Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Making An Impact That MattersDokument32 SeitenMaking An Impact That MatterssaddamNoch keine Bewertungen

- Rancho Foods Deposits All Cash Receipts Each Wednesday and FridayDokument1 SeiteRancho Foods Deposits All Cash Receipts Each Wednesday and FridayAmit PandeyNoch keine Bewertungen

- Germany SpainDokument18 SeitenGermany SpainsriramNoch keine Bewertungen

- Management Review in 2020Dokument13 SeitenManagement Review in 2020Giang Luu100% (1)

- RandommmmmDokument8 SeitenRandommmmmMmNoch keine Bewertungen

- Standards On Auditing: Presented By: Nikhil Panicker Manaswi Tripathi Moderator: CA. Abhay ChhajedDokument85 SeitenStandards On Auditing: Presented By: Nikhil Panicker Manaswi Tripathi Moderator: CA. Abhay Chhajedneelam mishraNoch keine Bewertungen

- Auditing of ConsolidationDokument3 SeitenAuditing of Consolidationiskandar027Noch keine Bewertungen

- Audit Testbank-Bobadilla PDFDokument560 SeitenAudit Testbank-Bobadilla PDFNir Noel Aquino100% (12)

- Substantive Testing and DocumentationDokument3 SeitenSubstantive Testing and DocumentationRose Medina BarondaNoch keine Bewertungen

- Internal Audit Checklist Questions - QMSDokument22 SeitenInternal Audit Checklist Questions - QMSAshiq Maan100% (2)

- Big Bazaar ErpDokument12 SeitenBig Bazaar ErpVarun Tripathi100% (1)

- Short Notes of AuditingDokument3 SeitenShort Notes of AuditingMahmudul HasanNoch keine Bewertungen

- Sridhar Reddy - Alla ResumeDokument5 SeitenSridhar Reddy - Alla ResumeVijayNoch keine Bewertungen

- Multi Task Questions.Dokument8 SeitenMulti Task Questions.wilbertNoch keine Bewertungen

- Is Enhanced Audit Quality Associated With Greater Real Earnings Management?Dokument22 SeitenIs Enhanced Audit Quality Associated With Greater Real Earnings Management?Darvin AnanthanNoch keine Bewertungen

- Mohammed Rafi PDFDokument3 SeitenMohammed Rafi PDFYamini SharmaNoch keine Bewertungen

- Whitepaper BRC Study of Unannounced AuditsDokument19 SeitenWhitepaper BRC Study of Unannounced AuditsDavidHernandezNoch keine Bewertungen

- Hillsborough County Finance Report - Final 2020xDokument33 SeitenHillsborough County Finance Report - Final 2020xABC Action News100% (1)

- CONSTITUTIONDokument20 SeitenCONSTITUTIONAkim LatifouNoch keine Bewertungen

- 2023.02.01 Lecture - Audit of Expenditure and Disbursement CycleDokument1 Seite2023.02.01 Lecture - Audit of Expenditure and Disbursement Cyclemisonim.eNoch keine Bewertungen

- Accenture Top Healthcare ConsultingDokument1 SeiteAccenture Top Healthcare ConsultingWasif HudaNoch keine Bewertungen

- EDM05 Stakeholder TransparencyDokument9 SeitenEDM05 Stakeholder TransparencynoneNoch keine Bewertungen

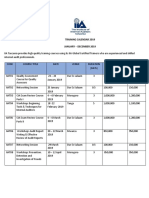

- IIA Calender 2019Dokument5 SeitenIIA Calender 2019MtanaNoch keine Bewertungen

- Clinical (Practice) Audit: A Guide For PCSDokument10 SeitenClinical (Practice) Audit: A Guide For PCSMohsin IslamNoch keine Bewertungen

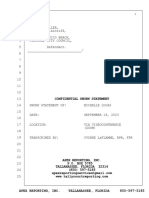

- Mexico Beach Sworn StatementDokument49 SeitenMexico Beach Sworn StatementWJHG - TVNoch keine Bewertungen

- Muhammad Usman Saleem: House No. P-754, Peoples Colony No.2 Raja Chowk, AisalabadDokument3 SeitenMuhammad Usman Saleem: House No. P-754, Peoples Colony No.2 Raja Chowk, AisalabadUsmän MïrżäNoch keine Bewertungen

- Purchase-To-Pay Process Map: Inventory DepartmentDokument2 SeitenPurchase-To-Pay Process Map: Inventory DepartmentDanielle MarundanNoch keine Bewertungen

- What Is Cost AccountingDokument3 SeitenWhat Is Cost AccountingWajahat BhattiNoch keine Bewertungen

- ARCH Log BookDokument34 SeitenARCH Log BookJared MakoriNoch keine Bewertungen

- NCW Format Application NCWDokument4 SeitenNCW Format Application NCWAnonymous WtjVcZCgNoch keine Bewertungen