Das könnte Ihnen auch gefallen

- FXSumsDokument5 SeitenFXSumsPRANJAL BANSALNoch keine Bewertungen

- IfDokument14 SeitenIfĐặng Thuỳ HươngNoch keine Bewertungen

- Chapter 6Dokument17 SeitenChapter 6mark leeNoch keine Bewertungen

- MBF14e Chap05 FX MarketsDokument20 SeitenMBF14e Chap05 FX MarketsHaniyah Nadhira100% (1)

- Week 2 Tutorial ProblemsDokument7 SeitenWeek 2 Tutorial ProblemsWOP INVESTNoch keine Bewertungen

- ExchangeRate SeraphineAmira 120310170096 TugasMKIHitunganDokument7 SeitenExchangeRate SeraphineAmira 120310170096 TugasMKIHitunganSeraphine AmiraNoch keine Bewertungen

- Assumptions Values Spot Exchange RateDokument7 SeitenAssumptions Values Spot Exchange RateSeraphine AmiraNoch keine Bewertungen

- ExchangeRates SeraphineAmira 120310170096 Essay MKIDokument4 SeitenExchangeRates SeraphineAmira 120310170096 Essay MKISeraphine AmiraNoch keine Bewertungen

- FX II PracticeDokument10 SeitenFX II PracticeFinanceman4Noch keine Bewertungen

- MBFinance Chap06-Pbms-finalDokument20 SeitenMBFinance Chap06-Pbms-finalLinda YuNoch keine Bewertungen

- MBF14e Chap05 FX Markets PbmsDokument20 SeitenMBF14e Chap05 FX Markets PbmsNhi Phạm Trần YếnNoch keine Bewertungen

- MBF14e Chap05 FX MarketsDokument20 SeitenMBF14e Chap05 FX Marketskk50% (2)

- MBS12 FeDokument2 SeitenMBS12 FewertyuoiuNoch keine Bewertungen

- Currency Bid Rate Ask/Offer Rate: 1. 2. 3. 4. How Much CAD Received When Selling CHF10, 000,000? 5Dokument4 SeitenCurrency Bid Rate Ask/Offer Rate: 1. 2. 3. 4. How Much CAD Received When Selling CHF10, 000,000? 5Dinhphung Le100% (1)

- Case Study 1 Consists of A Series of Problems andDokument6 SeitenCase Study 1 Consists of A Series of Problems andhhhhhNoch keine Bewertungen

- Test I SDokument5 SeitenTest I Siczech1506Noch keine Bewertungen

- Session 4 International FinanceDokument4 SeitenSession 4 International FinanceTumbleweedNoch keine Bewertungen

- Tugas 3 - Dita Sari LutfianiDokument7 SeitenTugas 3 - Dita Sari LutfianiDita Sari LutfianiNoch keine Bewertungen

- FXD Vs FloatingDokument15 SeitenFXD Vs FloatingVishalNoch keine Bewertungen

- A4-5. Exchange Rate Relationships WorkingsDokument4 SeitenA4-5. Exchange Rate Relationships Workingsmohantyrishita2000Noch keine Bewertungen

- Descriptive Mid 2Dokument1 SeiteDescriptive Mid 2সাবরিন সুলতানাNoch keine Bewertungen

- Fixed Vs Variable Rate Info Sheet.2Dokument6 SeitenFixed Vs Variable Rate Info Sheet.2Tanjiro CedNoch keine Bewertungen

- 2010 Midterm Test MIB27 AcDokument4 Seiten2010 Midterm Test MIB27 Acjust4utube2k10Noch keine Bewertungen

- FINC2011 Tutorial 4Dokument7 SeitenFINC2011 Tutorial 4suitup100100% (3)

- Wksheet 05Dokument18 SeitenWksheet 05venkeeeeeNoch keine Bewertungen

- FX Derivatives ForwardDokument28 SeitenFX Derivatives ForwardtreiptreuNoch keine Bewertungen

- Final ExamDokument18 SeitenFinal ExamHarryNoch keine Bewertungen

- AnnuitiesDokument4 SeitenAnnuitieslekhi spamNoch keine Bewertungen

- Sample Final Term Exam-Solutions PGDokument3 SeitenSample Final Term Exam-Solutions PGYilin YANGNoch keine Bewertungen

- MBF13e Chap06 Pbms - FinalDokument20 SeitenMBF13e Chap06 Pbms - Finalaveenobeatnik100% (2)

- International Finance and Trade II 0705Dokument12 SeitenInternational Finance and Trade II 0705api-26541915Noch keine Bewertungen

- CH 34: International Financial ManagementDokument2 SeitenCH 34: International Financial ManagementMukul KadyanNoch keine Bewertungen

- Results and FindingsDokument8 SeitenResults and FindingsAisyah Mohd KhairNoch keine Bewertungen

- Global Edition: Interest-Rate Swaps, Caps, and FloorsDokument32 SeitenGlobal Edition: Interest-Rate Swaps, Caps, and FloorskerenkangNoch keine Bewertungen

- Westpack AUG 03 Mornng ReportDokument1 SeiteWestpack AUG 03 Mornng ReportMiir ViirNoch keine Bewertungen

- Ans.: Borrow HKD Gain HKD 9,500Dokument3 SeitenAns.: Borrow HKD Gain HKD 9,500Nandini JaganNoch keine Bewertungen

- KR Valuation 28 Sept 2019Dokument54 SeitenKR Valuation 28 Sept 2019ket careNoch keine Bewertungen

- Westpack JUL 20 Mornng ReportDokument1 SeiteWestpack JUL 20 Mornng ReportMiir ViirNoch keine Bewertungen

- Chapter 7 DerrivsDokument7 SeitenChapter 7 DerrivsMbusoThabetheNoch keine Bewertungen

- Ch. 34: International Financial Management Problem 1Dokument4 SeitenCh. 34: International Financial Management Problem 1Mukul KadyanNoch keine Bewertungen

- MBF14e Chap08 Interest Rate Derviatives PbmsDokument16 SeitenMBF14e Chap08 Interest Rate Derviatives PbmsVũ Trần Nhật ViNoch keine Bewertungen

- Uraian 2015 2016 2017 2018 2019 2020 Aug Sep Oct Nov Dec Jan LIBOR (Deposito Dalam USD)Dokument2 SeitenUraian 2015 2016 2017 2018 2019 2020 Aug Sep Oct Nov Dec Jan LIBOR (Deposito Dalam USD)Soni SeptianNoch keine Bewertungen

- MIFA Chap 8Dokument17 SeitenMIFA Chap 8aalomukherjeeNoch keine Bewertungen

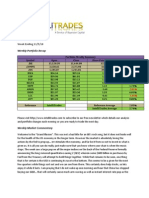

- Weekly Summary - 11/5/2010Dokument2 SeitenWeekly Summary - 11/5/2010intellitradesNoch keine Bewertungen

- Westpack AUG 11 Mornng ReportDokument1 SeiteWestpack AUG 11 Mornng ReportMiir ViirNoch keine Bewertungen

- Westpack JUL 26 Mornng ReportDokument1 SeiteWestpack JUL 26 Mornng ReportMiir ViirNoch keine Bewertungen

- Compound Interest and Present ValueDokument27 SeitenCompound Interest and Present ValueAnnie VNoch keine Bewertungen

- Lynx Fund Performance SummaryDokument2 SeitenLynx Fund Performance Summarymrobertson3890Noch keine Bewertungen

- International Corporate FinanceDokument15 SeitenInternational Corporate Financegabisan1087Noch keine Bewertungen

- Group Assignment 1, (Afsana)Dokument11 SeitenGroup Assignment 1, (Afsana)Afsana Mim JotyNoch keine Bewertungen

- Lecture 3 - Project Network DevelopmentDokument26 SeitenLecture 3 - Project Network Developmentmaoz0533Noch keine Bewertungen

- IPPTChap 003Dokument35 SeitenIPPTChap 003Ghita RochdiNoch keine Bewertungen

- Assignment-1 (IFM), Fatema Sharmin, Id-2022916Dokument5 SeitenAssignment-1 (IFM), Fatema Sharmin, Id-2022916fatemaNoch keine Bewertungen

- Business Statistics Group Mid-Term Exam: Answer 1Dokument4 SeitenBusiness Statistics Group Mid-Term Exam: Answer 1na banNoch keine Bewertungen

- Trading Research, Analysis & Strategy: Prepared By: Junior TradersDokument26 SeitenTrading Research, Analysis & Strategy: Prepared By: Junior TradersLuigiMangayaNoch keine Bewertungen

- Financial Analyst G&M - Real Estate Test & Case StudyDokument19 SeitenFinancial Analyst G&M - Real Estate Test & Case StudyDhruv ShahNoch keine Bewertungen

- Derivative and Risk ManagementDokument4 SeitenDerivative and Risk ManagementDushyant TaraNoch keine Bewertungen

- Muskan Valbani PGP/24/456Dokument6 SeitenMuskan Valbani PGP/24/456Muskan ValbaniNoch keine Bewertungen

- Personal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyVon EverandPersonal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyNoch keine Bewertungen

- Cosco Example PDFDokument4 SeitenCosco Example PDFBeatrice BallabioNoch keine Bewertungen

- Chapter 4 and Other Questions Chapters 1 To 5Dokument8 SeitenChapter 4 and Other Questions Chapters 1 To 5Beatrice BallabioNoch keine Bewertungen

- Assignment Chapter 3Dokument3 SeitenAssignment Chapter 3Beatrice BallabioNoch keine Bewertungen

- Assignment Chapter 1Dokument1 SeiteAssignment Chapter 1Beatrice BallabioNoch keine Bewertungen

- Assignment Chapter 2Dokument1 SeiteAssignment Chapter 2Beatrice BallabioNoch keine Bewertungen

- Assignment Chapter 2 SOLUTIONDokument6 SeitenAssignment Chapter 2 SOLUTIONBeatrice BallabioNoch keine Bewertungen

- Chapter 8Dokument22 SeitenChapter 8mark leeNoch keine Bewertungen

- Chap08 Pbms MBF12eDokument15 SeitenChap08 Pbms MBF12eBeatrice BallabioNoch keine Bewertungen

- Chap07 Pbms MBF12eDokument22 SeitenChap07 Pbms MBF12eBeatrice Ballabio100% (1)

- Chap12 Pbms MBF12eDokument10 SeitenChap12 Pbms MBF12eBeatrice BallabioNoch keine Bewertungen

- Sector San Juan Guidance For RepoweringDokument12 SeitenSector San Juan Guidance For RepoweringTroy IveyNoch keine Bewertungen

- Model Questions and Answers Macro EconomicsDokument14 SeitenModel Questions and Answers Macro EconomicsVrkNoch keine Bewertungen

- Otis C. Mitchell - Hitler-s-Stormtroopers-and-the-Attack-on-the-German-Republic-1919-1933 PDFDokument201 SeitenOtis C. Mitchell - Hitler-s-Stormtroopers-and-the-Attack-on-the-German-Republic-1919-1933 PDFbodyfull100% (2)

- Business English IDokument8 SeitenBusiness English ILarbi Ben TamaNoch keine Bewertungen

- Former Rajya Sabha MP Ajay Sancheti Appeals Finance Minister To Create New Laws To Regulate Cryptocurrency MarketDokument3 SeitenFormer Rajya Sabha MP Ajay Sancheti Appeals Finance Minister To Create New Laws To Regulate Cryptocurrency MarketNation NextNoch keine Bewertungen

- Position Trading Maximizing Probability of Winning TradesDokument91 SeitenPosition Trading Maximizing Probability of Winning Tradescarlo bakaakoNoch keine Bewertungen

- Sculpture and ArchitectureDokument9 SeitenSculpture and ArchitectureIngrid Dianne Luga BernilNoch keine Bewertungen

- Competency #14 Ay 2022-2023 Social StudiesDokument22 SeitenCompetency #14 Ay 2022-2023 Social StudiesCharis RebanalNoch keine Bewertungen

- DEH-X500BT DEH-S4150BT: CD Rds Receiver Receptor de CD Con Rds CD Player Com RdsDokument53 SeitenDEH-X500BT DEH-S4150BT: CD Rds Receiver Receptor de CD Con Rds CD Player Com RdsLUIS MANUEL RINCON100% (1)

- D D D D D D D: SN54HC574, SN74HC574 Octal Edge-Triggered D-Type Flip-Flops With 3-State OutputsDokument16 SeitenD D D D D D D: SN54HC574, SN74HC574 Octal Edge-Triggered D-Type Flip-Flops With 3-State OutputsJADERSONNoch keine Bewertungen

- SIDPAC Standard Data Channels: Ch. No. Symbols Description UnitsDokument2 SeitenSIDPAC Standard Data Channels: Ch. No. Symbols Description UnitsRGFENoch keine Bewertungen

- Akira 007Dokument70 SeitenAkira 007Ocre OcreNoch keine Bewertungen

- UW Mathematics Professor Evaluations For Fall 2011Dokument241 SeitenUW Mathematics Professor Evaluations For Fall 2011DPNoch keine Bewertungen

- Epri Guide For Transmission Line Groundingpdf PDF FreeDokument188 SeitenEpri Guide For Transmission Line Groundingpdf PDF FreeHolman Wbeimar Suarez Niño100% (1)

- Ifrs 15Dokument24 SeitenIfrs 15Madhu Sudan DarjeeNoch keine Bewertungen

- Net June 2013Dokument22 SeitenNet June 2013Sunil PandeyNoch keine Bewertungen

- Method For Determination of Iron Folic Acid & Vitamin B12 in FRK - 07.11.2023Dokument17 SeitenMethod For Determination of Iron Folic Acid & Vitamin B12 in FRK - 07.11.2023jonesbennetteNoch keine Bewertungen

- RULE 130 Rules of CourtDokument141 SeitenRULE 130 Rules of CourtalotcepilloNoch keine Bewertungen

- User Manual For Scanbox Ergo & Banquet Line: Ambient (Neutral), Hot and Active Cooling. Scanbox Meal Delivery CartsDokument8 SeitenUser Manual For Scanbox Ergo & Banquet Line: Ambient (Neutral), Hot and Active Cooling. Scanbox Meal Delivery CartsManunoghiNoch keine Bewertungen

- Technical EnglishDokument7 SeitenTechnical EnglishGul HaiderNoch keine Bewertungen

- Installation Manual of FirmwareDokument6 SeitenInstallation Manual of FirmwareOmar Stalin Lucio RonNoch keine Bewertungen

- NewspaperDokument2 SeitenNewspaperbro nabsNoch keine Bewertungen

- 5 Waves AnswersDokument2 Seiten5 Waves AnswersNoor Ulain NabeelaNoch keine Bewertungen

- Sap Business Objects Edge Series 3.1 Install Windows enDokument104 SeitenSap Business Objects Edge Series 3.1 Install Windows enGerardoNoch keine Bewertungen

- Post Market Surveillance SOPDokument8 SeitenPost Market Surveillance SOPgopinathNoch keine Bewertungen

- Binary To DecimalDokument8 SeitenBinary To DecimalEmmanuel JoshuaNoch keine Bewertungen

- A Person On A Position of Air Traffic ControllerDokument7 SeitenA Person On A Position of Air Traffic ControllerMUHAMMAD RAMZANNoch keine Bewertungen

- How To Do Nothing - Jenny Odell - MediumDokument67 SeitenHow To Do Nothing - Jenny Odell - MediumWilmer Rodriguez100% (4)

- AH Business-Management All 2011Dokument11 SeitenAH Business-Management All 2011Sanam PuriNoch keine Bewertungen

- Assessment 3 Comparative Analysis Primary Vs Secondary SourcesDokument5 SeitenAssessment 3 Comparative Analysis Primary Vs Secondary SourcesMATOZA, YLJOE V.Noch keine Bewertungen