Das könnte Ihnen auch gefallen

- AFE 5008-B Model Answers For The Final Examinations: SolutionsDokument10 SeitenAFE 5008-B Model Answers For The Final Examinations: SolutionsDiana TuckerNoch keine Bewertungen

- Sample Questions For Publication-Mbaf 601-Oct-2022Dokument3 SeitenSample Questions For Publication-Mbaf 601-Oct-2022Laud ListowellNoch keine Bewertungen

- Sample Questions For Publication-Mbaf 601-Oct-2022-SolutionsDokument3 SeitenSample Questions For Publication-Mbaf 601-Oct-2022-SolutionsLaud ListowellNoch keine Bewertungen

- Magsino Hannah Florence Activity 5 Discounted Cash FlowsDokument36 SeitenMagsino Hannah Florence Activity 5 Discounted Cash FlowsKathyrine Claire Edrolin100% (2)

- Exercises On Implementation of DCF ApproachDokument10 SeitenExercises On Implementation of DCF ApproachVincenzoPizzulliNoch keine Bewertungen

- Chapter 8Dokument6 SeitenChapter 8ديـنـا عادلNoch keine Bewertungen

- CH - 04 SolutionDokument3 SeitenCH - 04 SolutionSaifur R. SabbirNoch keine Bewertungen

- Economy ExcelDokument7 SeitenEconomy ExcelCarina MariaNoch keine Bewertungen

- Managerial Economics Assignment Bratu Carina Maria BA EXCELDokument7 SeitenManagerial Economics Assignment Bratu Carina Maria BA EXCELCarina MariaNoch keine Bewertungen

- ACC9005M - Lecture 4 - Financial Analysis (Recycle LTD) QUESTIONDokument2 SeitenACC9005M - Lecture 4 - Financial Analysis (Recycle LTD) QUESTIONPravallika RavikumarNoch keine Bewertungen

- Solution FAR 2Dokument20 SeitenSolution FAR 2ANoch keine Bewertungen

- 17 Financial Statements (With Adjustments)Dokument16 Seiten17 Financial Statements (With Adjustments)Dayaan ANoch keine Bewertungen

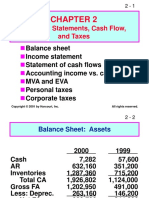

- Financial Statements, Cash Flow, and TaxesDokument44 SeitenFinancial Statements, Cash Flow, and TaxesJuliani Tania RizkyNoch keine Bewertungen

- Tutor 1Dokument6 SeitenTutor 1Elaine LimNoch keine Bewertungen

- Tutorial 11 Interco TransactionsDokument15 SeitenTutorial 11 Interco TransactionsBình QuốcNoch keine Bewertungen

- CFAS 16 and 18Dokument2 SeitenCFAS 16 and 18Cath OquialdaNoch keine Bewertungen

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDokument7 SeitenAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNoch keine Bewertungen

- Allowable DeductionsDokument9 SeitenAllowable DeductionsLyka RoguelNoch keine Bewertungen

- Problem 7-15 SolutionDokument5 SeitenProblem 7-15 SolutionNguyenNoch keine Bewertungen

- Delta ProjectDokument14 SeitenDelta ProjectAyush SinghNoch keine Bewertungen

- Assignment N3Dokument12 SeitenAssignment N3Maiko KopadzeNoch keine Bewertungen

- ACCG 200 Week 8 Homework QuestionsDokument3 SeitenACCG 200 Week 8 Homework QuestionsAlexander TrovatoNoch keine Bewertungen

- Statement of Cash Flows Lecture Questions and AnswersDokument9 SeitenStatement of Cash Flows Lecture Questions and AnswersSaaniya AbbasiNoch keine Bewertungen

- RATIO QuestionsDokument5 SeitenRATIO QuestionsikkaNoch keine Bewertungen

- Tyasa Putri R - Tugas Akl 1 TM 4Dokument6 SeitenTyasa Putri R - Tugas Akl 1 TM 4Rayhan MametNoch keine Bewertungen

- Far410 - SS - Feb 2022Dokument9 SeitenFar410 - SS - Feb 2022AFIZA JASMANNoch keine Bewertungen

- D.1. Financial Statement AnalysisDokument3 SeitenD.1. Financial Statement AnalysisIrfan PoonawalaNoch keine Bewertungen

- ACCT101 9n10 SCFDokument17 SeitenACCT101 9n10 SCFVedanshi BihaniNoch keine Bewertungen

- Solution To R Haque Associates ProblemDokument8 SeitenSolution To R Haque Associates ProblemHasanNoch keine Bewertungen

- Equity MethodDokument2 SeitenEquity MethodJeane Mae BooNoch keine Bewertungen

- Financial AnalysisDokument24 SeitenFinancial AnalysisSwathi ShanmuganathanNoch keine Bewertungen

- Lazar Blue Book Chapter 4 Solution (1 To 14 Only)Dokument27 SeitenLazar Blue Book Chapter 4 Solution (1 To 14 Only)Shuhada Shamsuddin75% (4)

- Illustration 1 & 2Dokument5 SeitenIllustration 1 & 2faith olaNoch keine Bewertungen

- Fundamentals of Corporate Finance 6th Edition Christensen Solutions ManualDokument6 SeitenFundamentals of Corporate Finance 6th Edition Christensen Solutions ManualJamesOrtegapfcs100% (61)

- 8447809Dokument11 Seiten8447809blackghostNoch keine Bewertungen

- Better Mousetraps ExerciseDokument11 SeitenBetter Mousetraps ExerciseBrl Gnsn0% (1)

- Financial Ratios IIDokument27 SeitenFinancial Ratios IIMohamad Gammaz0% (1)

- Solutions IAS 1 For SEPT ATTEMPT FinalDokument25 SeitenSolutions IAS 1 For SEPT ATTEMPT FinalShehrozSTNoch keine Bewertungen

- Asdos Jawaban 2Dokument3 SeitenAsdos Jawaban 2mutiaoooNoch keine Bewertungen

- Financial Analysis DashboardDokument11 SeitenFinancial Analysis DashboardZidan ZaifNoch keine Bewertungen

- E - CAsh Flow Question Meath With Solution and WorkingsDokument5 SeitenE - CAsh Flow Question Meath With Solution and Workingschalah DeriNoch keine Bewertungen

- Febbinia Dwigna P - Week7 AKL 1Dokument5 SeitenFebbinia Dwigna P - Week7 AKL 1febbiniaNoch keine Bewertungen

- Solutions To End-Of-Chapter ProblemsDokument14 SeitenSolutions To End-Of-Chapter ProblemsTushar MalhotraNoch keine Bewertungen

- FM II Assignment 3 SolutionDokument2 SeitenFM II Assignment 3 SolutionSheryar NaeemNoch keine Bewertungen

- Assignment 1 MENG 6502Dokument6 SeitenAssignment 1 MENG 6502russ jhingoorieNoch keine Bewertungen

- Statement of Cash FlowsDokument12 SeitenStatement of Cash FlowsDaniel PeterNoch keine Bewertungen

- Chapter 1 - Hightech Single Step vs. Multi-Step Income StatementDokument2 SeitenChapter 1 - Hightech Single Step vs. Multi-Step Income StatementvarshithagangavarapuNoch keine Bewertungen

- Chapter 7 Up StreamDokument14 SeitenChapter 7 Up StreamAditya Agung SatrioNoch keine Bewertungen

- Data Bodie Industrial Supply V1Dokument10 SeitenData Bodie Industrial Supply V1Giovani R. Pangos RosasNoch keine Bewertungen

- Question No 1: A-Gross PayDokument6 SeitenQuestion No 1: A-Gross PayArmaghan Ali MalikNoch keine Bewertungen

- Spread Sheet ModelingDokument9 SeitenSpread Sheet ModelingAbhay BaraNoch keine Bewertungen

- Start-Up Capital:: Particulars Taka TakaDokument5 SeitenStart-Up Capital:: Particulars Taka TakaSahriar EmonNoch keine Bewertungen

- MBA Session 2 Teddy PLC QuestionDokument2 SeitenMBA Session 2 Teddy PLC QuestionTafsir-i- AliNoch keine Bewertungen

- Assets 2018 2019 Forecast: Balance SheetDokument12 SeitenAssets 2018 2019 Forecast: Balance SheetJosephAmparoNoch keine Bewertungen

- Lecture 1 & 2 ExamplesDokument5 SeitenLecture 1 & 2 ExamplesAbubakari Abdul MananNoch keine Bewertungen

- Purchase Price and Implied Value Less: Book Value of Equity Acquired: Difference Beetwen Implied and Book Value Record New Goodwil BalanceDokument14 SeitenPurchase Price and Implied Value Less: Book Value of Equity Acquired: Difference Beetwen Implied and Book Value Record New Goodwil BalancesallyNoch keine Bewertungen

- Complete Financial Statements With SCF Direcdt MethodDokument23 SeitenComplete Financial Statements With SCF Direcdt MethodJuja FlorentinoNoch keine Bewertungen

- Problem 7-15 Part ADokument7 SeitenProblem 7-15 Part AImelda100% (1)

- Homework N3Dokument24 SeitenHomework N3Maiko KopadzeNoch keine Bewertungen

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsVon EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNoch keine Bewertungen

- Construction Contracts-Journal EntriesDokument2 SeitenConstruction Contracts-Journal EntriesChristine Joy Lanaban100% (1)

- Seatwork 01 Statement of Financial PositionDokument3 SeitenSeatwork 01 Statement of Financial PositionChristine Joy LanabanNoch keine Bewertungen

- Home Office and Branch Accounting-ExerciseDokument2 SeitenHome Office and Branch Accounting-ExerciseChristine Joy LanabanNoch keine Bewertungen

- Name: - Course and Year: - Problem No. 1Dokument2 SeitenName: - Course and Year: - Problem No. 1Christine Joy LanabanNoch keine Bewertungen

- Problem 12-1Dokument1 SeiteProblem 12-1Christine Joy LanabanNoch keine Bewertungen

- Home Office and Branch Accounting-Exercise PDFDokument2 SeitenHome Office and Branch Accounting-Exercise PDFChristine Joy LanabanNoch keine Bewertungen

- Seatwork 02 Statement of Income (TEST I) Multiple Choice: Shade Your Answer With YELLOWDokument5 SeitenSeatwork 02 Statement of Income (TEST I) Multiple Choice: Shade Your Answer With YELLOWChristine Joy LanabanNoch keine Bewertungen

- Gross Profit in Prior YearsDokument2 SeitenGross Profit in Prior YearsChristine Joy LanabanNoch keine Bewertungen

- Quizzer Financial Position and Income StatementDokument9 SeitenQuizzer Financial Position and Income StatementChristine Joy LanabanNoch keine Bewertungen

- Consumption Savings Investment. ParadoxDokument46 SeitenConsumption Savings Investment. ParadoxChristine Joy LanabanNoch keine Bewertungen

- Chapter 3 Master BudgetDokument64 SeitenChapter 3 Master BudgetAklil TeganewNoch keine Bewertungen

- СHASE 20181218-statements-7322Dokument6 SeitenСHASE 20181218-statements-7322Myt WovenNoch keine Bewertungen

- Yale Lecture NotesDokument52 SeitenYale Lecture NotesK NorthNoch keine Bewertungen

- FABM2 Q3 Module 1Dokument27 SeitenFABM2 Q3 Module 1Sharlyn Marie An Noble-BadilloNoch keine Bewertungen

- Kumkum YadavDokument51 SeitenKumkum YadavHarshit KashyapNoch keine Bewertungen

- Semas Handout 5Dokument6 SeitenSemas Handout 5GONZALES, MICA ANGEL A.Noch keine Bewertungen

- Full Download Financial Management Theory and Practice 2nd Edition Brigham Test BankDokument33 SeitenFull Download Financial Management Theory and Practice 2nd Edition Brigham Test Bankjosephkvqhperez100% (34)

- Accounting 102 TermsDokument3 SeitenAccounting 102 TermsAlfred MartinNoch keine Bewertungen

- Unit - 3: Profits and Gains of Business or Profession: After Studying This Chapter, You Would Be Able ToDokument166 SeitenUnit - 3: Profits and Gains of Business or Profession: After Studying This Chapter, You Would Be Able ToSakshi SharmaNoch keine Bewertungen

- InvestorsDokument8 SeitenInvestorsJohahn MacabuhayNoch keine Bewertungen

- J R Mohapatra Co Chartered Accountants Hospital Road, Ranihat Cuttack - 753007Dokument1 SeiteJ R Mohapatra Co Chartered Accountants Hospital Road, Ranihat Cuttack - 753007amarnath ojhaNoch keine Bewertungen

- 2023 Tutorial 1 FMADokument4 Seiten2023 Tutorial 1 FMAĐỗ Ngọc ÁnhNoch keine Bewertungen

- Practice of Profitability RatiosDokument11 SeitenPractice of Profitability RatiosZarish AzharNoch keine Bewertungen

- Corporate RestructuringDokument19 SeitenCorporate RestructuringVaibhav KaushikNoch keine Bewertungen

- BMW Financial Statement Analysis PDFDokument27 SeitenBMW Financial Statement Analysis PDFsaurabhm707Noch keine Bewertungen

- Invoice 399924383597 5176902039Dokument1 SeiteInvoice 399924383597 5176902039mruliseNoch keine Bewertungen

- OutDokument10 SeitenOutroyhan bayuNoch keine Bewertungen

- Unit 1 Introduction of FinanceDokument53 SeitenUnit 1 Introduction of FinanceMalde KhuntiNoch keine Bewertungen

- "H. J. Heinz M&A": Case StudyDokument8 Seiten"H. J. Heinz M&A": Case StudySudhanva S 1510214100% (9)

- Financial Statement Analysis of Atlas Honda Motors, Indus Motors and Pak Suzuki Motors (Evidence From PakistanDokument17 SeitenFinancial Statement Analysis of Atlas Honda Motors, Indus Motors and Pak Suzuki Motors (Evidence From PakistanHabib JunejoNoch keine Bewertungen

- Onerous Contracts-Cost of Fulfilling A Contract Amendments To Ias 37Dokument6 SeitenOnerous Contracts-Cost of Fulfilling A Contract Amendments To Ias 37Suzy BaeNoch keine Bewertungen

- Analysis and Interpretation of FS 1Dokument13 SeitenAnalysis and Interpretation of FS 1marissa casareno almueteNoch keine Bewertungen

- SBI Mutual Funds: Financial ServicesDokument9 SeitenSBI Mutual Funds: Financial ServicesShivam MutkuleNoch keine Bewertungen

- FundedNext Trading Journal.Dokument57 SeitenFundedNext Trading Journal.Antonio FernandoNoch keine Bewertungen

- Fybcommathssem1unit1sharesandmutualfunds 2019 02-28-03 47Dokument5 SeitenFybcommathssem1unit1sharesandmutualfunds 2019 02-28-03 47princeNoch keine Bewertungen

- Tuto Akaun Bab 7 ArDokument5 SeitenTuto Akaun Bab 7 ArNoranis NajwaNoch keine Bewertungen

- Cash MemoDokument3 SeitenCash MemoHimanshu SinghNoch keine Bewertungen

- Graphic Era Hill University Sip ReportDokument54 SeitenGraphic Era Hill University Sip ReportdivsdaveNoch keine Bewertungen

- Goal of The Firm PDFDokument4 SeitenGoal of The Firm PDFSandyNoch keine Bewertungen

- Introduction To Financial AccountingDokument14 SeitenIntroduction To Financial AccountingMohd Azhari Hani SurayaNoch keine Bewertungen