Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- US Internal Revenue Service: 2290rulesty2007v4 0Dokument6 SeitenUS Internal Revenue Service: 2290rulesty2007v4 0IRSNoch keine Bewertungen

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Objectives Report To Congress v2Dokument153 Seiten2008 Objectives Report To Congress v2IRSNoch keine Bewertungen

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Credit Card Bulk Provider RequirementsDokument112 Seiten2008 Credit Card Bulk Provider RequirementsIRSNoch keine Bewertungen

- 2008 Data DictionaryDokument260 Seiten2008 Data DictionaryIRSNoch keine Bewertungen

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Weill Routh File 2Dokument46 SeitenWeill Routh File 2the kingfishNoch keine Bewertungen

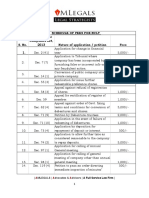

- Schedule of Fees in NCLT 1Dokument4 SeitenSchedule of Fees in NCLT 1Lavkesh BhambhaniNoch keine Bewertungen

- Case Digest2Dokument26 SeitenCase Digest2Catherine KimNoch keine Bewertungen

- First Counterclaim For Fraud and MisrepresentationDokument3 SeitenFirst Counterclaim For Fraud and Misrepresentationidris2111Noch keine Bewertungen

- Teaching Week 4 - Torts 2 (Other Torts)Dokument31 SeitenTeaching Week 4 - Torts 2 (Other Torts)Click HereNoch keine Bewertungen

- Sarsosa Vda de Barsobia Vs Cuenco To Ong Ching Po Vs CADokument4 SeitenSarsosa Vda de Barsobia Vs Cuenco To Ong Ching Po Vs CAMariaAyraCelinaBatacanNoch keine Bewertungen

- Ac Ransom Vs NLRC DigestDokument2 SeitenAc Ransom Vs NLRC DigestPMV100% (2)

- Processual PresumptionDokument2 SeitenProcessual Presumptionaileen reyesNoch keine Bewertungen

- Chapter 8 - Utilitarianism For June 3, 2023Dokument52 SeitenChapter 8 - Utilitarianism For June 3, 2023JeffersonNoch keine Bewertungen

- ASID 2011 - Code of Ethics and Professional ConductDokument10 SeitenASID 2011 - Code of Ethics and Professional ConductMo HANoch keine Bewertungen

- Tatad Vs Secretary Case DigestDokument3 SeitenTatad Vs Secretary Case DigestEsnani MaiNoch keine Bewertungen

- The Muslim Concept of Surrender To God: by Mark NygardDokument6 SeitenThe Muslim Concept of Surrender To God: by Mark NygardmaghniavNoch keine Bewertungen

- Seaoil Petroleum Corporation vs. Autocorp Group (164326) 569 SCRA 387 (2008)Dokument16 SeitenSeaoil Petroleum Corporation vs. Autocorp Group (164326) 569 SCRA 387 (2008)Joe PoNoch keine Bewertungen

- Caltex V PNOCDokument2 SeitenCaltex V PNOCI.G. Mingo MulaNoch keine Bewertungen

- Murder Actus Reus Activity PPDokument15 SeitenMurder Actus Reus Activity PPapi-248690201Noch keine Bewertungen

- Good Governance CompleteDokument19 SeitenGood Governance CompleteKaleem MarwatNoch keine Bewertungen

- Eo No. 1008Dokument4 SeitenEo No. 1008Raine Buenaventura-EleazarNoch keine Bewertungen

- Ipl CaseDokument4 SeitenIpl CasestephclloNoch keine Bewertungen

- NSTP 1 Revision 02 2022 23Dokument190 SeitenNSTP 1 Revision 02 2022 23Jayson LanuzaNoch keine Bewertungen

- Xcentric V Goddeau ComplaintDokument11 SeitenXcentric V Goddeau ComplaintEric GoldmanNoch keine Bewertungen

- Philcom Employees Union vs. Phil Global CommunicationsDokument2 SeitenPhilcom Employees Union vs. Phil Global CommunicationsIsay YasonNoch keine Bewertungen

- Special Power of AttorneyDokument4 SeitenSpecial Power of AttorneyMPDO ManticaoNoch keine Bewertungen

- Ventura County Rules of CourtDokument100 SeitenVentura County Rules of CourtNameNoch keine Bewertungen

- Crim Law Deskbook V 1Dokument901 SeitenCrim Law Deskbook V 1jamesbeaudoinNoch keine Bewertungen

- Roque, Jr. vs. COMELECDokument5 SeitenRoque, Jr. vs. COMELECMonikka DeleraNoch keine Bewertungen

- Application For Rescission of Judgemnt ZimnatDokument9 SeitenApplication For Rescission of Judgemnt ZimnatAJ AJNoch keine Bewertungen

- Quit Claim FormDokument2 SeitenQuit Claim FormAngelica CruzNoch keine Bewertungen

- 18 Dawa vs. Judge de AsaDokument5 Seiten18 Dawa vs. Judge de AsaHv EstokNoch keine Bewertungen

- OCA Circular 93-20 PDFDokument4 SeitenOCA Circular 93-20 PDFDaniel Al DelfinNoch keine Bewertungen

- Ac 10299Dokument1 SeiteAc 10299April CelestinoNoch keine Bewertungen