial PerformanceDokument7 SeitenProjected Statement of Financial PerformanceAngelli LamiqueNoch keine Bewertungen

- Fs Chapter 3 EditedDokument10 SeitenFs Chapter 3 EditedAngelli LamiqueNoch keine Bewertungen

- Baasco Audit Manual Oraganizational Chart: Research and Development Analysis ReviewDokument1 SeiteBaasco Audit Manual Oraganizational Chart: Research and Development Analysis ReviewAngelli LamiqueNoch keine Bewertungen

- 162.005.exercises and AssignDokument2 Seiten162.005.exercises and AssignAngelli Lamique50% (2)

- Case 12-29,30Dokument3 SeitenCase 12-29,30Angelli LamiqueNoch keine Bewertungen

- Example From GoogleDokument32 SeitenExample From Googlemiss jiaNoch keine Bewertungen

- You Have Been Given The Following Information For Rpe ConsultingDokument1 SeiteYou Have Been Given The Following Information For Rpe ConsultingTaimour HassanNoch keine Bewertungen

- Introduction To Financial Accounting NotesDokument3 SeitenIntroduction To Financial Accounting NotesRaksa HemNoch keine Bewertungen

- Financial Accounting Vs Management AccountingDokument2 SeitenFinancial Accounting Vs Management AccountingMuhamamd Asfand YarNoch keine Bewertungen

- SRM BBA CBCS SyllabusDokument96 SeitenSRM BBA CBCS SyllabusVipin MisraNoch keine Bewertungen

- PQ 2019 - Financial Accounting SyllabusDokument5 SeitenPQ 2019 - Financial Accounting SyllabusUmeesh NantakumarNoch keine Bewertungen

- Invitation Letter For PFRF and Sca March 3 and 4 1Dokument5 SeitenInvitation Letter For PFRF and Sca March 3 and 4 1Jess MalayaoNoch keine Bewertungen

- Answer To MTP - Intermediate - Syllabus 2016 - Dec2017 - Set 1: Paper 5-Financial AccountingDokument15 SeitenAnswer To MTP - Intermediate - Syllabus 2016 - Dec2017 - Set 1: Paper 5-Financial Accountingpirates123Noch keine Bewertungen

- Practical AccountingDokument25 SeitenPractical AccountingWed CornelNoch keine Bewertungen

- Overview of Ops Aud Part 2 - MARPDokument25 SeitenOverview of Ops Aud Part 2 - MARPRNoch keine Bewertungen

- GTI 2012 Chapter 1 Horizon MarkedDokument9 SeitenGTI 2012 Chapter 1 Horizon MarkedArizal Zul LathiifNoch keine Bewertungen

- New Entity TPS THAYER CPAs in Great Houston AreaDokument2 SeitenNew Entity TPS THAYER CPAs in Great Houston AreaPR.comNoch keine Bewertungen

- GL PPT Basic For Oracle AppsDokument81 SeitenGL PPT Basic For Oracle AppsPhanendra KumarNoch keine Bewertungen

- Audthe02 Activity 1Dokument4 SeitenAudthe02 Activity 1Christian Arnel Jumpay LopezNoch keine Bewertungen

- User Manual Asset AccountingDokument47 SeitenUser Manual Asset AccountinginasapNoch keine Bewertungen

- Financial Statements PLDT and GLobeDokument18 SeitenFinancial Statements PLDT and GLobeArnelli GregorioNoch keine Bewertungen

- Practical Accounting 2Dokument6 SeitenPractical Accounting 2Jessica Marie B. Mendoza0% (1)

- 0157 20230901 Motion To Comply With The August 14 RO Final CombinedDokument86 Seiten0157 20230901 Motion To Comply With The August 14 RO Final CombinedMetro Puerto RicoNoch keine Bewertungen

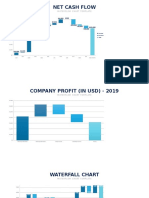

- Waterfall Chart Slides PowerPoint TemplateDokument30 SeitenWaterfall Chart Slides PowerPoint Templateziad ghanemNoch keine Bewertungen

- FNSACC501 Assessment 2Dokument6 SeitenFNSACC501 Assessment 2Daranee TrakanchanNoch keine Bewertungen

- Day 2 Finman p2Dokument6 SeitenDay 2 Finman p2Ericka DeguzmanNoch keine Bewertungen

- Principles of Accounting - Module Information PackDokument6 SeitenPrinciples of Accounting - Module Information PackHaider QureshiNoch keine Bewertungen

- Who Wants To Get UnoDokument45 SeitenWho Wants To Get UnoCarmen YanguasNoch keine Bewertungen

- Job Opportunities World Bank IUCEA African Centers of Excellence (ACE II) ProjectDokument1 SeiteJob Opportunities World Bank IUCEA African Centers of Excellence (ACE II) ProjectRashid BumarwaNoch keine Bewertungen

- International Accounting 3Rd Edition Doupnik Test Bank Full Chapter PDFDokument40 SeitenInternational Accounting 3Rd Edition Doupnik Test Bank Full Chapter PDFJulieHaasyjzp100% (9)

- 2019 ICREATE Audit ReportDokument3 Seiten2019 ICREATE Audit ReportJoanna GarciaNoch keine Bewertungen

- SoM UIA Forensic Review 11.25.2020 708891 7Dokument34 SeitenSoM UIA Forensic Review 11.25.2020 708891 7Tiffany RobertsonNoch keine Bewertungen

- At Quizzer 3 - 2018 Code of Ethics For Professional Accountants in The Phils T1AY2122Dokument15 SeitenAt Quizzer 3 - 2018 Code of Ethics For Professional Accountants in The Phils T1AY2122Rena NervalNoch keine Bewertungen