Das könnte Ihnen auch gefallen

- Kotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Dokument15 SeitenKotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Surbhî GuptaNoch keine Bewertungen

- Bank of BarodaDokument22 SeitenBank of BarodaShivane SivakumarNoch keine Bewertungen

- 17 - Manoj Batra - Hero Honda MotorsDokument13 Seiten17 - Manoj Batra - Hero Honda Motorsrajat_singlaNoch keine Bewertungen

- HDFC Bank - FM AssignmentDokument9 SeitenHDFC Bank - FM AssignmentaditiNoch keine Bewertungen

- Company Name - Deepak Nitrite Soumya Upadhyay 110 EBIZ 2 Sujay Singhvi 112 EBIZ 2Dokument14 SeitenCompany Name - Deepak Nitrite Soumya Upadhyay 110 EBIZ 2 Sujay Singhvi 112 EBIZ 2Sujay SinghviNoch keine Bewertungen

- Ratios, VLOOKUP, Goal SeekDokument15 SeitenRatios, VLOOKUP, Goal SeekVIIKHAS VIIKHASNoch keine Bewertungen

- Reshma Chauhan - PGFC1927 (BOCA)Dokument9 SeitenReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNoch keine Bewertungen

- Ratio Analysis: Submitted To. Prof Lakshmi Chand Submitted By: Rahul Sebastian Submitted On: 10/01/2011Dokument6 SeitenRatio Analysis: Submitted To. Prof Lakshmi Chand Submitted By: Rahul Sebastian Submitted On: 10/01/2011Thomas RajanNoch keine Bewertungen

- Bemd RatiosDokument12 SeitenBemd RatiosPRADEEP CHAVANNoch keine Bewertungen

- Bank Performance Analysis - Sahil Badaya PGFB1942Dokument10 SeitenBank Performance Analysis - Sahil Badaya PGFB1942Surbhî GuptaNoch keine Bewertungen

- This Is An Open Book Examination. 2. Attempt Any Four Out of Six Questions. 3. All Questions Carry Equal MarksDokument32 SeitenThis Is An Open Book Examination. 2. Attempt Any Four Out of Six Questions. 3. All Questions Carry Equal MarksSukanya Shridhar 1 9 9 0 3 5Noch keine Bewertungen

- FMUE Group Assignment - Group 4 - Section B2CDDokument42 SeitenFMUE Group Assignment - Group 4 - Section B2CDyash jhunjhunuwalaNoch keine Bewertungen

- 29 - Tej Inder - Bharti AirtelDokument14 Seiten29 - Tej Inder - Bharti Airtelrajat_singlaNoch keine Bewertungen

- Bank ValuationDokument88 SeitenBank Valuationsnithisha chandranNoch keine Bewertungen

- New Microsoft Word DocumentDokument2 SeitenNew Microsoft Word Documentনীল আকাশNoch keine Bewertungen

- Three Statement ModelDokument9 SeitenThree Statement ModelAnkit SharmaNoch keine Bewertungen

- Group8 - Ratio Analysis of Yes BankDokument14 SeitenGroup8 - Ratio Analysis of Yes Bankavinash singhNoch keine Bewertungen

- Bank Performance Analysis With Risk RatiosDokument8 SeitenBank Performance Analysis With Risk RatiosSurbhî GuptaNoch keine Bewertungen

- Financials of Canara BankDokument14 SeitenFinancials of Canara BankSattwik rathNoch keine Bewertungen

- Dabul Income Statement SourceDokument13 SeitenDabul Income Statement SourceChachapooltableNoch keine Bewertungen

- Tata Motors DCFDokument11 SeitenTata Motors DCFChirag SharmaNoch keine Bewertungen

- Tvs Motor 2019 2018 2017 2016 2015Dokument108 SeitenTvs Motor 2019 2018 2017 2016 2015Rima ParekhNoch keine Bewertungen

- Oil and Natural Gas CorporationDokument43 SeitenOil and Natural Gas CorporationNishant SharmaNoch keine Bewertungen

- KPR Phase - 1Dokument23 SeitenKPR Phase - 1Satyam1771Noch keine Bewertungen

- Apollo TyresDokument4 SeitenApollo TyresGokulKumarNoch keine Bewertungen

- FA Balance SheetDokument15 SeitenFA Balance SheetPrakash BhanushaliNoch keine Bewertungen

- Radico KhaitanDokument38 SeitenRadico Khaitantapasya khanijouNoch keine Bewertungen

- BF1 Package Ratios ForecastingDokument16 SeitenBF1 Package Ratios ForecastingBilal Javed JafraniNoch keine Bewertungen

- HDFC Bank Equity Research ReportDokument9 SeitenHDFC Bank Equity Research ReportShreyo ChakrabortyNoch keine Bewertungen

- FA of ItcDokument18 SeitenFA of ItcSriya GuptaNoch keine Bewertungen

- FINANCIAL ANALYSIS of ONGCDokument13 SeitenFINANCIAL ANALYSIS of ONGCdipshi92Noch keine Bewertungen

- Financial Modelling ExcelDokument6 SeitenFinancial Modelling ExcelAanchal MahajanNoch keine Bewertungen

- Relaxo Footwear - Updated BSDokument54 SeitenRelaxo Footwear - Updated BSRonakk MoondraNoch keine Bewertungen

- Federal Bank AnalysisDokument22 SeitenFederal Bank AnalysisSoorajKrishnanNoch keine Bewertungen

- Private Banks Fundamentals: Siddesh Naik Abhishek RanjanDokument19 SeitenPrivate Banks Fundamentals: Siddesh Naik Abhishek RanjanAbhishekNoch keine Bewertungen

- KPR MillsDokument32 SeitenKPR MillsSatyam1771Noch keine Bewertungen

- สำเนา Financial Model 2Dokument6 Seitenสำเนา Financial Model 2Chananya SriromNoch keine Bewertungen

- Asset Liability Management at HDFC BankDokument31 SeitenAsset Liability Management at HDFC BankwebstdsnrNoch keine Bewertungen

- Bank Performance Analysis-INDUSIND BANK: Particulars Mar-16Dokument26 SeitenBank Performance Analysis-INDUSIND BANK: Particulars Mar-16Surbhî GuptaNoch keine Bewertungen

- Key Financial Ratios of UCO Bank - in Rs. Cr.Dokument19 SeitenKey Financial Ratios of UCO Bank - in Rs. Cr.anishbhattacharyyaNoch keine Bewertungen

- Common SizeDokument4 SeitenCommon SizeEsa KarismaNoch keine Bewertungen

- Accounts Term PaperDokument508 SeitenAccounts Term Paperrohit_indiaNoch keine Bewertungen

- D489 Abhishek JSWphase 2Dokument44 SeitenD489 Abhishek JSWphase 2Yash KalaNoch keine Bewertungen

- DCF - Mega Webinar - Pranav - 22.08Dokument80 SeitenDCF - Mega Webinar - Pranav - 22.08zorem axoneNoch keine Bewertungen

- Balance Sheet of Indiabulls - in Rs. Cr.Dokument3 SeitenBalance Sheet of Indiabulls - in Rs. Cr.MubeenNoch keine Bewertungen

- DR Lal Path Labs Financial Model - Ayushi JainDokument39 SeitenDR Lal Path Labs Financial Model - Ayushi JainDeepak NechlaniNoch keine Bewertungen

- MaricoDokument13 SeitenMaricoRitesh KhobragadeNoch keine Bewertungen

- JSW Energy: Horizontal Analysis Vertical AnalysisDokument15 SeitenJSW Energy: Horizontal Analysis Vertical Analysissuyash gargNoch keine Bewertungen

- Balancesheet - Tata Motors LTDDokument9 SeitenBalancesheet - Tata Motors LTDNaveen KumarNoch keine Bewertungen

- Ambuja Cements: Profit & Loss AccountDokument15 SeitenAmbuja Cements: Profit & Loss Accountwritik sahaNoch keine Bewertungen

- Shinansh TiwariDokument11 SeitenShinansh TiwariAnuj VermaNoch keine Bewertungen

- Titan Company TemplateDokument18 SeitenTitan Company Templatesejal aroraNoch keine Bewertungen

- IM ProjectDokument24 SeitenIM ProjectDäzzlîñg HärîshNoch keine Bewertungen

- 17pgp216 ApolloDokument5 Seiten17pgp216 ApolloVamsi GunturuNoch keine Bewertungen

- Finance Profit & Loss HDFC Bank LTD: Year 2021 2020 2019 2018 IncomeDokument12 SeitenFinance Profit & Loss HDFC Bank LTD: Year 2021 2020 2019 2018 IncomeYash SinghalNoch keine Bewertungen

- Profitability Test: Profit/Net Sales Pat-Pref Div/ No of Eq Shares (Pat-Pref Div) / Eqty FundDokument7 SeitenProfitability Test: Profit/Net Sales Pat-Pref Div/ No of Eq Shares (Pat-Pref Div) / Eqty FundJatin AroraNoch keine Bewertungen

- Financial Statements - TATA - MotorsDokument5 SeitenFinancial Statements - TATA - MotorsKAVYA GOYAL PGP 2021-23 BatchNoch keine Bewertungen

- Project of Tata MotorsDokument7 SeitenProject of Tata MotorsRaj KiranNoch keine Bewertungen

- Year Latest 2017 2016 2015 2014 2013 2012 2011 2010 2009 Key RatiosDokument11 SeitenYear Latest 2017 2016 2015 2014 2013 2012 2011 2010 2009 Key Ratiospriyanshu14Noch keine Bewertungen

- Schaum's Outline of Basic Business Mathematics, 2edVon EverandSchaum's Outline of Basic Business Mathematics, 2edBewertung: 5 von 5 Sternen5/5 (1)

- Boca Vinay pgfc1948 Icici BankDokument12 SeitenBoca Vinay pgfc1948 Icici BankSurbhî GuptaNoch keine Bewertungen

- Shreya Jain - PGFC1935 - Performance AnalysisDokument13 SeitenShreya Jain - PGFC1935 - Performance AnalysisSurbhî GuptaNoch keine Bewertungen

- Marketing Channels For ServicesDokument24 SeitenMarketing Channels For ServicesSurbhî GuptaNoch keine Bewertungen

- Electronic Marketing ChannelsDokument25 SeitenElectronic Marketing ChannelsSurbhî GuptaNoch keine Bewertungen

- Bank Performance Analysis-INDUSIND BANK: Particulars Mar-16Dokument26 SeitenBank Performance Analysis-INDUSIND BANK: Particulars Mar-16Surbhî GuptaNoch keine Bewertungen

- Shashank Malik - PGFB1944 - BOCA GR2 - Study Group 4 - Central Bank of IndiaDokument13 SeitenShashank Malik - PGFB1944 - BOCA GR2 - Study Group 4 - Central Bank of IndiaSurbhî GuptaNoch keine Bewertungen

- Kotak Mahindra Bank Performance AnalysisDokument18 SeitenKotak Mahindra Bank Performance AnalysisSurbhî GuptaNoch keine Bewertungen

- Nitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Dokument12 SeitenNitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Surbhî GuptaNoch keine Bewertungen

- Shreeya Verma (PGSF1952)Dokument15 SeitenShreeya Verma (PGSF1952)Surbhî GuptaNoch keine Bewertungen

- Bank of India Performance Analysis: Total AssetsDokument6 SeitenBank of India Performance Analysis: Total AssetsSurbhî GuptaNoch keine Bewertungen

- Performance Analysis - CbiDokument19 SeitenPerformance Analysis - CbiSurbhî GuptaNoch keine Bewertungen

- Samarth Mehrotra - BOCADokument23 SeitenSamarth Mehrotra - BOCASurbhî GuptaNoch keine Bewertungen

- Satyam PGSF1937 BOCA BOI BADokument15 SeitenSatyam PGSF1937 BOCA BOI BASurbhî GuptaNoch keine Bewertungen

- Bank Performance Analysis - Sahil Badaya PGFB1942Dokument10 SeitenBank Performance Analysis - Sahil Badaya PGFB1942Surbhî GuptaNoch keine Bewertungen

- Axis Bank Ltd. Performance AnalysisDokument13 SeitenAxis Bank Ltd. Performance AnalysisSurbhî GuptaNoch keine Bewertungen

- Bank Performance Analysis With Risk RatiosDokument8 SeitenBank Performance Analysis With Risk RatiosSurbhî GuptaNoch keine Bewertungen

- YES Bank Performance AnalysisDokument11 SeitenYES Bank Performance AnalysisSurbhî GuptaNoch keine Bewertungen

- Rashi AggarwalDokument17 SeitenRashi AggarwalSurbhî GuptaNoch keine Bewertungen

- Reshma Chauhan - PGFC1927 (BOCA)Dokument9 SeitenReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNoch keine Bewertungen

- Equities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Dokument11 SeitenEquities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Surbhî GuptaNoch keine Bewertungen

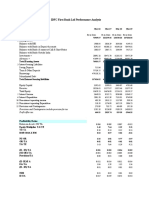

- IDFC First Bank LTD Performance Analysis: Total AssetsDokument6 SeitenIDFC First Bank LTD Performance Analysis: Total AssetsSurbhî GuptaNoch keine Bewertungen

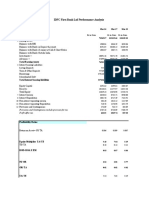

- IDFC First Bank LTD Performance Analysis: Total AssetsDokument9 SeitenIDFC First Bank LTD Performance Analysis: Total AssetsSurbhî GuptaNoch keine Bewertungen

- Priya Bansal pgfc1924Dokument8 SeitenPriya Bansal pgfc1924Surbhî GuptaNoch keine Bewertungen

- Bank Performance AnalysisDokument10 SeitenBank Performance AnalysisSurbhî GuptaNoch keine Bewertungen

- Assignment pgfc1913Dokument9 SeitenAssignment pgfc1913Surbhî GuptaNoch keine Bewertungen

- Provisions and Contingencies Include Provision For TaxDokument6 SeitenProvisions and Contingencies Include Provision For TaxSurbhî GuptaNoch keine Bewertungen

- Bank Performance AnalysisDokument4 SeitenBank Performance AnalysisSurbhî GuptaNoch keine Bewertungen

- Axis Bank Ltd. Performance AnalysisDokument11 SeitenAxis Bank Ltd. Performance AnalysisSurbhî GuptaNoch keine Bewertungen

- Performance Analysis of ICICI BankDokument7 SeitenPerformance Analysis of ICICI BankSurbhî GuptaNoch keine Bewertungen

- Peritoneal Dialysis Unit Renal Department SGH PD WPI 097 Workplace InstructionDokument10 SeitenPeritoneal Dialysis Unit Renal Department SGH PD WPI 097 Workplace InstructionAjeng SuparwiNoch keine Bewertungen

- Filipino Concept of Health and IllnessDokument43 SeitenFilipino Concept of Health and IllnessFelisa Lacsamana Gregorio50% (2)

- Case StudyDokument3 SeitenCase StudyMarlon MagtibayNoch keine Bewertungen

- X-Pruf Crystalcoat: Cementitious Crystalline Waterproof Coating For ConcreteDokument2 SeitenX-Pruf Crystalcoat: Cementitious Crystalline Waterproof Coating For ConcreteAmr RagabNoch keine Bewertungen

- Osmotic Power Generation: Prepared byDokument16 SeitenOsmotic Power Generation: Prepared byPritam MishraNoch keine Bewertungen

- 200 State Council Members 2010Dokument21 Seiten200 State Council Members 2010madhu kanna100% (1)

- Medical-Surgical Nursing Assessment and Management of Clinical Problems 9e Chapter 23Dokument5 SeitenMedical-Surgical Nursing Assessment and Management of Clinical Problems 9e Chapter 23sarasjunkNoch keine Bewertungen

- Risk Management Policy StatementDokument13 SeitenRisk Management Policy StatementRatnakumar ManivannanNoch keine Bewertungen

- Data NX 45-5-1800-4Dokument1 SeiteData NX 45-5-1800-4BHILLA TORRESNoch keine Bewertungen

- BRSM Form 009 - QMS MDD TPDDokument15 SeitenBRSM Form 009 - QMS MDD TPDAnonymous q8lh3fldWMNoch keine Bewertungen

- Anthropometric Article2Dokument11 SeitenAnthropometric Article2Lakshita SainiNoch keine Bewertungen

- Field Study 1-Act 5.1Dokument5 SeitenField Study 1-Act 5.1Mariya QuedzNoch keine Bewertungen

- Principles in Biochemistry (SBK3013)Dokument3 SeitenPrinciples in Biochemistry (SBK3013)Leena MuniandyNoch keine Bewertungen

- AJINOMOTO 2013 Ideal Amino Acid Profile For PigletsDokument28 SeitenAJINOMOTO 2013 Ideal Amino Acid Profile For PigletsFreddy Alexander Horna Morillo100% (1)

- DENSO Diagnostic TipsDokument1 SeiteDENSO Diagnostic TipsVerona MamaiaNoch keine Bewertungen

- Brooklyn Hops BreweryDokument24 SeitenBrooklyn Hops BrewerynyairsunsetNoch keine Bewertungen

- 21-Ent, 45 Notes To PGDokument12 Seiten21-Ent, 45 Notes To PGAshish SinghNoch keine Bewertungen

- UntitledDokument8 SeitenUntitledapi-86749355Noch keine Bewertungen

- SwivelDokument29 SeitenSwivelluisedonossaNoch keine Bewertungen

- Decommissioning HSE PDFDokument105 SeitenDecommissioning HSE PDFRafael Rocha100% (1)

- 95491fisa Tehnica Acumulator Growatt Lithiu 6.5 KWH Acumulatori Sistem Fotovoltaic Alaska Energies Romania CompressedDokument4 Seiten95491fisa Tehnica Acumulator Growatt Lithiu 6.5 KWH Acumulatori Sistem Fotovoltaic Alaska Energies Romania CompressedmiaasieuNoch keine Bewertungen

- XII Biology Practicals 2020-21 Without ReadingDokument32 SeitenXII Biology Practicals 2020-21 Without ReadingStylish HeroNoch keine Bewertungen

- 2 5416087904969556847 PDFDokument480 Seiten2 5416087904969556847 PDFArvindhanNoch keine Bewertungen

- Assignment 4Dokument4 SeitenAssignment 4ShabihNoch keine Bewertungen

- Clase No. 24 Nouns and Their Modifiers ExercisesDokument2 SeitenClase No. 24 Nouns and Their Modifiers ExercisesenriquefisicoNoch keine Bewertungen

- Contoh Permintaan Obat CitoDokument2 SeitenContoh Permintaan Obat CitoAriandy yanuarNoch keine Bewertungen

- Applications Shaft SealDokument23 SeitenApplications Shaft SealMandisa Sinenhlanhla NduliNoch keine Bewertungen

- Cruz v. CA - G.R. No. 122445 - November 18, 1997 - DIGESTDokument2 SeitenCruz v. CA - G.R. No. 122445 - November 18, 1997 - DIGESTAaron Ariston80% (5)

- Norsok R 002Dokument186 SeitenNorsok R 002robson2015Noch keine Bewertungen

- Research Article Effects of PH On The Shape of Alginate Particles and Its Release BehaviorDokument10 SeitenResearch Article Effects of PH On The Shape of Alginate Particles and Its Release BehaviorAmalia HanifaNoch keine Bewertungen