Das könnte Ihnen auch gefallen

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Von EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Bewertung: 5 von 5 Sternen5/5 (1)

- Public Expenditure PFM handbook-WB-2008 PDFDokument354 SeitenPublic Expenditure PFM handbook-WB-2008 PDFThơm TrùnNoch keine Bewertungen

- Auditing Past Exam QuestionsDokument6 SeitenAuditing Past Exam QuestionsAishwarya Yuvarajan50% (2)

- ISO 9001 Auditor Training Q&ADokument10 SeitenISO 9001 Auditor Training Q&AAli Zafar71% (7)

- Aas 29 Auditing in A Computer Information Systems EnvironmentDokument6 SeitenAas 29 Auditing in A Computer Information Systems EnvironmentRishabh GuptaNoch keine Bewertungen

- Arens Auditing16e SM 10Dokument30 SeitenArens Auditing16e SM 10김현중100% (1)

- Inception Report February 2012Dokument48 SeitenInception Report February 2012RUMMNoch keine Bewertungen

- BGA-HSSE-SAF-GL-1532 Evacuation, Muster, Escape - Rescue Rev01Dokument14 SeitenBGA-HSSE-SAF-GL-1532 Evacuation, Muster, Escape - Rescue Rev01TFattah100% (2)

- F20-AAUD Questions Dec08Dokument3 SeitenF20-AAUD Questions Dec08irfanki0% (1)

- Term Paper On Software Project ManagementDokument65 SeitenTerm Paper On Software Project ManagementManojitNoch keine Bewertungen

- Internship ReportDokument33 SeitenInternship ReportPriyanka A SNoch keine Bewertungen

- Occupational Safety and HealthDokument49 SeitenOccupational Safety and HealthNUR AFIFAH AHMAD SUBUKINoch keine Bewertungen

- Term Test 1Dokument3 SeitenTerm Test 1Hassan TanveerNoch keine Bewertungen

- Paper - 2: Auditing Questions: Accounting Treatment of The Above Receipt of Rs. 50 Lacs?Dokument20 SeitenPaper - 2: Auditing Questions: Accounting Treatment of The Above Receipt of Rs. 50 Lacs?tpsbtpsbtpsbNoch keine Bewertungen

- © The Institute of Chartered Accountants of IndiaDokument14 Seiten© The Institute of Chartered Accountants of IndiaGaihre रातो HULKNoch keine Bewertungen

- F MauditDokument4 SeitenF MauditPaulomee JhaveriNoch keine Bewertungen

- Audit Papers DecDokument164 SeitenAudit Papers DecKeshav SethiNoch keine Bewertungen

- Solutions To Auditing & Assurance Standards Nov 2009 - PCC/IPCCDokument9 SeitenSolutions To Auditing & Assurance Standards Nov 2009 - PCC/IPCCtanguduhareeshNoch keine Bewertungen

- Paper - 2: Auditing and Assurance QuestionsDokument20 SeitenPaper - 2: Auditing and Assurance Questions9331934775100% (1)

- Test Series: October, 2018 Mock Test Paper - 2 Final (New) Course: Group - I Paper - 3: Advanced Auditing and Professional EthicsDokument4 SeitenTest Series: October, 2018 Mock Test Paper - 2 Final (New) Course: Group - I Paper - 3: Advanced Auditing and Professional EthicsRobinxyNoch keine Bewertungen

- Question No.1 Is Compulsory. Answer Any Five From The RestDokument4 SeitenQuestion No.1 Is Compulsory. Answer Any Five From The RestAsim DasNoch keine Bewertungen

- Test Series: August, 2018 Mock Test Paper - 1 Final (New) Course: Group - I Paper - 3: Advanced Auditing and Professional EthicsDokument5 SeitenTest Series: August, 2018 Mock Test Paper - 1 Final (New) Course: Group - I Paper - 3: Advanced Auditing and Professional EthicsRobinxyNoch keine Bewertungen

- Final Auditing Question Paper - May - 2008Dokument5 SeitenFinal Auditing Question Paper - May - 2008Khristine CaserialNoch keine Bewertungen

- Advanced AuditingDokument14 SeitenAdvanced Auditingpriyeshrjain1Noch keine Bewertungen

- Ca Final May 2012 Exam Paper 3Dokument4 SeitenCa Final May 2012 Exam Paper 3Asim DasNoch keine Bewertungen

- May 2021 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeDokument19 SeitenMay 2021 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeVonnieNoch keine Bewertungen

- Advanced Auditing and Professional Ethics-3 QDokument16 SeitenAdvanced Auditing and Professional Ethics-3 QCAtestseriesNoch keine Bewertungen

- CODE: NF-3006 MARKS: 100 Final Advanced Auditing & Professional Ethics Syllabus:Audit - Module-I (As Per SM)Dokument18 SeitenCODE: NF-3006 MARKS: 100 Final Advanced Auditing & Professional Ethics Syllabus:Audit - Module-I (As Per SM)Devendra PatelNoch keine Bewertungen

- Ca Final (Advanced Auditing & Professional Ethics) Mock Test - IDokument18 SeitenCa Final (Advanced Auditing & Professional Ethics) Mock Test - ISrinivas RevankarNoch keine Bewertungen

- Test Series: March, 2013 Mock Test Paper - 2 Ipcc: Group - Ii Paper - 6: Auditing and AssuranceDokument3 SeitenTest Series: March, 2013 Mock Test Paper - 2 Ipcc: Group - Ii Paper - 6: Auditing and Assuranceguptafamily1992Noch keine Bewertungen

- Attention C.A. PCC & Ipcc Students: (No.1 Institute of Jharkhand)Dokument9 SeitenAttention C.A. PCC & Ipcc Students: (No.1 Institute of Jharkhand)Dharnis123Noch keine Bewertungen

- FINAL CA Audit INTEGRATED CASE STUDY BASED MCQs PDFDokument25 SeitenFINAL CA Audit INTEGRATED CASE STUDY BASED MCQs PDFJinal SanghviNoch keine Bewertungen

- 18552pcc Sugg Paper Nov09 2 PDFDokument14 Seiten18552pcc Sugg Paper Nov09 2 PDFGaurang AgarwalNoch keine Bewertungen

- Advanced Auditing and Professional Ethics - QDokument16 SeitenAdvanced Auditing and Professional Ethics - QCAtestseriesNoch keine Bewertungen

- Advanced Company Law & Practice: NoteDokument4 SeitenAdvanced Company Law & Practice: NoteabhinandNoch keine Bewertungen

- D11 AudDokument2 SeitenD11 AudNafees AhmedNoch keine Bewertungen

- All Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestDokument11 SeitenAll Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The Restritz meshNoch keine Bewertungen

- All Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestDokument11 SeitenAll Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestAditya MaheshwariNoch keine Bewertungen

- D11 AudDokument2 SeitenD11 AudadnanNoch keine Bewertungen

- CA IPCC Company Audit IIDokument50 SeitenCA IPCC Company Audit IIanon_672065362Noch keine Bewertungen

- Ep Module 1 Dec18 OsDokument81 SeitenEp Module 1 Dec18 OsHeena MistryNoch keine Bewertungen

- FR Power Full Book @mission - CA - Final PDFDokument422 SeitenFR Power Full Book @mission - CA - Final PDFlaksh sangtaniNoch keine Bewertungen

- Paper - 6: Auditing and Assurance: © The Institute of Chartered Accountants of IndiaDokument14 SeitenPaper - 6: Auditing and Assurance: © The Institute of Chartered Accountants of IndiaMuraliNoch keine Bewertungen

- All Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestDokument10 SeitenAll Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestMehul JainNoch keine Bewertungen

- Audit and Assurance: Certificate in Accounting and Finance Stage ExaminationDokument3 SeitenAudit and Assurance: Certificate in Accounting and Finance Stage ExaminationAdil AfridiNoch keine Bewertungen

- Assessment Test 1Dokument3 SeitenAssessment Test 1Arslan AhmadNoch keine Bewertungen

- CAF-09 Audit CompleteDokument36 SeitenCAF-09 Audit CompleteShehrozSTNoch keine Bewertungen

- All Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestDokument10 SeitenAll Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The Restritz meshNoch keine Bewertungen

- Scanner CAP II Audit and AssuranceDokument111 SeitenScanner CAP II Audit and Assuranceshankar k.c.Noch keine Bewertungen

- P6 Audit New Suggested CA Inter May 18Dokument14 SeitenP6 Audit New Suggested CA Inter May 18Rishabh jainNoch keine Bewertungen

- Pe2 Auditing Nov05Dokument14 SeitenPe2 Auditing Nov05api-3825774Noch keine Bewertungen

- 108 QP 1100Dokument4 Seiten108 QP 1100Rewa ShankarNoch keine Bewertungen

- CA (Final) Financial Reporting: InstructionsDokument4 SeitenCA (Final) Financial Reporting: InstructionsNakul GoyalNoch keine Bewertungen

- Audit ExamDokument13 SeitenAudit Examvyom rajNoch keine Bewertungen

- Case Study Based (Without Answers)Dokument14 SeitenCase Study Based (Without Answers)mshivam617Noch keine Bewertungen

- Auditing - MCQDokument14 SeitenAuditing - MCQProf. Subhassis PalNoch keine Bewertungen

- All Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestDokument10 SeitenAll Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The Restritz meshNoch keine Bewertungen

- All Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestDokument10 SeitenAll Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The Restritz meshNoch keine Bewertungen

- Tutorial On AuditingDokument6 SeitenTutorial On AuditingSyazliana KasimNoch keine Bewertungen

- CFAP 6 AARS Summer 2019Dokument3 SeitenCFAP 6 AARS Summer 2019shakilNoch keine Bewertungen

- PCC - Auditing - RTP - June 2009Dokument18 SeitenPCC - Auditing - RTP - June 2009Omnia HassanNoch keine Bewertungen

- CT AuditReg 4 QPDokument4 SeitenCT AuditReg 4 QPKhushi KapurNoch keine Bewertungen

- CAF 8 AUD Spring 2020Dokument5 SeitenCAF 8 AUD Spring 2020Huma BashirNoch keine Bewertungen

- Case Studies On Accounting & Auditing Standards: Lucknow Chartered Accountants' SocietyDokument12 SeitenCase Studies On Accounting & Auditing Standards: Lucknow Chartered Accountants' SocietyReema TembhurkarNoch keine Bewertungen

- Case Set 7 - Subsequent Events and Going ConcernDokument5 SeitenCase Set 7 - Subsequent Events and Going ConcernTimothy WongNoch keine Bewertungen

- Actuarial Society of India: ExaminationsDokument6 SeitenActuarial Society of India: ExaminationsRewa ShankarNoch keine Bewertungen

- AL Audit Assurance May June 2012Dokument3 SeitenAL Audit Assurance May June 2012Fakhrul IslamNoch keine Bewertungen

- Audit and Assurance: Certificate in Accounting and Finance Stage ExaminationDokument3 SeitenAudit and Assurance: Certificate in Accounting and Finance Stage ExaminationSYED ANEES ALINoch keine Bewertungen

- Adv Aud Final May08Dokument16 SeitenAdv Aud Final May08Fazi HaiderNoch keine Bewertungen

- Appendix 2 - ISO/IEC 17025:2017 Internal Audit Checklist: Clause Requirement YES NO CommentsDokument27 SeitenAppendix 2 - ISO/IEC 17025:2017 Internal Audit Checklist: Clause Requirement YES NO CommentsahmedNoch keine Bewertungen

- 02 Chapter 2 - Corporate Governance MechanismDokument19 Seiten02 Chapter 2 - Corporate Governance MechanismHanis ZahiraNoch keine Bewertungen

- REEM Document Submission GuildlinesDokument6 SeitenREEM Document Submission GuildlinesJiong SoonNoch keine Bewertungen

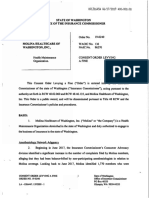

- Consent Order Levying Fine Molina Healthcare and Washington State Office of Insurance CommissionerDokument15 SeitenConsent Order Levying Fine Molina Healthcare and Washington State Office of Insurance CommissionernewscloudNoch keine Bewertungen

- Syllabus Bba 10042013Dokument40 SeitenSyllabus Bba 10042013Satyam DixitNoch keine Bewertungen

- Rough Transition To IATF 16949 Presentation For Customers-EstadisticaDokument35 SeitenRough Transition To IATF 16949 Presentation For Customers-EstadisticalabpresaNoch keine Bewertungen

- 3audit ReportsDokument67 Seiten3audit ReportsmuinbossNoch keine Bewertungen

- Leader Accountability For School Financial ManagementDokument16 SeitenLeader Accountability For School Financial ManagementallanrnmanalotoNoch keine Bewertungen

- Chapter 4 The Internal AssessmentDokument30 SeitenChapter 4 The Internal AssessmentRemy CaperochoNoch keine Bewertungen

- An Overview of The Banks and Other Financial Institutions Act 2020Dokument29 SeitenAn Overview of The Banks and Other Financial Institutions Act 2020Akin Akorede FolarinNoch keine Bewertungen

- FMMDokument124 SeitenFMMSiti Nur Ain RamliNoch keine Bewertungen

- Guidelines For System Operator Sabah F T Labuan 2023Dokument42 SeitenGuidelines For System Operator Sabah F T Labuan 2023Danial AmsyarNoch keine Bewertungen

- Ilo Osh 2001Dokument23 SeitenIlo Osh 2001Armand LiviuNoch keine Bewertungen

- Niagara Internship ReportDokument79 SeitenNiagara Internship ReportAnoshKhanNoch keine Bewertungen

- AAU Prospective Graduate 2022Dokument251 SeitenAAU Prospective Graduate 2022Getu100% (1)

- Assessing MaterialityDokument7 SeitenAssessing MaterialityThiên NguyễnNoch keine Bewertungen

- PD 692Dokument17 SeitenPD 692Larry TobiasNoch keine Bewertungen

- Module 6 - Risk AssuranceDokument8 SeitenModule 6 - Risk AssuranceMarjon DimafilisNoch keine Bewertungen

- Bank Audit - Opportunities and Concerns: 1) IntroductionDokument14 SeitenBank Audit - Opportunities and Concerns: 1) IntroductionSURYA DEEPAK BEHERANoch keine Bewertungen

- Fig 4.1 02 PDCA EnMSDokument2 SeitenFig 4.1 02 PDCA EnMSRavi ShankarNoch keine Bewertungen

- Unit 8Dokument22 SeitenUnit 8eldorado.se69Noch keine Bewertungen