Das könnte Ihnen auch gefallen

- Fertilizer Sector: FFC Result PreviewDokument1 SeiteFertilizer Sector: FFC Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFBL Result PreviewDokument1 SeiteFertilizer Sector: FFBL Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: Dispatches Slow Down ContinuesDokument1 SeiteCement Sector: Dispatches Slow Down ContinuesMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFBL - A Good BUYDokument1 SeiteFertilizer Sector: FFBL - A Good BUYMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFBL Result PreviewDokument1 SeiteFertilizer Sector: FFBL Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: ACPL Result PreviewDokument1 SeiteCement Sector: ACPL Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- 08 Dec 2010Dokument1 Seite08 Dec 2010Muhammad Sarfraz AbbasiNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Regional Trading Blocs & Impact On Marketing: by - Prenitha BDokument9 SeitenRegional Trading Blocs & Impact On Marketing: by - Prenitha BPrenithaNoch keine Bewertungen

- Economics Class 12 Project On DemonetisationDokument8 SeitenEconomics Class 12 Project On DemonetisationHargun Virk25% (4)

- Chapter 2 Marketing EnvironmentDokument26 SeitenChapter 2 Marketing EnvironmentBích ChâuNoch keine Bewertungen

- MCQs by DanielDokument74 SeitenMCQs by DanielAbubakar Butt100% (1)

- Indonesia Jakarta Rental Apartment Q1 2021Dokument2 SeitenIndonesia Jakarta Rental Apartment Q1 2021Grace SaragihNoch keine Bewertungen

- Ethiopia at A GlanceDokument3 SeitenEthiopia at A GlanceTSEDEKENoch keine Bewertungen

- FullReport AES2021Dokument108 SeitenFullReport AES2021clement3176Noch keine Bewertungen

- Bar ChartDokument3 SeitenBar ChartVanh VũNoch keine Bewertungen

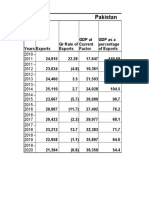

- Circular Debt in PakistanDokument17 SeitenCircular Debt in PakistanHira Noor91% (11)

- Form Number AR/3: Ministry of Finance Income and Sales Tax DepartmentDokument2 SeitenForm Number AR/3: Ministry of Finance Income and Sales Tax Departmentsufian olimatNoch keine Bewertungen

- One Nation One Ration CardDokument10 SeitenOne Nation One Ration CardPrashant ThoratNoch keine Bewertungen

- 21.10 M - D T - F T T: Mrunal's Economy Pillar#2A: Budget Revenue Part Tax-Receipts Page 123Dokument3 Seiten21.10 M - D T - F T T: Mrunal's Economy Pillar#2A: Budget Revenue Part Tax-Receipts Page 123Washim Alam50CNoch keine Bewertungen

- Forward Rates - August 6 2019Dokument2 SeitenForward Rates - August 6 2019Tiso Blackstar GroupNoch keine Bewertungen

- London Stock ExchangeDokument9 SeitenLondon Stock ExchangeVika IgnatenkoNoch keine Bewertungen

- MicroWatch Issue 59 - Q1 2021Dokument20 SeitenMicroWatch Issue 59 - Q1 2021Entertainment worldNoch keine Bewertungen

- Global North and The First World CountriesDokument2 SeitenGlobal North and The First World CountriesErica ChavezNoch keine Bewertungen

- Project Excel FileDokument7 SeitenProject Excel FileMoazzam MangiNoch keine Bewertungen

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument25 SeitenDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceVicky GunaNoch keine Bewertungen

- Overeign Funds Flow Ndia Replaces Hina As Most Sought After DestinationDokument18 SeitenOvereign Funds Flow Ndia Replaces Hina As Most Sought After DestinationABHINAV DEWALIYANoch keine Bewertungen

- The Service Sector Team's Script For NewscastingDokument2 SeitenThe Service Sector Team's Script For NewscastingBrent Luna DelmoNoch keine Bewertungen

- Break Even AnalysisDokument13 SeitenBreak Even Analysissuchipatel100% (2)

- Rio de Janeiro: Office Q3 2020Dokument4 SeitenRio de Janeiro: Office Q3 2020Alessandro BarillàNoch keine Bewertungen

- Economic Calendar Economic CalendarDokument5 SeitenEconomic Calendar Economic CalendarAtulNoch keine Bewertungen

- Federal Board of Revenue FBR McqsDokument10 SeitenFederal Board of Revenue FBR McqsHassan Ali0% (3)

- Income Inequality in IndiaDokument2 SeitenIncome Inequality in IndiaAnisha JosephNoch keine Bewertungen

- Economy To Enter Goldilocks PhaseDokument1 SeiteEconomy To Enter Goldilocks PhaseNeeraj GargNoch keine Bewertungen

- International Trade FairDokument4 SeitenInternational Trade FairAlonny100% (1)

- Taxation SystemDokument3 SeitenTaxation SystemSaqibMahmoodNoch keine Bewertungen

- Senator Schumer - Federal Aid Request LetterDokument2 SeitenSenator Schumer - Federal Aid Request LetterDaily FreemanNoch keine Bewertungen

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument5 SeitenStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSandesh Pujari100% (1)