Das könnte Ihnen auch gefallen

- Types of Al-Ijarah Contracts ExplainedDokument6 SeitenTypes of Al-Ijarah Contracts ExplainedMastura AmitNoch keine Bewertungen

- Meezan Bank ReportDokument19 SeitenMeezan Bank ReportkashifislamicNoch keine Bewertungen

- Ijarah Fund: This Way May Be Justified On The Analogy of Simsâr (Broker) For Whom The Fee Based On Percentage Is AllowedDokument9 SeitenIjarah Fund: This Way May Be Justified On The Analogy of Simsâr (Broker) For Whom The Fee Based On Percentage Is AllowedumairNoch keine Bewertungen

- Unit FourDokument28 SeitenUnit FourTesfaye Megiso BegajoNoch keine Bewertungen

- Leasing and Hire PurchaseDokument4 SeitenLeasing and Hire PurchaseAsad KhanNoch keine Bewertungen

- Ijarah LeasingDokument3 SeitenIjarah LeasingHuda Reem MansharamaniNoch keine Bewertungen

- Ijarah: Basic Rules of Ijarah/LeasingDokument6 SeitenIjarah: Basic Rules of Ijarah/Leasingali_zain_7Noch keine Bewertungen

- LeasingDokument7 SeitenLeasingavishkar kaleNoch keine Bewertungen

- A SalamDokument3 SeitenA Salamali_zain_7Noch keine Bewertungen

- Al Ijarah Essentials GuideDokument15 SeitenAl Ijarah Essentials Guidekamranp1Noch keine Bewertungen

- Islamic Modes of Financing: Ijarah (I)Dokument38 SeitenIslamic Modes of Financing: Ijarah (I)atiqa tanveerNoch keine Bewertungen

- IjamanDokument20 SeitenIjamanIqbal Hussain DadiNoch keine Bewertungen

- Lease FinancingDokument36 SeitenLease Financingssahni15Noch keine Bewertungen

- Introduction To Ijarah: Release DateDokument21 SeitenIntroduction To Ijarah: Release Datewafa shumailNoch keine Bewertungen

- Group2 Lease FinancingDokument24 SeitenGroup2 Lease FinancingMohit Motwani100% (1)

- Ijara-Based Financing: Definition of Ijara (Leasing)Dokument13 SeitenIjara-Based Financing: Definition of Ijara (Leasing)Nura HaikuNoch keine Bewertungen

- Sale Leaseback & MortgageDokument30 SeitenSale Leaseback & MortgageshivpreetsandhuNoch keine Bewertungen

- Leasing (Ijara) FacilityDokument24 SeitenLeasing (Ijara) FacilityAbdiel BanjaryNoch keine Bewertungen

- IjarahDokument26 SeitenIjarahMohsen SirajNoch keine Bewertungen

- ACCOUNTING FOR ISLAMIC BANKS: KEY ISSUES IN IJARAH FINANCINGDokument50 SeitenACCOUNTING FOR ISLAMIC BANKS: KEY ISSUES IN IJARAH FINANCINGDeliaFitrianaHidayatNoch keine Bewertungen

- Lesson 4Dokument10 SeitenLesson 4Absalom OtienoNoch keine Bewertungen

- Lease FinancingDokument17 SeitenLease FinancingSonile JereNoch keine Bewertungen

- IjaraDokument26 SeitenIjaraNehal BadawyNoch keine Bewertungen

- Basic Concepts of Islamic FinanceDokument5 SeitenBasic Concepts of Islamic FinanceSaifullahMakenNoch keine Bewertungen

- YuvikaDokument8 SeitenYuvikaYuvika DhimanNoch keine Bewertungen

- Ibf Case StudyDokument17 SeitenIbf Case StudyAyesha HamidNoch keine Bewertungen

- Ijara: 1.1 Scope of The StandardDokument19 SeitenIjara: 1.1 Scope of The StandardAsghar KhanNoch keine Bewertungen

- Basic Rules Governing Leasing Under Islamic LawDokument4 SeitenBasic Rules Governing Leasing Under Islamic LawmobinnaimNoch keine Bewertungen

- Term Paper # 1. Definition and Meaning of Lease FinancingDokument16 SeitenTerm Paper # 1. Definition and Meaning of Lease FinancingAniket PuriNoch keine Bewertungen

- Lease TheoryDokument10 SeitenLease TheorySyeda AtikNoch keine Bewertungen

- Non Banking Financial Institutions: by Sudev Jyothisi FN-92 Scms-CochinDokument18 SeitenNon Banking Financial Institutions: by Sudev Jyothisi FN-92 Scms-CochinSUDEVJYOTHISINoch keine Bewertungen

- Definition of IjarahDokument4 SeitenDefinition of Ijarahmings bbyNoch keine Bewertungen

- Comparison Between Ijara and Conventional LeasingDokument31 SeitenComparison Between Ijara and Conventional Leasingumar0% (1)

- TYPES OF LEASES UNDER IAS 17Dokument11 SeitenTYPES OF LEASES UNDER IAS 17Kurrent Toy100% (1)

- ILOs on Lease AccountingDokument12 SeitenILOs on Lease AccountingMon RamNoch keine Bewertungen

- 14 Different Types of Lease You Need To KnowDokument3 Seiten14 Different Types of Lease You Need To KnowLaylaNoch keine Bewertungen

- Leasing: Definitions, Types, Merits and Demerits: AdvertisementsDokument5 SeitenLeasing: Definitions, Types, Merits and Demerits: AdvertisementsShivani GogiaNoch keine Bewertungen

- The Saint Augustine University of Tanzania: QuestionsDokument7 SeitenThe Saint Augustine University of Tanzania: QuestionsIssa AdiemaNoch keine Bewertungen

- 1 - IjarahDokument31 Seiten1 - IjarahAlishba KaiserNoch keine Bewertungen

- Islamic Law ProjectDokument8 SeitenIslamic Law ProjectSami UllahNoch keine Bewertungen

- 1 Year MBADokument28 Seiten1 Year MBABijoy BijoyNoch keine Bewertungen

- Accounting For LeasesDokument14 SeitenAccounting For LeasesBringi KenyiNoch keine Bewertungen

- IjarahDokument29 SeitenIjarahiqraNoch keine Bewertungen

- Unit Iv Fund Based Financial Services: Basic Concepts in LeasingDokument13 SeitenUnit Iv Fund Based Financial Services: Basic Concepts in LeasingJessica TerryNoch keine Bewertungen

- Ijaraha ShortDokument6 SeitenIjaraha ShortMuhammad HasnainNoch keine Bewertungen

- Securitization and Hire Purchase ExplainedDokument19 SeitenSecuritization and Hire Purchase Explainedsumit_mehta12Noch keine Bewertungen

- Ijarah MechanismDokument5 SeitenIjarah MechanismRezaul Alam100% (1)

- Lease Financing: Presentation By: Mohammed Akbar KhanDokument30 SeitenLease Financing: Presentation By: Mohammed Akbar KhanMohammed Akbar KhanNoch keine Bewertungen

- Fund Based Financial Services GuideDokument16 SeitenFund Based Financial Services GuidePriyanka PanigrahiNoch keine Bewertungen

- Types of Finance LeasingDokument6 SeitenTypes of Finance LeasingRishi kaurNoch keine Bewertungen

- Ijarah RGBDokument23 SeitenIjarah RGBAsad AliNoch keine Bewertungen

- Transfer of Property & Registration ActDokument23 SeitenTransfer of Property & Registration Actsiddiquishoaib1Noch keine Bewertungen

- Understand Leasing Concepts and TypesDokument48 SeitenUnderstand Leasing Concepts and TypesPreeti Sharma100% (1)

- CH Hamad Rasool BhullarDokument12 SeitenCH Hamad Rasool BhullarAlHuda Centre of Islamic Banking & Economics (CIBE)Noch keine Bewertungen

- Theoretical and Regulatory Framework of Leasing: Management of Financial Services - MY KhanDokument28 SeitenTheoretical and Regulatory Framework of Leasing: Management of Financial Services - MY KhanSuraj Rajpurohit50% (2)

- Leasing, Hire Purchase & Consumer Credit: Unit-2Dokument60 SeitenLeasing, Hire Purchase & Consumer Credit: Unit-2Feeroj PathanNoch keine Bewertungen

- New LeasingDokument56 SeitenNew LeasingChirag Goyal100% (1)

- Securitized Real Estate and 1031 ExchangesVon EverandSecuritized Real Estate and 1031 ExchangesNoch keine Bewertungen

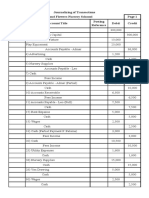

- Journalizing Transaction (Ezekiel Lapitan)Dokument3 SeitenJournalizing Transaction (Ezekiel Lapitan)Ezekiel LapitanNoch keine Bewertungen

- Fim01 - 02 - Basic FsDokument8 SeitenFim01 - 02 - Basic FsJomar VillenaNoch keine Bewertungen

- Metro-Score PPI: Customer Credit ReportDokument5 SeitenMetro-Score PPI: Customer Credit ReportPastor Roy Onyancha CyberNoch keine Bewertungen

- Bond Pricing CalculatorDokument37 SeitenBond Pricing CalculatorFurqan Farooq Vadharia100% (1)

- MOCK UP SOAL UAS AKL II Dan ADV II 2018Dokument5 SeitenMOCK UP SOAL UAS AKL II Dan ADV II 2018Nathalie Christnindita DecidNoch keine Bewertungen

- Module 2a - AR RecapDokument10 SeitenModule 2a - AR RecapChen HaoNoch keine Bewertungen

- FM16 Ch26 Tool KitDokument21 SeitenFM16 Ch26 Tool KitAdamNoch keine Bewertungen

- CTTT - C5 (Eng)Dokument18 SeitenCTTT - C5 (Eng)Tram AnhhNoch keine Bewertungen

- Loan Application Form and DocumentsDokument2 SeitenLoan Application Form and DocumentsSoowhysoo Twoonel100% (2)

- Feb 23 To Jan 24Dokument40 SeitenFeb 23 To Jan 24Next Media UKNoch keine Bewertungen

- Section "A" Very Short Answer Questions) (Attempt All Questions)Dokument5 SeitenSection "A" Very Short Answer Questions) (Attempt All Questions)Ayusha TimalsinaNoch keine Bewertungen

- Forex Trading Machine EbookDokument0 SeitenForex Trading Machine EbookMahadi MahmodNoch keine Bewertungen

- CXC Past Questions and Answers - Principles of Business: (2mks) (4mks) (4mks) Total 10 MarksDokument34 SeitenCXC Past Questions and Answers - Principles of Business: (2mks) (4mks) (4mks) Total 10 MarksTushti RamloganNoch keine Bewertungen

- Sign Verified Tax Invoice for GPON Fiber HD5 HYD 50Mbps Monthly SubscriptionDokument1 SeiteSign Verified Tax Invoice for GPON Fiber HD5 HYD 50Mbps Monthly SubscriptionShetkar GouthamNoch keine Bewertungen

- Shweta TybbiDokument72 SeitenShweta Tybbishwetalad887% (30)

- Assignment June 2022Dokument3 SeitenAssignment June 2022AirForce ManNoch keine Bewertungen

- Banking Regulations SummaryDokument20 SeitenBanking Regulations SummaryGraceson Binu Sebastian100% (1)

- Wedding Photography and Videography QuotationDokument1 SeiteWedding Photography and Videography Quotationbhagyashree satamNoch keine Bewertungen

- EJMCM Volume 7 Issue 4 Pages 999-1009Dokument11 SeitenEJMCM Volume 7 Issue 4 Pages 999-1009Reem Alaa AldinNoch keine Bewertungen

- Q CH 9Dokument7 SeitenQ CH 9Jhon F SinagaNoch keine Bewertungen

- Audit of Cash and Financial InstrumentsDokument4 SeitenAudit of Cash and Financial Instrumentsmrs leeNoch keine Bewertungen

- Executive SummaryDokument2 SeitenExecutive Summarycsaswin2010Noch keine Bewertungen

- PrabhDokument3 SeitenPrabhrajNoch keine Bewertungen

- Wildcat Capital InvestorsDokument18 SeitenWildcat Capital Investorsokta hutahaeanNoch keine Bewertungen

- Exercise: The Market For Foreign Exchange: BMFM 33135 Oct 2020Dokument3 SeitenExercise: The Market For Foreign Exchange: BMFM 33135 Oct 2020Sylvia GynNoch keine Bewertungen

- Investment - Audit Program - HandoutsDokument2 SeitenInvestment - Audit Program - HandoutsRoquessa Michel R. IgnaligNoch keine Bewertungen

- Quizzes - Topic 6 - Leases - Xem L I Bài LàmDokument4 SeitenQuizzes - Topic 6 - Leases - Xem L I Bài LàmHải YếnNoch keine Bewertungen

- MAEC - Project Report - Group PDokument21 SeitenMAEC - Project Report - Group PSudip KarNoch keine Bewertungen

- Cebu International Finance Corporation V CA AlegreDokument4 SeitenCebu International Finance Corporation V CA AlegreJANE MARIE DOROMALNoch keine Bewertungen

- Suggested Solutions To Assignment 2 (OPTIONAL)Dokument10 SeitenSuggested Solutions To Assignment 2 (OPTIONAL)famin87Noch keine Bewertungen