Das könnte Ihnen auch gefallen

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersVon EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNoch keine Bewertungen

- Construction Industry ReportDokument12 SeitenConstruction Industry Reportyahoooo1234Noch keine Bewertungen

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsVon EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNoch keine Bewertungen

- Toronto: OntarioDokument8 SeitenToronto: Ontarioapi-26443221Noch keine Bewertungen

- CHP Col ResearchDokument10 SeitenCHP Col ResearchJun GomezNoch keine Bewertungen

- The Red Dream: The Chinese Communist Party and the Financial Deterioration of ChinaVon EverandThe Red Dream: The Chinese Communist Party and the Financial Deterioration of ChinaNoch keine Bewertungen

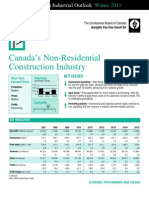

- Canada's Non-Residential Construction Industry: Key IssuesDokument10 SeitenCanada's Non-Residential Construction Industry: Key IssuesSteve LadurantayeNoch keine Bewertungen

- An Unconventional Introduction to Development Economics: A lively and user-friendly case studies method using hundreds of real-life macroeconomic scenarios from 52 countriesVon EverandAn Unconventional Introduction to Development Economics: A lively and user-friendly case studies method using hundreds of real-life macroeconomic scenarios from 52 countriesNoch keine Bewertungen

- Apartment Market Research Seattle 2010 3qDokument4 SeitenApartment Market Research Seattle 2010 3qDave EicherNoch keine Bewertungen

- Estimating the Job Creation Impact of Development AssistanceVon EverandEstimating the Job Creation Impact of Development AssistanceNoch keine Bewertungen

- CCRC Benchmarks and 2009 Medians-BB&T-Jan 2010Dokument8 SeitenCCRC Benchmarks and 2009 Medians-BB&T-Jan 2010api-26406608Noch keine Bewertungen

- 03.27.12 - Annual Report - Single Page Format With 10-K PDFDokument114 Seiten03.27.12 - Annual Report - Single Page Format With 10-K PDFm_edas4262Noch keine Bewertungen

- Franchise Business Economic Outlook: 2011: Prepared ForDokument18 SeitenFranchise Business Economic Outlook: 2011: Prepared Forapi-61836513Noch keine Bewertungen

- BCA - 2011 01 OutlookDokument3 SeitenBCA - 2011 01 OutlookJay Chan Wen JieNoch keine Bewertungen

- 3) Current Market InformationDokument6 Seiten3) Current Market Informationjwingo1Noch keine Bewertungen

- 22nd Japan Country-ReportDokument16 Seiten22nd Japan Country-ReportDavid MarlisNoch keine Bewertungen

- Real Estate Market Overview AD Jul 2010Dokument35 SeitenReal Estate Market Overview AD Jul 2010Mahesh ButaniNoch keine Bewertungen

- 3 - 7 and 3 - 8 - RJ - ISI - 2011 - Finav2lxDokument17 Seiten3 - 7 and 3 - 8 - RJ - ISI - 2011 - Finav2lxarnabkp14_799534911Noch keine Bewertungen

- Local Market Reports 2012 q4 ALMobileDokument7 SeitenLocal Market Reports 2012 q4 ALMobileFevi AbejeNoch keine Bewertungen

- Malloy2012 2013 Budget Power Point FinalDokument78 SeitenMalloy2012 2013 Budget Power Point FinalHelen BennettNoch keine Bewertungen

- CgreDokument5 SeitenCgreAnonymous Feglbx5Noch keine Bewertungen

- CAN Toronto Office Insight Q2 2018 JLL PDFDokument4 SeitenCAN Toronto Office Insight Q2 2018 JLL PDFMichaelNoch keine Bewertungen

- Upah Dan Produktivitas Untuk Pembangunan BerkelanjutanDokument6 SeitenUpah Dan Produktivitas Untuk Pembangunan Berkelanjutanmahdi cakepNoch keine Bewertungen

- Stock Pointer: Alok Industries LTDDokument20 SeitenStock Pointer: Alok Industries LTDGirish RaskarNoch keine Bewertungen

- October 2010Dokument4 SeitenOctober 2010Rachel E. Stassen-BergerNoch keine Bewertungen

- 2020 q4 Commercial Real Estate Metro Market Reports Az Tucson 03-02-2021Dokument1 Seite2020 q4 Commercial Real Estate Metro Market Reports Az Tucson 03-02-2021Joshua MoralesNoch keine Bewertungen

- FICCI Eco Survey 2011 12Dokument9 SeitenFICCI Eco Survey 2011 12Anirudh BhatjiwaleNoch keine Bewertungen

- OSA City of Jackson Analysis PDFDokument7 SeitenOSA City of Jackson Analysis PDFthe kingfishNoch keine Bewertungen

- Ccme Nhs Feb1stDokument7 SeitenCcme Nhs Feb1stgknyakoNoch keine Bewertungen

- Daiwa Capital MarketDokument6 SeitenDaiwa Capital MarketRongye Daniel LaiNoch keine Bewertungen

- Cbre Kyiv Office Market Report 2019 - Eng 1 PDFDokument8 SeitenCbre Kyiv Office Market Report 2019 - Eng 1 PDFBeta084Noch keine Bewertungen

- Ivrcl LTD: Business/Credit Profile - Akhil PawarDokument10 SeitenIvrcl LTD: Business/Credit Profile - Akhil PawarKintali VinodNoch keine Bewertungen

- Tell Us MoreDokument13 SeitenTell Us MoreFooNoch keine Bewertungen

- HR Budget PresentationDokument11 SeitenHR Budget PresentationMilanie NoriegaNoch keine Bewertungen

- EDD Press ReleaseDokument4 SeitenEDD Press ReleaseJustin BedecarreNoch keine Bewertungen

- IVRCL Infrastructure: Performance HighlightsDokument7 SeitenIVRCL Infrastructure: Performance Highlightsanudeep05Noch keine Bewertungen

- MRSD qtlmr124Dokument66 SeitenMRSD qtlmr124Ko NgeNoch keine Bewertungen

- NSWBC Sep2018 ReportDokument6 SeitenNSWBC Sep2018 ReportToby VueNoch keine Bewertungen

- 1Q21 Core Income Up 9.1% Y/y On Higher Data-Related Revenues, in Line With EstimatesDokument8 Seiten1Q21 Core Income Up 9.1% Y/y On Higher Data-Related Revenues, in Line With EstimatesJajahinaNoch keine Bewertungen

- State of Pakistan EconomyDokument8 SeitenState of Pakistan EconomyMuhammad KashifNoch keine Bewertungen

- KEP SC Feb11Dokument6 SeitenKEP SC Feb11waimun88Noch keine Bewertungen

- 2020 10 19 PH S Tel PDFDokument7 Seiten2020 10 19 PH S Tel PDFJNoch keine Bewertungen

- RDokument17 SeitenRSarmad Sadiq E4 42Noch keine Bewertungen

- Greenville Americas Alliance MarketBeat Industrial Q22017Dokument2 SeitenGreenville Americas Alliance MarketBeat Industrial Q22017Anonymous Feglbx5Noch keine Bewertungen

- Kuwait Investment Sector: Kuwait Financial Centre "Markaz"Dokument23 SeitenKuwait Investment Sector: Kuwait Financial Centre "Markaz"Jyoti PrakashNoch keine Bewertungen

- Simplex Infrastructures: Performance HighlightsDokument11 SeitenSimplex Infrastructures: Performance Highlightskrishna615Noch keine Bewertungen

- Kellogg's 2009 2010 Net Cash (Millions USD) Net Cash (Millions USD) Changes in Net Cash (Millions USD) Changes in Net Cash (Millions USD)Dokument4 SeitenKellogg's 2009 2010 Net Cash (Millions USD) Net Cash (Millions USD) Changes in Net Cash (Millions USD) Changes in Net Cash (Millions USD)NavinNoch keine Bewertungen

- Commercial Real Estate Outlook 2012 11Dokument8 SeitenCommercial Real Estate Outlook 2012 11National Association of REALTORS®Noch keine Bewertungen

- Uol Group Fy2020 Results 26 FEBRUARY 2021Dokument33 SeitenUol Group Fy2020 Results 26 FEBRUARY 2021Pat KwekNoch keine Bewertungen

- Employment Whitepaper 111007Dokument2 SeitenEmployment Whitepaper 111007Anonymous Feglbx5Noch keine Bewertungen

- Term Paper # 1: Eco519:Economics For ManagersDokument16 SeitenTerm Paper # 1: Eco519:Economics For ManagersckteamNoch keine Bewertungen

- April 2009 Economic UpdateDokument4 SeitenApril 2009 Economic UpdateMinnesota Public RadioNoch keine Bewertungen

- Metro Forecast Jan 2012Dokument5 SeitenMetro Forecast Jan 2012Anonymous Feglbx5Noch keine Bewertungen

- Chapter 5 Basics of Analysis Multiple CHDokument7 SeitenChapter 5 Basics of Analysis Multiple CHEslam AwadNoch keine Bewertungen

- Atloff 1Q11Dokument2 SeitenAtloff 1Q11Anonymous Feglbx5Noch keine Bewertungen

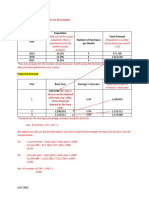

- Historical Demand Population Number of Purchases Per Month Total DemandDokument2 SeitenHistorical Demand Population Number of Purchases Per Month Total DemandDENXIONoch keine Bewertungen

- CDSL TP: 750: in Its Own LeagueDokument10 SeitenCDSL TP: 750: in Its Own LeagueSumangalNoch keine Bewertungen

- RecDokument28 SeitenRecChirag ShahNoch keine Bewertungen

- DP22 08Dokument42 SeitenDP22 08darksmancandaNoch keine Bewertungen

- ValeportDokument3 SeitenValeportAnonymous Feglbx5Noch keine Bewertungen

- Progress Ventures Newsletter 3Q2018Dokument18 SeitenProgress Ventures Newsletter 3Q2018Anonymous Feglbx5Noch keine Bewertungen

- Houston's Office Market Is Finally On The MendDokument9 SeitenHouston's Office Market Is Finally On The MendAnonymous Feglbx5Noch keine Bewertungen

- The Woodlands Office Submarket SnapshotDokument4 SeitenThe Woodlands Office Submarket SnapshotAnonymous Feglbx5Noch keine Bewertungen

- THRealEstate THINK-US Multifamily ResearchDokument10 SeitenTHRealEstate THINK-US Multifamily ResearchAnonymous Feglbx5Noch keine Bewertungen

- Houston's Industrial Market Continues To Expand, Adding 4.4M SF of Inventory in The Third QuarterDokument6 SeitenHouston's Industrial Market Continues To Expand, Adding 4.4M SF of Inventory in The Third QuarterAnonymous Feglbx5Noch keine Bewertungen

- Asl Marine Holdings LTDDokument28 SeitenAsl Marine Holdings LTDAnonymous Feglbx5Noch keine Bewertungen

- Hampton Roads Americas Alliance MarketBeat Retail Q32018Dokument2 SeitenHampton Roads Americas Alliance MarketBeat Retail Q32018Anonymous Feglbx5Noch keine Bewertungen

- Mack-Cali Realty Corporation Reports Third Quarter 2018 ResultsDokument9 SeitenMack-Cali Realty Corporation Reports Third Quarter 2018 ResultsAnonymous Feglbx5Noch keine Bewertungen

- Under Armour: Q3 Gains Come at Q4 Expense: Maintain SELLDokument7 SeitenUnder Armour: Q3 Gains Come at Q4 Expense: Maintain SELLAnonymous Feglbx5Noch keine Bewertungen

- Greenville Americas Alliance MarketBeat Office Q32018Dokument1 SeiteGreenville Americas Alliance MarketBeat Office Q32018Anonymous Feglbx5Noch keine Bewertungen

- Five Fast Facts - RIC Q3 2018Dokument1 SeiteFive Fast Facts - RIC Q3 2018Anonymous Feglbx5Noch keine Bewertungen

- Encyclopedia of Clinical Pharmacy by Joseph T. DiPiroDokument958 SeitenEncyclopedia of Clinical Pharmacy by Joseph T. DiPiroAlex Pieces100% (1)

- Gillenwater - Adult and Pediatric Urology 4th EdDokument1.564 SeitenGillenwater - Adult and Pediatric Urology 4th EdRoxana Boloaga100% (1)

- Bethesda: Downtown PlanDokument65 SeitenBethesda: Downtown PlanM-NCPPCNoch keine Bewertungen

- Notice: MeetingsDokument1 SeiteNotice: MeetingsJustia.comNoch keine Bewertungen

- Montgomery County PPP Loan RecipientsDokument29 SeitenMontgomery County PPP Loan RecipientsBethesda MagazineNoch keine Bewertungen

- Category Shopping Center Name: Neighborhood 1601 E. Gude DriveDokument72 SeitenCategory Shopping Center Name: Neighborhood 1601 E. Gude DriveM-NCPPCNoch keine Bewertungen

- WMAL Flyer CBREDokument3 SeitenWMAL Flyer CBREAJ MetcalfNoch keine Bewertungen

- Alex ResumeDokument2 SeitenAlex ResumeAlexandros XouriasNoch keine Bewertungen

- Chapter 19: Case Studies: Tall Buildings and Transit-Oriented Development in SuburbsDokument28 SeitenChapter 19: Case Studies: Tall Buildings and Transit-Oriented Development in SuburbsMara ANoch keine Bewertungen

- Floreen Pre-GeneralDokument76 SeitenFloreen Pre-GeneralDaniel SchereNoch keine Bewertungen

- Target Market AnalysisDokument3 SeitenTarget Market AnalysisJericho Fampulme FajilanNoch keine Bewertungen

- Pipeline of Approved Commercial Development: Montgomery County, MarylandDokument1 SeitePipeline of Approved Commercial Development: Montgomery County, MarylandM-NCPPCNoch keine Bewertungen

- Shopping Centers Included in InventoryDokument197 SeitenShopping Centers Included in InventoryM-NCPPCNoch keine Bewertungen

- Top Attorneys 2019Dokument14 SeitenTop Attorneys 2019Arlington MagazineNoch keine Bewertungen

- FINAL - AMS Community Letter - 8.23.17 LetterheadDokument2 SeitenFINAL - AMS Community Letter - 8.23.17 LetterheadAnonymous iJaTl5uLNoch keine Bewertungen

- Notice: MeetingsDokument1 SeiteNotice: MeetingsJustia.comNoch keine Bewertungen

- The Greater Bethesda-Chevy Chase Chamber of Commerce 2010-2011 Business Referral GuideDokument76 SeitenThe Greater Bethesda-Chevy Chase Chamber of Commerce 2010-2011 Business Referral GuideBCCChamberNoch keine Bewertungen

- May 16, 2011 New Boundary Study For BCC ClusterDokument3 SeitenMay 16, 2011 New Boundary Study For BCC ClusterParents' Coalition of Montgomery County, MarylandNoch keine Bewertungen

- Waiter Rant: Thanks for the Tip—Confessions of a Cynical WaiterVon EverandWaiter Rant: Thanks for the Tip—Confessions of a Cynical WaiterBewertung: 3.5 von 5 Sternen3.5/5 (487)

- Dealers of Lightning: Xerox PARC and the Dawn of the Computer AgeVon EverandDealers of Lightning: Xerox PARC and the Dawn of the Computer AgeBewertung: 4 von 5 Sternen4/5 (88)

- The United States of Beer: A Freewheeling History of the All-American DrinkVon EverandThe United States of Beer: A Freewheeling History of the All-American DrinkBewertung: 4 von 5 Sternen4/5 (7)

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumVon EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumBewertung: 3 von 5 Sternen3/5 (12)

- All The Beauty in the World: The Metropolitan Museum of Art and MeVon EverandAll The Beauty in the World: The Metropolitan Museum of Art and MeBewertung: 4.5 von 5 Sternen4.5/5 (83)

- System Error: Where Big Tech Went Wrong and How We Can RebootVon EverandSystem Error: Where Big Tech Went Wrong and How We Can RebootNoch keine Bewertungen

- The Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyVon EverandThe Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyNoch keine Bewertungen

- AI Superpowers: China, Silicon Valley, and the New World OrderVon EverandAI Superpowers: China, Silicon Valley, and the New World OrderBewertung: 4.5 von 5 Sternen4.5/5 (398)

- Summary: Unreasonable Hospitality: The Remarkable Power of Giving People More than They Expect by Will Guidara: Key Takeaways, Summary & Analysis IncludedVon EverandSummary: Unreasonable Hospitality: The Remarkable Power of Giving People More than They Expect by Will Guidara: Key Takeaways, Summary & Analysis IncludedBewertung: 2.5 von 5 Sternen2.5/5 (5)

- Pit Bull: Lessons from Wall Street's Champion TraderVon EverandPit Bull: Lessons from Wall Street's Champion TraderBewertung: 4 von 5 Sternen4/5 (17)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomVon EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomNoch keine Bewertungen

- The Kingdom of Prep: The Inside Story of the Rise and (Near) Fall of J.CrewVon EverandThe Kingdom of Prep: The Inside Story of the Rise and (Near) Fall of J.CrewBewertung: 4.5 von 5 Sternen4.5/5 (26)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesVon EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesBewertung: 4.5 von 5 Sternen4.5/5 (8)

- Getting Started in Consulting: The Unbeatable Comprehensive Guidebook for First-Time ConsultantsVon EverandGetting Started in Consulting: The Unbeatable Comprehensive Guidebook for First-Time ConsultantsBewertung: 4.5 von 5 Sternen4.5/5 (10)

- All You Need to Know About the Music Business: Eleventh EditionVon EverandAll You Need to Know About the Music Business: Eleventh EditionNoch keine Bewertungen

- INSPIRED: How to Create Tech Products Customers LoveVon EverandINSPIRED: How to Create Tech Products Customers LoveBewertung: 5 von 5 Sternen5/5 (9)

- The Formula: How Rogues, Geniuses, and Speed Freaks Reengineered F1 into the World's Fastest Growing SportVon EverandThe Formula: How Rogues, Geniuses, and Speed Freaks Reengineered F1 into the World's Fastest Growing SportNoch keine Bewertungen

- Data-ism: The Revolution Transforming Decision Making, Consumer Behavior, and Almost Everything ElseVon EverandData-ism: The Revolution Transforming Decision Making, Consumer Behavior, and Almost Everything ElseBewertung: 3.5 von 5 Sternen3.5/5 (12)

- An Ugly Truth: Inside Facebook's Battle for DominationVon EverandAn Ugly Truth: Inside Facebook's Battle for DominationBewertung: 4 von 5 Sternen4/5 (33)

- The Toyota Way (Second Edition): 14 Management Principles from the World's Greatest ManufacturerVon EverandThe Toyota Way (Second Edition): 14 Management Principles from the World's Greatest ManufacturerBewertung: 4 von 5 Sternen4/5 (121)

- All You Need to Know About the Music Business: 11th EditionVon EverandAll You Need to Know About the Music Business: 11th EditionNoch keine Bewertungen