Das könnte Ihnen auch gefallen

- Solution 2Dokument3 SeitenSolution 2AbhishekKumarNoch keine Bewertungen

- 4 Completing The Accounting Cycle PartDokument1 Seite4 Completing The Accounting Cycle PartTalionNoch keine Bewertungen

- Cheng Company: Selected Transactions From The Journal of June Feldman, Investment Broker, Are Presented BelowDokument4 SeitenCheng Company: Selected Transactions From The Journal of June Feldman, Investment Broker, Are Presented BelowHà Anh Đỗ100% (1)

- Management Accounting I Construction of Balance Sheet (PGP22: Section A, B & C)Dokument7 SeitenManagement Accounting I Construction of Balance Sheet (PGP22: Section A, B & C)saurabhNoch keine Bewertungen

- 07 Activity 1Dokument2 Seiten07 Activity 1Eva Mae Fernandez OcularNoch keine Bewertungen

- Financial Accounting: Chapter # 01 Accounting and The Business EnvoirmentDokument11 SeitenFinancial Accounting: Chapter # 01 Accounting and The Business Envoirmentalihaider comsatsNoch keine Bewertungen

- CORPORATION LIQUIDATION - AcctnfDokument2 SeitenCORPORATION LIQUIDATION - AcctnfJewel CabigonNoch keine Bewertungen

- Tutorial 1Dokument2 SeitenTutorial 1KHANH Du Ngoc0% (1)

- Solution Manual For College Accounting 22nd EditionDokument18 SeitenSolution Manual For College Accounting 22nd EditionMichaelRamseydgjk100% (38)

- College Accounting Chapters 1-27-22nd Edition Heintz Solutions ManualDokument35 SeitenCollege Accounting Chapters 1-27-22nd Edition Heintz Solutions Manualengildhebraism.he3o100% (22)

- College Accounting 21st Edition Heintz Solutions ManualDokument35 SeitenCollege Accounting 21st Edition Heintz Solutions Manualniblicktartar.nevn3100% (19)

- Dwnload Full College Accounting 21st Edition Heintz Solutions Manual PDFDokument35 SeitenDwnload Full College Accounting 21st Edition Heintz Solutions Manual PDFvintagerarbored.le0lr100% (9)

- Form Latihan Bab 2 Dan 3Dokument10 SeitenForm Latihan Bab 2 Dan 3Gogo LinaNoch keine Bewertungen

- Entrep 07 Activity 1Dokument2 SeitenEntrep 07 Activity 1Ronald varrie BautistaNoch keine Bewertungen

- College Accounting Chapters 1-27-21st Edition Heintz Solutions ManualDokument35 SeitenCollege Accounting Chapters 1-27-21st Edition Heintz Solutions Manualengildhebraism.he3o100% (14)

- Week 4 Solutions PDFDokument4 SeitenWeek 4 Solutions PDFchi_nguyen_100Noch keine Bewertungen

- The Accounting Cycle: Reporting Financial ResultsDokument8 SeitenThe Accounting Cycle: Reporting Financial ResultsOmar KhanNoch keine Bewertungen

- The Trial Balance Columns of The Worksheet For Warren Roofi NG at March 31Dokument1 SeiteThe Trial Balance Columns of The Worksheet For Warren Roofi NG at March 31MD. RASEL HOSSAINNoch keine Bewertungen

- Solution Manual For College Accounting Chapters 1-15-22nd Edition Heintz Parry ISBN 1305666178 9781305666177Dokument36 SeitenSolution Manual For College Accounting Chapters 1-15-22nd Edition Heintz Parry ISBN 1305666178 9781305666177ralphadamsyorbpqmzia96% (23)

- Measuring Business IncomeDokument3 SeitenMeasuring Business Incomeeater PeopleNoch keine Bewertungen

- Amper Accounting Activity2Dokument5 SeitenAmper Accounting Activity2Realle Rainne CruzNoch keine Bewertungen

- College Accounting 21st Edition Heintz Solutions ManualDokument25 SeitenCollege Accounting 21st Edition Heintz Solutions ManualBrianHudsonoqer98% (59)

- Akuntansi Pengantar 6Dokument3 SeitenAkuntansi Pengantar 6WiwitvlogNoch keine Bewertungen

- LkhgyDokument2 SeitenLkhgyDynNoch keine Bewertungen

- 07 Activity 1Dokument2 Seiten07 Activity 1Althea NovidaNoch keine Bewertungen

- Yolanda Reality Work Sheet For The Month Ended April 2020Dokument2 SeitenYolanda Reality Work Sheet For The Month Ended April 2020Hannah DimalibotNoch keine Bewertungen

- 07 Activity 1Dokument2 Seiten07 Activity 1jezrel mauricio100% (1)

- 07 Activity 1Dokument2 Seiten07 Activity 1Ronald varrie BautistaNoch keine Bewertungen

- CH 02Dokument4 SeitenCH 02flrnciairnNoch keine Bewertungen

- Activity - Preparation of Financial StatementsDokument4 SeitenActivity - Preparation of Financial StatementsJoy ValenciaNoch keine Bewertungen

- Problem Sheet 4 Summer 22Dokument4 SeitenProblem Sheet 4 Summer 22Md Tanvir AhmedNoch keine Bewertungen

- Week 4 PDF FreeDokument5 SeitenWeek 4 PDF FreeM. Gibran KhalilNoch keine Bewertungen

- Problem No 5 (Acctg. 1)Dokument5 SeitenProblem No 5 (Acctg. 1)Ash imoNoch keine Bewertungen

- 05 Completing The Accounting Cycle PROBLEMSDokument5 Seiten05 Completing The Accounting Cycle PROBLEMSbetlogNoch keine Bewertungen

- Mittens Kittens CompanyDokument5 SeitenMittens Kittens CompanyDianna EsmerayNoch keine Bewertungen

- P2Dokument40 SeitenP2Michiko Kyung-soonNoch keine Bewertungen

- Accounting Cycle Week 2 ReviewerDokument11 SeitenAccounting Cycle Week 2 ReviewerVinz Danzel BialaNoch keine Bewertungen

- Accounting Assignment CHP 1-1Dokument11 SeitenAccounting Assignment CHP 1-1MUHAMMAD AMMAD ARSHADNoch keine Bewertungen

- Assignment/ TugasanDokument21 SeitenAssignment/ Tugasanhafiz azuanNoch keine Bewertungen

- Baliwag Polytechnic College Elective: Fundamentals of Abm 1 Mr. Jomar V. Villena, CpaDokument1 SeiteBaliwag Polytechnic College Elective: Fundamentals of Abm 1 Mr. Jomar V. Villena, CpaJomar VillenaNoch keine Bewertungen

- 07 Activity 1-EnTREPDokument2 Seiten07 Activity 1-EnTREPClar PachecoNoch keine Bewertungen

- Rivera and Santos PartnershipDokument31 SeitenRivera and Santos PartnershipDaneca GallardoNoch keine Bewertungen

- Financial PositionDokument2 SeitenFinancial PositionKatherine BorjaNoch keine Bewertungen

- Solution Manual For College Accounting Chapters 1-27-22nd Edition by Heintz and Parry ISBN 130566616X 9781305666160Dokument36 SeitenSolution Manual For College Accounting Chapters 1-27-22nd Edition by Heintz and Parry ISBN 130566616X 9781305666160ralphadamsyorbpqmzia100% (31)

- Gmernacej W5C5 AssigmentOLDDokument6 SeitenGmernacej W5C5 AssigmentOLDalmaNoch keine Bewertungen

- Chapter 08Dokument26 SeitenChapter 08Dan ChuaNoch keine Bewertungen

- Mansa Building Case - GROUP GDokument10 SeitenMansa Building Case - GROUP GSanyam RahejaNoch keine Bewertungen

- Ch23 StatementofCashFlowExamples Zeke and ZoeDokument4 SeitenCh23 StatementofCashFlowExamples Zeke and ZoeHossein ParvardehNoch keine Bewertungen

- Question Bbaw2103 Financial AccountingDokument9 SeitenQuestion Bbaw2103 Financial AccountingZakey Zainal0% (1)

- 07 Activity 1 (24) .DocsDokument2 Seiten07 Activity 1 (24) .DocsNICOOR YOWWNoch keine Bewertungen

- Mini Exercise Answer KeyDokument3 SeitenMini Exercise Answer KeyKaren TumabiniNoch keine Bewertungen

- FAR Review MaterialDokument22 SeitenFAR Review MaterialAntonette Eve CelomineNoch keine Bewertungen

- BAAB1014 Assignment EliteDokument5 SeitenBAAB1014 Assignment Elitejinosini ramadasNoch keine Bewertungen

- Basic Accounting Equation Exercises 2Dokument2 SeitenBasic Accounting Equation Exercises 2Ace Joseph TabaderoNoch keine Bewertungen

- Single Entry AccountingDokument12 SeitenSingle Entry AccountingArjun ThawaniNoch keine Bewertungen

- Accounting P1 Nov 2022Dokument14 SeitenAccounting P1 Nov 2022Lesego TsatsinyaneNoch keine Bewertungen

- Sy Final AccountDokument8 SeitenSy Final Accountsmit9993Noch keine Bewertungen

- Bacayo 07 Activity 1 EntrepDokument3 SeitenBacayo 07 Activity 1 EntrepDavid GutierrezNoch keine Bewertungen

- Managing County Assets and Liabilities in Kenya: Postdevolution Challenges and ResponsesVon EverandManaging County Assets and Liabilities in Kenya: Postdevolution Challenges and ResponsesNoch keine Bewertungen

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersVon EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNoch keine Bewertungen

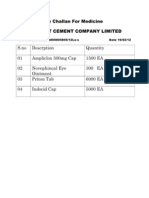

- Delivery Challan For MedicineDokument1 SeiteDelivery Challan For MedicineSAMEERADEELNoch keine Bewertungen

- Chapter - 1 Introduction of The Study: Section # 1Dokument16 SeitenChapter - 1 Introduction of The Study: Section # 1SAMEERADEELNoch keine Bewertungen

- UFone Assignment by Shakeel AhmadDokument46 SeitenUFone Assignment by Shakeel AhmadSAMEERADEEL50% (6)

- EducationDokument3 SeitenEducationSAMEERADEELNoch keine Bewertungen

- Audio-Visual Aids: Introduction: Modern Approaches To Teaching Unit 9Dokument16 SeitenAudio-Visual Aids: Introduction: Modern Approaches To Teaching Unit 9SAMEERADEELNoch keine Bewertungen

- Paper Presented at The Fourth National Competitiveness Forum at Serena Hotel, Kampala On 16 October, 2009Dokument4 SeitenPaper Presented at The Fourth National Competitiveness Forum at Serena Hotel, Kampala On 16 October, 2009Real TrekstarNoch keine Bewertungen

- English For Logistics VocabularyDokument2 SeitenEnglish For Logistics VocabularyOla WodaNoch keine Bewertungen

- Business Ethics - Group 1 Case Analysis: Theranos: The Unicorn That Wasn'tDokument8 SeitenBusiness Ethics - Group 1 Case Analysis: Theranos: The Unicorn That Wasn'tARANYA GHOSHNoch keine Bewertungen

- CELL PHONES SUPPORT ECONOMIC DEVELOPMENT (Case Study)Dokument4 SeitenCELL PHONES SUPPORT ECONOMIC DEVELOPMENT (Case Study)jan martinNoch keine Bewertungen

- Engaging With The Danish Young GenerationDokument26 SeitenEngaging With The Danish Young GenerationQuang Minh NguyenNoch keine Bewertungen

- Material Requirements Planning (MRP) and ERPDokument86 SeitenMaterial Requirements Planning (MRP) and ERPGautam JrNoch keine Bewertungen

- Imports/Exports Procedures - Uganda Import Procedure: Required DocumentsDokument3 SeitenImports/Exports Procedures - Uganda Import Procedure: Required DocumentsIvan TumazeNoch keine Bewertungen

- Test I - Multiple Choice - TheoryDokument6 SeitenTest I - Multiple Choice - Theorycute meNoch keine Bewertungen

- IB Economics IA 2Dokument4 SeitenIB Economics IA 2SpicyChildrenNoch keine Bewertungen

- Treasury ChallanDokument1 SeiteTreasury ChallanMainong JenbumNoch keine Bewertungen

- 2005T148 Ngezi Concentrator Insurance Spares Chemicals and Gas Cylinders Sheds TenderDokument56 Seiten2005T148 Ngezi Concentrator Insurance Spares Chemicals and Gas Cylinders Sheds TenderTatenda Katurura KaysNoch keine Bewertungen

- Uco Rtgs FormDokument2 SeitenUco Rtgs FormdevchandvirjiNoch keine Bewertungen

- Jefferson County Clerk's Office Fraud Alert - RecordingsDokument1 SeiteJefferson County Clerk's Office Fraud Alert - RecordingsNewzjunkyNoch keine Bewertungen

- Chapter 16Dokument25 SeitenChapter 16Wedaje AlemayehuNoch keine Bewertungen

- The Home Depot IncDokument12 SeitenThe Home Depot IncKhushbooNoch keine Bewertungen

- Eligible Collaterals Directive 05 JUL 2022Dokument22 SeitenEligible Collaterals Directive 05 JUL 2022Fuaad DodooNoch keine Bewertungen

- CV Unit 7Dokument21 SeitenCV Unit 7amrutraj gNoch keine Bewertungen

- Emerging Trends in Real Estate 2023 ReportDokument123 SeitenEmerging Trends in Real Estate 2023 ReportSushant VermaNoch keine Bewertungen

- P.P.Savani Chaitanya Vidya Sankul, Cbse Ch. 5 Organising (Notes) STD: - 12 Subject: - Business StudiesDokument8 SeitenP.P.Savani Chaitanya Vidya Sankul, Cbse Ch. 5 Organising (Notes) STD: - 12 Subject: - Business StudiesbholaprasadpandeyNoch keine Bewertungen

- Zomato Food Order: Summary and Receipt: Item Quantity Unit Price Total PriceDokument1 SeiteZomato Food Order: Summary and Receipt: Item Quantity Unit Price Total PriceSurbhi SandhuNoch keine Bewertungen

- Full Assignment Purchasing Management and Supply ChainDokument105 SeitenFull Assignment Purchasing Management and Supply ChainMaizurah AbdullahNoch keine Bewertungen

- Outer-Rim CantinaDokument19 SeitenOuter-Rim CantinaJoão Pedro ValeNoch keine Bewertungen

- Tybaf Sem5 Fa-Vi Nov19Dokument6 SeitenTybaf Sem5 Fa-Vi Nov19Hasan ShahNoch keine Bewertungen

- Conformity AssessmentDokument45 SeitenConformity Assessmentboborg8792Noch keine Bewertungen

- Capital Budgeting Under UncertaintyDokument80 SeitenCapital Budgeting Under UncertaintyAndualem ZenebeNoch keine Bewertungen

- ER - Diagrams: Employee Management SystemDokument2 SeitenER - Diagrams: Employee Management SystemAbby DukeworthNoch keine Bewertungen

- AP Module 01 - Accounting Changes and ErrorsDokument10 SeitenAP Module 01 - Accounting Changes and ErrorsjasfNoch keine Bewertungen

- Mock Test of Jaiib Principles & Practices of Banking.: AnswerDokument12 SeitenMock Test of Jaiib Principles & Practices of Banking.: Answeraao wacNoch keine Bewertungen

- Loans and Advances Final Version 2 PowerpointDokument75 SeitenLoans and Advances Final Version 2 PowerpointMd Tanjir Islam JerryNoch keine Bewertungen

- Jesse A Stancil: On-Line Self Select PIN Without Direct Debit Tax Return Signature/Consent To DisclosureDokument11 SeitenJesse A Stancil: On-Line Self Select PIN Without Direct Debit Tax Return Signature/Consent To DisclosureJesse StancilNoch keine Bewertungen