Das könnte Ihnen auch gefallen

- Valued Added TaxDokument5 SeitenValued Added TaxCharles Reginald K. Hwang100% (6)

- Accounting For Materials 1Dokument24 SeitenAccounting For Materials 1Charles Reginald K. HwangNoch keine Bewertungen

- Sample Changes Shareholder's EquityDokument1 SeiteSample Changes Shareholder's EquityCharles Reginald K. HwangNoch keine Bewertungen

- ACCCOB3 Syllbus Online 2021T1 1Dokument12 SeitenACCCOB3 Syllbus Online 2021T1 1Charles Reginald K. HwangNoch keine Bewertungen

- Value Added TaxDokument4 SeitenValue Added TaxCharles Reginald K. Hwang100% (4)

- Accounting For Labor 3Dokument13 SeitenAccounting For Labor 3Charles Reginald K. HwangNoch keine Bewertungen

- Introduction To CorporationDokument5 SeitenIntroduction To CorporationCharles Reginald K. Hwang0% (1)

- PostingDokument2 SeitenPostingCharles Reginald K. HwangNoch keine Bewertungen

- Trial BalanceDokument2 SeitenTrial BalanceCharles Reginald K. HwangNoch keine Bewertungen

- Par Value Shares and Delinquent SharesDokument3 SeitenPar Value Shares and Delinquent SharesCharles Reginald K. Hwang100% (3)

- Post Closing TB and ReversingDokument1 SeitePost Closing TB and ReversingCharles Reginald K. HwangNoch keine Bewertungen

- Actbas 2 Downloaded Lecture Notes 2Dokument7 SeitenActbas 2 Downloaded Lecture Notes 2Charles Reginald K. HwangNoch keine Bewertungen

- Statement of Cash FlowsDokument1 SeiteStatement of Cash FlowsCharles Reginald K. HwangNoch keine Bewertungen

- LiquidationDokument2 SeitenLiquidationCharles Reginald K. HwangNoch keine Bewertungen

- Closing EntriesDokument1 SeiteClosing EntriesCharles Reginald K. HwangNoch keine Bewertungen

- Corporation CodeDokument35 SeitenCorporation CodeCharles Reginald K. HwangNoch keine Bewertungen

- DepreciationDokument2 SeitenDepreciationCharles Reginald K. HwangNoch keine Bewertungen

- Shareholders' EquityDokument1 SeiteShareholders' EquityCharles Reginald K. HwangNoch keine Bewertungen

- The WorksheetDokument1 SeiteThe WorksheetCharles Reginald K. HwangNoch keine Bewertungen

- Accounting For Retained EarningsDokument1 SeiteAccounting For Retained EarningsCharles Reginald K. HwangNoch keine Bewertungen

- Actpaco Download Lecture NotesDokument59 SeitenActpaco Download Lecture NotesCharles Reginald K. Hwang100% (1)

- Accounting For Treasury SharesDokument2 SeitenAccounting For Treasury SharesCharles Reginald K. Hwang100% (1)

- Doubtful AccountsDokument2 SeitenDoubtful AccountsCharles Reginald K. HwangNoch keine Bewertungen

- Actbas 2 Downloaded Lecture Notes 2Dokument7 SeitenActbas 2 Downloaded Lecture Notes 2Charles Reginald K. HwangNoch keine Bewertungen

- Open-Economy Macroeconomics: The Balance of Payments and Exchange RatesDokument26 SeitenOpen-Economy Macroeconomics: The Balance of Payments and Exchange RatesCharles Reginald K. HwangNoch keine Bewertungen

- The Labor Market, Unemployment, and Inflation: Fernando & Yvonn QuijanoDokument31 SeitenThe Labor Market, Unemployment, and Inflation: Fernando & Yvonn QuijanoCharles Reginald K. HwangNoch keine Bewertungen

- Aggregate Demand, Aggregate Supply, and Inflation: Fernando & Yvonn QuijanoDokument23 SeitenAggregate Demand, Aggregate Supply, and Inflation: Fernando & Yvonn QuijanoCharles Reginald K. HwangNoch keine Bewertungen

- Case Econ08 PPT 21Dokument38 SeitenCase Econ08 PPT 21Ronnie DeanNoch keine Bewertungen

- Money, The Interest Rate, and Output: Analysis and Policy: Part Vi Macroeconomic AnalysisDokument27 SeitenMoney, The Interest Rate, and Output: Analysis and Policy: Part Vi Macroeconomic AnalysisCharles Reginald K. HwangNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Blackbook (80 PG) FinalDokument82 SeitenBlackbook (80 PG) Finalaadil shaikhNoch keine Bewertungen

- Kavisha Dissertation Retail BankingDokument68 SeitenKavisha Dissertation Retail BankingMohit AgarwalNoch keine Bewertungen

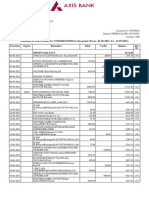

- Statement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Dokument6 SeitenStatement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Anirban DebNoch keine Bewertungen

- Ewallet Terms of Use: 1. SubjectDokument14 SeitenEwallet Terms of Use: 1. SubjectJohanna castroNoch keine Bewertungen

- Account Opening FormDokument23 SeitenAccount Opening Formabhishek shawNoch keine Bewertungen

- ABA Mobile Terms and Condition en V2.1Dokument20 SeitenABA Mobile Terms and Condition en V2.1suos.vuthy26Noch keine Bewertungen

- Daily Revenue ReportDokument3 SeitenDaily Revenue ReportRoftadiaWgNoch keine Bewertungen

- Deposit Account RulesDokument33 SeitenDeposit Account RulesELIZABETH JOHNSONNoch keine Bewertungen

- Full Survey Report On Online ShoppingDokument33 SeitenFull Survey Report On Online ShoppingAbhishek Mani PathakNoch keine Bewertungen

- UPI-PG-17 - 01 - 31 - RBI - Final Version 1.7 PDFDokument89 SeitenUPI-PG-17 - 01 - 31 - RBI - Final Version 1.7 PDFVegeta100% (1)

- DebiCheck DecodedDokument61 SeitenDebiCheck DecodedJanido MohlalaNoch keine Bewertungen

- Amazon Easystore & Neo BankingDokument32 SeitenAmazon Easystore & Neo BankingAlgo TraderNoch keine Bewertungen

- VIA TravelDokument12 SeitenVIA TravelLoraine RingonNoch keine Bewertungen

- Https WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action DoprintDokument1 SeiteHttps WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action DoprintSyed HanafieNoch keine Bewertungen

- Ravi Kumar - Assistant Manager - Fraud RiskDokument3 SeitenRavi Kumar - Assistant Manager - Fraud RiskDaminiNoch keine Bewertungen

- Statement1679393377960 PDFDokument5 SeitenStatement1679393377960 PDFAaditya Vignyan VellalaNoch keine Bewertungen

- Bharti Airtel LTD.: Your Account Summary This Month'S ChargesDokument4 SeitenBharti Airtel LTD.: Your Account Summary This Month'S ChargesMadhukar Reddy KukunoorNoch keine Bewertungen

- Format PT Galaxy Elektronik 2Dokument53 SeitenFormat PT Galaxy Elektronik 2sabrina damayantiNoch keine Bewertungen

- User Manual Class4Dokument16 SeitenUser Manual Class4Kamlesh SinghNoch keine Bewertungen

- 2012 Spring Turkey, Javelina, Buffalo and Bear: Hunt Draw InformationDokument32 Seiten2012 Spring Turkey, Javelina, Buffalo and Bear: Hunt Draw InformationRoeHuntingResourcesNoch keine Bewertungen

- Most Important Terms & Conditions: Schedule of ChargesDokument11 SeitenMost Important Terms & Conditions: Schedule of ChargesRaghavan VenkatramanNoch keine Bewertungen

- PAC Registration Guide For Fiji and TongaDokument18 SeitenPAC Registration Guide For Fiji and TongaKameli MNoch keine Bewertungen

- 2013-2014 Kumari Bank Annual ReportDokument100 Seiten2013-2014 Kumari Bank Annual Reportdevi ghimireNoch keine Bewertungen

- Final Internship Report On Summit Bank by Ibrar A. QaziDokument50 SeitenFinal Internship Report On Summit Bank by Ibrar A. QaziAbrar Ahmed Qazi82% (11)

- Project On Online BankingDokument78 SeitenProject On Online BankingNamita Sawant88% (8)

- GK Tornado Ibps RRB Main Exam 2019 English 43 PDFDokument150 SeitenGK Tornado Ibps RRB Main Exam 2019 English 43 PDFSankar SreeramdasNoch keine Bewertungen

- Coway-Sales-Order-Form - 2020-05-01 02-38-02 - ROFAIZAL-BIN-RAHMAT PDFDokument2 SeitenCoway-Sales-Order-Form - 2020-05-01 02-38-02 - ROFAIZAL-BIN-RAHMAT PDFNoor Shahirah Ayub100% (1)

- Receiving Bank Reference EbsDokument13 SeitenReceiving Bank Reference EbsPAVAN TAVVANoch keine Bewertungen

- One India One PlanDokument3 SeitenOne India One PlanViral100% (1)

- Ecom 3Dokument10 SeitenEcom 3Rachit SrivastavaNoch keine Bewertungen