Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- 2020 Tax DelinquencyDokument27 Seiten2020 Tax DelinquencyKentFaulk75% (8)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDokument15 Seiten6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Federal Tax Form W-4Dokument4 SeitenFederal Tax Form W-4Mitch SabioNoch keine Bewertungen

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Objectives Report To Congress v2Dokument153 Seiten2008 Objectives Report To Congress v2IRSNoch keine Bewertungen

- US Internal Revenue Service: 2290rulesty2007v4 0Dokument6 SeitenUS Internal Revenue Service: 2290rulesty2007v4 0IRSNoch keine Bewertungen

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Credit Card Bulk Provider RequirementsDokument112 Seiten2008 Credit Card Bulk Provider RequirementsIRSNoch keine Bewertungen

- 2008 Data DictionaryDokument260 Seiten2008 Data DictionaryIRSNoch keine Bewertungen

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDokument71 SeitenTratamentul Total Al CanceruluiAntal98% (98)

- BE-Way Bill SystemDokument2 SeitenBE-Way Bill SystemKrishna Computer DakorNoch keine Bewertungen

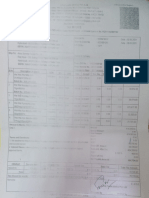

- Payslip 20200731Dokument1 SeitePayslip 20200731Sg BalajiNoch keine Bewertungen

- Important Information To Include On Your Tax Return Before Sending It To UsDokument10 SeitenImportant Information To Include On Your Tax Return Before Sending It To UsHagiNoch keine Bewertungen

- Banco de Oro, Et Al vs. Republic of The Philippines, Et AlDokument2 SeitenBanco de Oro, Et Al vs. Republic of The Philippines, Et AlJerome GonzalesNoch keine Bewertungen

- Akash - Salary SlipDokument2 SeitenAkash - Salary Slipzingo bingoNoch keine Bewertungen

- Instructions For Form 8962Dokument20 SeitenInstructions For Form 8962HNoch keine Bewertungen

- OrganicHarvest Invoice 1679174266-17Dokument1 SeiteOrganicHarvest Invoice 1679174266-17Dhruv and pari showtimeNoch keine Bewertungen

- FabHotels PI uhNfS 2324 00268 InvoiceDokument2 SeitenFabHotels PI uhNfS 2324 00268 Invoiceankitsahoo62Noch keine Bewertungen

- 40 Nippon Life V CIRDokument2 Seiten40 Nippon Life V CIRMae SampangNoch keine Bewertungen

- BIR Form 1701 2013 - Tax Deduction - Revenue PDFDokument1 SeiteBIR Form 1701 2013 - Tax Deduction - Revenue PDFsidneyNoch keine Bewertungen

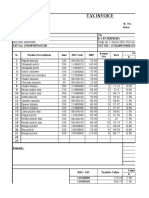

- Tax Invoice: % Rate CGST Sr. Product Description Gms HSN Code MRP Return QtyDokument4 SeitenTax Invoice: % Rate CGST Sr. Product Description Gms HSN Code MRP Return QtyJai GaneshNoch keine Bewertungen

- Iran Tax TreatyDokument3 SeitenIran Tax TreatyHossein DavaniNoch keine Bewertungen

- Income Tax Payment Challan: PSID #: 144740076Dokument1 SeiteIncome Tax Payment Challan: PSID #: 144740076usama ameenNoch keine Bewertungen

- Mauritius Tax Treaty Network - UpdateDokument1 SeiteMauritius Tax Treaty Network - UpdateNirvan MaudhooNoch keine Bewertungen

- Thrift Savings Plan TSP-1-C: Catch-Up Contribution ElectionDokument2 SeitenThrift Savings Plan TSP-1-C: Catch-Up Contribution ElectionIonut NeacsuNoch keine Bewertungen

- Private Foundations Tax GuideDokument48 SeitenPrivate Foundations Tax GuideKyu Chang HanNoch keine Bewertungen

- US Internal Revenue Service: f9325Dokument2 SeitenUS Internal Revenue Service: f9325IRSNoch keine Bewertungen

- Mediclaim 80D-1Dokument2 SeitenMediclaim 80D-1Jijo JosephNoch keine Bewertungen

- 7198 3Dokument1 Seite7198 3aravind029Noch keine Bewertungen

- Tax Management-Module 1 Problems On Residential Status and Incidence On TaxDokument2 SeitenTax Management-Module 1 Problems On Residential Status and Incidence On TaxdiviprabhuNoch keine Bewertungen

- D6659d767809b0879cc240hh60f16tdil725tad90h2: LR-RR NoDokument4 SeitenD6659d767809b0879cc240hh60f16tdil725tad90h2: LR-RR Noshaik matheenNoch keine Bewertungen

- Levy & Chrage of Tax - 221122 - 192035Dokument17 SeitenLevy & Chrage of Tax - 221122 - 192035Tushar MadanNoch keine Bewertungen

- Income Statement AssignmentDokument2 SeitenIncome Statement AssignmentJose SimmonsNoch keine Bewertungen

- It 2010043015691122654Dokument1 SeiteIt 2010043015691122654manzurhussainNoch keine Bewertungen

- Invoice BoatDokument1 SeiteInvoice Boatpjivan1208Noch keine Bewertungen

- Apollo Medicine InvoiceJan 20 2024 22 02Dokument1 SeiteApollo Medicine InvoiceJan 20 2024 22 02goodmorningviewersNoch keine Bewertungen

- Obillos V CIRDokument1 SeiteObillos V CIRAce Gregory AceronNoch keine Bewertungen

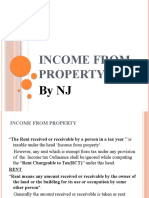

- Income From Property: by NJDokument8 SeitenIncome From Property: by NJUmar ZahidNoch keine Bewertungen