Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- UBS Training #1Dokument243 SeitenUBS Training #1Galen Cheng100% (15)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- MC Test Bank - ch11 To 17 and CH 20,21Dokument39 SeitenMC Test Bank - ch11 To 17 and CH 20,21realdmanNoch keine Bewertungen

- Market StructureDokument21 SeitenMarket StructureAtharva Sawant100% (10)

- Project Finance: Aditya Agarwal Sandeep KaulDokument96 SeitenProject Finance: Aditya Agarwal Sandeep Kaulsguha123Noch keine Bewertungen

- Cox Ross 1976 - The Valuation of Options For Alternative Stochastic ProcessesDokument22 SeitenCox Ross 1976 - The Valuation of Options For Alternative Stochastic ProcessesxeperiaNoch keine Bewertungen

- BT TCDNDokument6 SeitenBT TCDNVõ Hoàng NhânNoch keine Bewertungen

- DTC PARTICIPANTS Listing DRS Direct Resgistration Services Limited ListDokument2 SeitenDTC PARTICIPANTS Listing DRS Direct Resgistration Services Limited Listjacque zidaneNoch keine Bewertungen

- Date of Valuation: Default AssumptionsDokument55 SeitenDate of Valuation: Default AssumptionsLevy ANoch keine Bewertungen

- Steve Meizinger: Trading Calendar Spreads Using ISE FX OptionsDokument43 SeitenSteve Meizinger: Trading Calendar Spreads Using ISE FX OptionsumashankarsNoch keine Bewertungen

- Recerse DCF Calculation Yellow Manual InputDokument6 SeitenRecerse DCF Calculation Yellow Manual InputErvin Khouw100% (1)

- FIN 286 - Valuation - G TwiteDokument7 SeitenFIN 286 - Valuation - G TwiteVasileNoch keine Bewertungen

- Goldman Sachs - Template - 2017Dokument17 SeitenGoldman Sachs - Template - 2017Akshay PilaniNoch keine Bewertungen

- Entrepreneurship TermsDokument1 SeiteEntrepreneurship TermsShin SimNoch keine Bewertungen

- By Dr. B. Krishna Reddy: Capital StructureDokument29 SeitenBy Dr. B. Krishna Reddy: Capital StructureMegha ChaudharyNoch keine Bewertungen

- Black Swan Capital July 10Dokument5 SeitenBlack Swan Capital July 10ZerohedgeNoch keine Bewertungen

- Selling: Janata Bank LimitedDokument1 SeiteSelling: Janata Bank Limitedsalam ahmedNoch keine Bewertungen

- Summary Apollo and London BerhadDokument2 SeitenSummary Apollo and London BerhadEdan Kon Hua EnNoch keine Bewertungen

- Ey frd42856 08 02 2022Dokument83 SeitenEy frd42856 08 02 2022Shri Ramanujar Dhaya AaraamudhamNoch keine Bewertungen

- Accounting 106 Quiz On Forwards, Futures and OptionsDokument1 SeiteAccounting 106 Quiz On Forwards, Futures and OptionsLee SuarezNoch keine Bewertungen

- Notes On AMLADokument2 SeitenNotes On AMLAMQA lawNoch keine Bewertungen

- Audit of InvestmentsDokument4 SeitenAudit of InvestmentsLloydNoch keine Bewertungen

- Chapter 2Dokument13 SeitenChapter 2Rinda Wulandari Ritonga1ANoch keine Bewertungen

- When Does Investor Sentiment Predict Stock Returns?: San-Lin Chung, Chi-Hsiou Hung, and Chung-Ying YehDokument40 SeitenWhen Does Investor Sentiment Predict Stock Returns?: San-Lin Chung, Chi-Hsiou Hung, and Chung-Ying YehddkillerNoch keine Bewertungen

- 10 "The Rediscovered Benjamin Graham"Dokument6 Seiten10 "The Rediscovered Benjamin Graham"X.r. GeNoch keine Bewertungen

- BAF 202 Corporate Finance and Financial ModellingDokument62 SeitenBAF 202 Corporate Finance and Financial ModellingRhinosmikeNoch keine Bewertungen

- Manual SuperFx (English)Dokument12 SeitenManual SuperFx (English)qais yasinNoch keine Bewertungen

- Oregon Investment Council 7 29Dokument95 SeitenOregon Investment Council 7 29Zerohedge100% (2)

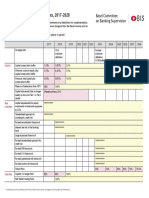

- Basel III Transitional Arrangements, 2017-2028: Basel Committee On Banking SupervisionDokument1 SeiteBasel III Transitional Arrangements, 2017-2028: Basel Committee On Banking SupervisiongoonNoch keine Bewertungen

- Cross Hedging: Nupur Gill 08D1328 Fin-2 (BBM D)Dokument9 SeitenCross Hedging: Nupur Gill 08D1328 Fin-2 (BBM D)Priti ChowdaryNoch keine Bewertungen

- Latih Soal Untuk Mhs Fin MGTDokument13 SeitenLatih Soal Untuk Mhs Fin MGTnajNoch keine Bewertungen