Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Ind As 2 PDFDokument26 SeitenInd As 2 PDFmanan3466Noch keine Bewertungen

- Ndokwa Salale Resume - AccountantDokument5 SeitenNdokwa Salale Resume - AccountantNdokwaNoch keine Bewertungen

- Doing Business in RPDokument80 SeitenDoing Business in RPRichard BalaisNoch keine Bewertungen

- R12 ReportsDokument176 SeitenR12 ReportsStacey BrooksNoch keine Bewertungen

- Chapter 1 - Page 18Dokument3 SeitenChapter 1 - Page 18Ri Fi100% (1)

- IFRS 9 - Financial InstrumentsDokument14 SeitenIFRS 9 - Financial InstrumentsJayvie Dizon Salvador0% (1)

- Accounts - Module 6 Provisions of The Companies Act 1956Dokument15 SeitenAccounts - Module 6 Provisions of The Companies Act 19569986212378Noch keine Bewertungen

- ABE Plumbing FlowchartDokument1 SeiteABE Plumbing FlowchartRainbow VillanuevaNoch keine Bewertungen

- Chapter 5 SolutionsDokument13 SeitenChapter 5 SolutionsjessicaNoch keine Bewertungen

- Accounting - Questions 010812Dokument4 SeitenAccounting - Questions 010812jhouvanNoch keine Bewertungen

- Arens - Chapter14 AuditingDokument39 SeitenArens - Chapter14 AuditingtableroofNoch keine Bewertungen

- Arun LamsalDokument50 SeitenArun LamsalSmith TiwariNoch keine Bewertungen

- ABC Company Balance Sheet For The Period Ended in PesoDokument41 SeitenABC Company Balance Sheet For The Period Ended in Pesojosh lunarNoch keine Bewertungen

- Case Study Solution 20% - ImpairmentDokument4 SeitenCase Study Solution 20% - ImpairmentSeiniNoch keine Bewertungen

- SDDokument19 SeitenSDNitinNoch keine Bewertungen

- Analisis Penerapan PSAK No.16 Dalam Perlakuan Akuntansi Aset Tetap PerusahaanDokument10 SeitenAnalisis Penerapan PSAK No.16 Dalam Perlakuan Akuntansi Aset Tetap PerusahaanNurlaili RomadhaniNoch keine Bewertungen

- Auditing Theory - Audit ReportDokument26 SeitenAuditing Theory - Audit ReportCarina Espallardo-RelucioNoch keine Bewertungen

- Financial Analysis ProjectDokument11 SeitenFinancial Analysis ProjectCharles TulipNoch keine Bewertungen

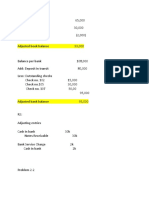

- Bank ReconciliationDokument6 SeitenBank Reconciliationclarisse jaramillaNoch keine Bewertungen

- Block 1 MS 035 Unit 1Dokument19 SeitenBlock 1 MS 035 Unit 1akshayvermaNoch keine Bewertungen

- Transformation in Revenue AccountingDokument92 SeitenTransformation in Revenue AccountingTestspotyfireal EsyNoch keine Bewertungen

- 4 Completing The Accounting Cycle PartDokument1 Seite4 Completing The Accounting Cycle PartTalionNoch keine Bewertungen

- Chap 12Dokument44 SeitenChap 12Jehad Selawe100% (1)

- Course Structure - BfiaDokument2 SeitenCourse Structure - BfiaAmity-elearningNoch keine Bewertungen

- Kế Toán Quốc Tế: Select oneDokument8 SeitenKế Toán Quốc Tế: Select oneLoki Luke100% (1)

- Accounting For Local GovernmentDokument6 SeitenAccounting For Local GovernmentEsther AkpanNoch keine Bewertungen

- ch04 SM RankinDokument23 Seitench04 SM RankinSTU DOC100% (2)

- Accounting-Financial Statements of Companies-1653399167327513Dokument37 SeitenAccounting-Financial Statements of Companies-1653399167327513Badhrinath ShanmugamNoch keine Bewertungen

- Zychol Chemicel Corporation Case StudyDokument3 SeitenZychol Chemicel Corporation Case StudyShawon Corleone33% (3)

- Management Acct AssignmentDokument11 SeitenManagement Acct AssignmentYasir ArafatNoch keine Bewertungen