Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- HBS Case Report Analysis of Newbridge's Investment in Shenzhen Development BankDokument11 SeitenHBS Case Report Analysis of Newbridge's Investment in Shenzhen Development BankAmandaTranNoch keine Bewertungen

- Agenda 11 6Dokument4 SeitenAgenda 11 6Luwei ShenNoch keine Bewertungen

- Standardized Approach For Counterparty Credit RiskDokument2 SeitenStandardized Approach For Counterparty Credit RiskjalutukNoch keine Bewertungen

- Cpa Review School - Prac 1Dokument12 SeitenCpa Review School - Prac 1jikee1150% (2)

- A Study On Financial Statement Analysis in Mokshwa Soft Drinks at CoimbatoreDokument23 SeitenA Study On Financial Statement Analysis in Mokshwa Soft Drinks at Coimbatorek eswariNoch keine Bewertungen

- Global Hedge Fund Conference Agenda NewDokument1 SeiteGlobal Hedge Fund Conference Agenda NewLuwei ShenNoch keine Bewertungen

- Alphaex Capital Candlestick Pattern Cheat Sheet InfographDokument1 SeiteAlphaex Capital Candlestick Pattern Cheat Sheet InfographFnudarman Fnudarman100% (1)

- Trading Volatility Ny 2016Dokument84 SeitenTrading Volatility Ny 2016sebab1Noch keine Bewertungen

- Premier Hedge Fund Conference Agenda 2017 PDFDokument4 SeitenPremier Hedge Fund Conference Agenda 2017 PDFLuwei ShenNoch keine Bewertungen

- Premier Hedge Fund Conference Agenda 2017 PDFDokument4 SeitenPremier Hedge Fund Conference Agenda 2017 PDFLuwei ShenNoch keine Bewertungen

- Dell Working CapitalDokument3 SeitenDell Working CapitalShashank Agarwal89% (9)

- Simply Trading Forex. A Free Guide On How To Trade The Forex Market. Kevin Greenhall PDFDokument55 SeitenSimply Trading Forex. A Free Guide On How To Trade The Forex Market. Kevin Greenhall PDFpaoloNoch keine Bewertungen

- Introduction - About Fast-Track Cities Initiative (Ftci) and The Hiv Asset & Gap Analysis (Aga)Dokument30 SeitenIntroduction - About Fast-Track Cities Initiative (Ftci) and The Hiv Asset & Gap Analysis (Aga)Luwei ShenNoch keine Bewertungen

- GHB GBL Chem Sex - Pepse v2Dokument11 SeitenGHB GBL Chem Sex - Pepse v2Luwei ShenNoch keine Bewertungen

- Page 2: Introduction To Your AgencyDokument6 SeitenPage 2: Introduction To Your AgencyLuwei ShenNoch keine Bewertungen

- Page 2: Introduction To Your AgencyDokument10 SeitenPage 2: Introduction To Your AgencyLuwei ShenNoch keine Bewertungen

- Kellogg RecruitmentReport 2016 CmcwebDokument28 SeitenKellogg RecruitmentReport 2016 CmcwebLuwei ShenNoch keine Bewertungen

- Agenda 10 31Dokument1 SeiteAgenda 10 31Luwei ShenNoch keine Bewertungen

- Wharton Resume TemplateDokument1 SeiteWharton Resume TemplateLuwei ShenNoch keine Bewertungen

- Mergers and Acquisitions in Indian Banking SectorDokument48 SeitenMergers and Acquisitions in Indian Banking SectorJai GaneshNoch keine Bewertungen

- GITAM Hyderabad Business School UG/PG III Semester End Semester Examination January 2022 B.Com (ACCA) MBC205 (Advance ExcelDokument3 SeitenGITAM Hyderabad Business School UG/PG III Semester End Semester Examination January 2022 B.Com (ACCA) MBC205 (Advance ExcelSharan MouryaNoch keine Bewertungen

- Chapter 6 - Capital BudgetingDokument12 SeitenChapter 6 - Capital BudgetingParth GargNoch keine Bewertungen

- Week Seven - Translation of Foreign Currency Financial StatementsDokument28 SeitenWeek Seven - Translation of Foreign Currency Financial StatementsCoffee JellyNoch keine Bewertungen

- ABC L3 Past Paper Series 3 2013Dokument7 SeitenABC L3 Past Paper Series 3 2013b3nzyNoch keine Bewertungen

- Port-Folio Management: Module Code: MBA 721Dokument31 SeitenPort-Folio Management: Module Code: MBA 721RabiaChaudhryNoch keine Bewertungen

- Emkay LEAD PMS - JULY 2019Dokument17 SeitenEmkay LEAD PMS - JULY 2019speedenquiryNoch keine Bewertungen

- Daily Report 01 10 4Dokument87 SeitenDaily Report 01 10 4Gihan PereraNoch keine Bewertungen

- Native Bush Spices Australia Strategic PlanDokument10 SeitenNative Bush Spices Australia Strategic PlanPersatuan Ekonomi Usahawan BumiputeraNoch keine Bewertungen

- 15-Mca-Or-Accounting and Financial ManagementDokument4 Seiten15-Mca-Or-Accounting and Financial ManagementSRINIVASA RAO GANTANoch keine Bewertungen

- Management Accounting Level 3: LCCI International QualificationsDokument14 SeitenManagement Accounting Level 3: LCCI International QualificationsHein Linn Kyaw50% (2)

- AmazonDokument4 SeitenAmazonbonnieNoch keine Bewertungen

- Antiquee ReportDokument51 SeitenAntiquee ReportanushkakiranNoch keine Bewertungen

- Full Download Advanced Accounting 13th Edition Beams Solutions ManualDokument36 SeitenFull Download Advanced Accounting 13th Edition Beams Solutions Manualjacksongubmor100% (34)

- AC4301 FinalExam 2020-21 SemA AnsDokument9 SeitenAC4301 FinalExam 2020-21 SemA AnslawlokyiNoch keine Bewertungen

- Philippine Journal of Development: Stock Market Development in The Philippines: Past & PresentDokument2 SeitenPhilippine Journal of Development: Stock Market Development in The Philippines: Past & PresentamerahNoch keine Bewertungen

- PMS Guide August 2019Dokument88 SeitenPMS Guide August 2019HetanshNoch keine Bewertungen

- Ias 33 EpsDokument4 SeitenIas 33 EpsMd. Mamunur RashidNoch keine Bewertungen

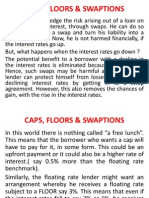

- Five-Caps, Floors & Swaptions 8Dokument8 SeitenFive-Caps, Floors & Swaptions 8Akhilesh SinghNoch keine Bewertungen

- Strategic Management 3rd Edition Rothaermel Test Bank DownloadDokument120 SeitenStrategic Management 3rd Edition Rothaermel Test Bank DownloadFrancine Lalinde100% (23)

- Cambridge International Examinations Cambridge International General Certificate of Secondary EducationDokument20 SeitenCambridge International Examinations Cambridge International General Certificate of Secondary Educationcharmainemakumbe60Noch keine Bewertungen

- Principles of Property ValuationDokument8 SeitenPrinciples of Property ValuationcivilsadiqNoch keine Bewertungen

- Prac ReviewDokument3 SeitenPrac ReviewYannah RebogioNoch keine Bewertungen