Das könnte Ihnen auch gefallen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- DFI 303 Simultaneous Effects of Supply and Demand ElasticityDokument10 SeitenDFI 303 Simultaneous Effects of Supply and Demand ElasticityKelvin Oronge100% (1)

- Public Finance Lecture on Role of GovernmentDokument26 SeitenPublic Finance Lecture on Role of GovernmentKelvin OrongeNoch keine Bewertungen

- Environmental Externalities: Market Failures and Policy OptionsDokument16 SeitenEnvironmental Externalities: Market Failures and Policy OptionsKelvin OrongeNoch keine Bewertungen

- Dfi 303 Ext 416Dokument8 SeitenDfi 303 Ext 416Kelvin OrongeNoch keine Bewertungen

- DFI 301 Lecture Five - Monetary PolicyDokument13 SeitenDFI 301 Lecture Five - Monetary PolicyKelvin OrongeNoch keine Bewertungen

- DFI 301 Lecture Two - Money SupplyDokument12 SeitenDFI 301 Lecture Two - Money SupplyKelvin OrongeNoch keine Bewertungen

- Central Bank Lecture: Roles, Independence & CredibilityDokument6 SeitenCentral Bank Lecture: Roles, Independence & CredibilityKelvin OrongeNoch keine Bewertungen

- Lecture One - IntroductionDokument11 SeitenLecture One - IntroductionKelvin OrongeNoch keine Bewertungen

- DFI 301R2020 Comprehensive Assignment OneDokument7 SeitenDFI 301R2020 Comprehensive Assignment OneKelvin OrongeNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- SKP Sec-Balrampur (Init Cov) - 2012Dokument12 SeitenSKP Sec-Balrampur (Init Cov) - 2012rchawdhry123Noch keine Bewertungen

- Karsanbhai Patel - The Indian entrepreneur who built a detergent empire from scratchDokument3 SeitenKarsanbhai Patel - The Indian entrepreneur who built a detergent empire from scratchNikhil PatelNoch keine Bewertungen

- Marketing Process: Analysis of The Opportunities in The MarketDokument7 SeitenMarketing Process: Analysis of The Opportunities in The Marketlekz reNoch keine Bewertungen

- Tutor 2 (Cost, Volume, Profit Analysis)Dokument2 SeitenTutor 2 (Cost, Volume, Profit Analysis)aulia100% (1)

- Solutions Paper - EcoDokument4 SeitenSolutions Paper - Ecosanchita mukherjeeNoch keine Bewertungen

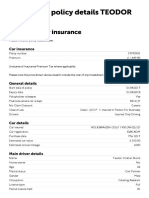

- Policy Details PageDokument2 SeitenPolicy Details PageLuci PoroNoch keine Bewertungen

- EOLA's Equity Distribution - v4Dokument18 SeitenEOLA's Equity Distribution - v4AR-Lion ResearchingNoch keine Bewertungen

- Chapter 6 - Accounting For SalesDokument4 SeitenChapter 6 - Accounting For SalesArmanNoch keine Bewertungen

- WestsideDokument10 SeitenWestsideBhaswati PandaNoch keine Bewertungen

- Dokumen - Tips 128057344 Chapter 2Dokument70 SeitenDokumen - Tips 128057344 Chapter 2GianJoshuaDayritNoch keine Bewertungen

- IT 2U Business Section 2 Seat 2Dokument120 SeitenIT 2U Business Section 2 Seat 2ANee NameeNoch keine Bewertungen

- Essential Shopping VocabularyDokument17 SeitenEssential Shopping VocabularyPeter Eric SmithNoch keine Bewertungen

- Markowitz Portfolio TheoryRDokument9 SeitenMarkowitz Portfolio TheoryRShafiq KhanNoch keine Bewertungen

- CH01 Printer PDFDokument26 SeitenCH01 Printer PDFClaire Evann Villena EboraNoch keine Bewertungen

- CH 11 - CF Estimation Mini Case Sols Word 1514edDokument13 SeitenCH 11 - CF Estimation Mini Case Sols Word 1514edHari CahyoNoch keine Bewertungen

- Strange Times, Or, Perhaps I Just Don T Get It (04.10.08)Dokument8 SeitenStrange Times, Or, Perhaps I Just Don T Get It (04.10.08)BunNoch keine Bewertungen

- PM Examiner's Report March June 2022Dokument23 SeitenPM Examiner's Report March June 2022NAVIN JOSHINoch keine Bewertungen

- EOQDokument53 SeitenEOQFredericfrancisNoch keine Bewertungen

- Service Pricing and The Financial and Economic Effect of ServiceDokument25 SeitenService Pricing and The Financial and Economic Effect of ServicePietro BertolucciNoch keine Bewertungen

- RR 8-98Dokument3 SeitenRR 8-98matinikkiNoch keine Bewertungen

- Financial StatementDokument33 SeitenFinancial StatementĎêěpãķ Šhăŕmå100% (1)

- Economics of Strategy 6Th Edition PDF Full ChapterDokument41 SeitenEconomics of Strategy 6Th Edition PDF Full Chapterrosa.green630100% (27)

- International Cha 2Dokument26 SeitenInternational Cha 2felekebirhanu7Noch keine Bewertungen

- Offer and Acceptance NotesDokument24 SeitenOffer and Acceptance NotesvijiNoch keine Bewertungen

- Causes and Measures of Disequilibrium in Balance of PaymentsDokument6 SeitenCauses and Measures of Disequilibrium in Balance of PaymentsMonika PathakNoch keine Bewertungen

- Hero Hond: Marketing and Human Resource ManagementDokument70 SeitenHero Hond: Marketing and Human Resource Managementdhiraj022Noch keine Bewertungen

- Midterm Examination in Public FinanceDokument2 SeitenMidterm Examination in Public FinanceNekki Joy LangcuyanNoch keine Bewertungen

- Tax Incidence and Shifting ExplainedDokument12 SeitenTax Incidence and Shifting ExplainedRajesh ShahiNoch keine Bewertungen

- 67 79 - 2008 1Dokument140 Seiten67 79 - 2008 1mgordon66Noch keine Bewertungen

- Cable Industry in Indonesia PDFDokument85 SeitenCable Industry in Indonesia PDFlinggaraninditaNoch keine Bewertungen