Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Global Top Executives ListDokument8 SeitenGlobal Top Executives ListSiju BoseNoch keine Bewertungen

- 500 Sensational Salads PDFDokument5 Seiten500 Sensational Salads PDFENACHE GEORGETA0% (4)

- Weight Watchers 200 Zero Point Freestyle Food List Printable 2Dokument2 SeitenWeight Watchers 200 Zero Point Freestyle Food List Printable 2Greisa Judy100% (1)

- Nifty 50 Reports For The Week (16-20th August '11)Dokument52 SeitenNifty 50 Reports For The Week (16-20th August '11)Dasher_No_1Noch keine Bewertungen

- Bullion Commodity Reports For The Week (1st - 5th August '11)Dokument8 SeitenBullion Commodity Reports For The Week (1st - 5th August '11)Dasher_No_1Noch keine Bewertungen

- Stock Market Reports For The Week (16-20th August '11)Dokument5 SeitenStock Market Reports For The Week (16-20th August '11)Dasher_No_1Noch keine Bewertungen

- Stock Market Reports For The Week (25th - 29th July '11)Dokument5 SeitenStock Market Reports For The Week (25th - 29th July '11)Dasher_No_1Noch keine Bewertungen

- Agri Commodity Reports For The Week (8th - 12th August '11)Dokument6 SeitenAgri Commodity Reports For The Week (8th - 12th August '11)Dasher_No_1Noch keine Bewertungen

- Stock Market Reports For The Week (8th - 12th August '11)Dokument5 SeitenStock Market Reports For The Week (8th - 12th August '11)Dasher_No_1Noch keine Bewertungen

- Bullion Commodity Reports For The Week (16-20th August '11)Dokument8 SeitenBullion Commodity Reports For The Week (16-20th August '11)Dasher_No_1Noch keine Bewertungen

- Agri Commodity Reports For The Week (16-20th August '11)Dokument6 SeitenAgri Commodity Reports For The Week (16-20th August '11)Dasher_No_1Noch keine Bewertungen

- Stock Market Reports For The Week (1st - 5th August '11)Dokument5 SeitenStock Market Reports For The Week (1st - 5th August '11)Dasher_No_1Noch keine Bewertungen

- Nifty 50 Reports For The Week (8th - 12th August '11)Dokument52 SeitenNifty 50 Reports For The Week (8th - 12th August '11)Dasher_No_1Noch keine Bewertungen

- Stock Futures and Option Reports For The Week (25th - 29th July '11)Dokument4 SeitenStock Futures and Option Reports For The Week (25th - 29th July '11)Dasher_No_1Noch keine Bewertungen

- Stock Futures and Options Reports For The Week (8th - 12th August '11)Dokument4 SeitenStock Futures and Options Reports For The Week (8th - 12th August '11)Dasher_No_1Noch keine Bewertungen

- Bullion Commodity Reports For The Week (8th - 12th August '11)Dokument8 SeitenBullion Commodity Reports For The Week (8th - 12th August '11)Dasher_No_1Noch keine Bewertungen

- Rollover Statistics (From July 2011 Series To September 2011 Series)Dokument10 SeitenRollover Statistics (From July 2011 Series To September 2011 Series)Dasher_No_1Noch keine Bewertungen

- Nifty 50 Reports For The Week (1st - 5th August '11)Dokument52 SeitenNifty 50 Reports For The Week (1st - 5th August '11)Dasher_No_1Noch keine Bewertungen

- Stock Market Reports For The Week (11th - 15th July '11)Dokument5 SeitenStock Market Reports For The Week (11th - 15th July '11)Dasher_No_1Noch keine Bewertungen

- Nifty 50 Reports For The Week (25th - 29th July '11)Dokument52 SeitenNifty 50 Reports For The Week (25th - 29th July '11)Dasher_No_1Noch keine Bewertungen

- Agri Commodity Reports For The Week (25th - 29th July '11)Dokument6 SeitenAgri Commodity Reports For The Week (25th - 29th July '11)Dasher_No_1Noch keine Bewertungen

- Agri Commodity Reports For The Week (1st - 5th August '11)Dokument6 SeitenAgri Commodity Reports For The Week (1st - 5th August '11)Dasher_No_1Noch keine Bewertungen

- Bullion Commodity Reports For The Week (25th - 29th July '11)Dokument8 SeitenBullion Commodity Reports For The Week (25th - 29th July '11)Dasher_No_1Noch keine Bewertungen

- Nifty 50 Reports For The Week (11th - 15th July '11)Dokument52 SeitenNifty 50 Reports For The Week (11th - 15th July '11)Dasher_No_1Noch keine Bewertungen

- Bulion Commodity Reports For The Week (11th - 15th July '11)Dokument8 SeitenBulion Commodity Reports For The Week (11th - 15th July '11)Dasher_No_1Noch keine Bewertungen

- Agri Commodity Reports For The Week (11th - 15th July '11)Dokument6 SeitenAgri Commodity Reports For The Week (11th - 15th July '11)Dasher_No_1Noch keine Bewertungen

- Stock Market Reports For The Week (4th - 8th July '11)Dokument5 SeitenStock Market Reports For The Week (4th - 8th July '11)Dasher_No_1Noch keine Bewertungen

- Rollover Statistics (From June 2011 Series To July 2011 Series)Dokument10 SeitenRollover Statistics (From June 2011 Series To July 2011 Series)Dasher_No_1Noch keine Bewertungen

- Bullion Commodity Reports For The Week (4th - 8th July '11)Dokument8 SeitenBullion Commodity Reports For The Week (4th - 8th July '11)Dasher_No_1Noch keine Bewertungen

- Nifty 50 Reports For The Week (4th - 8th July '11)Dokument52 SeitenNifty 50 Reports For The Week (4th - 8th July '11)Dasher_No_1Noch keine Bewertungen

- Ayurveda MDokument28 SeitenAyurveda MhajihalviNoch keine Bewertungen

- Engineering Consultant in AUHDokument11 SeitenEngineering Consultant in AUHShameem JazirNoch keine Bewertungen

- Nix v. Hedden, 149 U.S. 304 (1893)Dokument3 SeitenNix v. Hedden, 149 U.S. 304 (1893)Scribd Government DocsNoch keine Bewertungen

- Kitchen Expenses May 2015Dokument180 SeitenKitchen Expenses May 2015Bong Urbano AIcantaraNoch keine Bewertungen

- Detox Food Plan: Weekly Planner and RecipesDokument42 SeitenDetox Food Plan: Weekly Planner and RecipesAnupam Das100% (1)

- GI Foundation Low GI Shopping List Web PDFDokument2 SeitenGI Foundation Low GI Shopping List Web PDFJoycee MejiaNoch keine Bewertungen

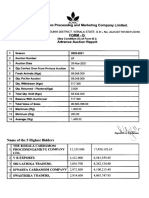

- Ero"" "Iltjtia: Kerala Cardamom Marketing Company LimitedDokument25 SeitenEro"" "Iltjtia: Kerala Cardamom Marketing Company LimitedRoshniNoch keine Bewertungen

- 1 Japanese Tea HistoryDokument5 Seiten1 Japanese Tea HistoryYi LiangNoch keine Bewertungen

- Ragam Kultivar Kopi Di LampungDokument9 SeitenRagam Kultivar Kopi Di LampungDanur WendaNoch keine Bewertungen

- Phase Chart 082210Dokument2 SeitenPhase Chart 082210Teodor MarcelNoch keine Bewertungen

- Growing Sweet Corn OrganicallyDokument1 SeiteGrowing Sweet Corn OrganicallySchool Vegetable GardeningNoch keine Bewertungen

- 101 Ways To Increase Your Load and Sperm CountDokument10 Seiten101 Ways To Increase Your Load and Sperm CountyudaNoch keine Bewertungen

- Production Technology of Carambola Botanical Name: Averrhoa Carambola Family: Oxalidaceae Origin: Indonesia Chromosome No: 2n 24Dokument3 SeitenProduction Technology of Carambola Botanical Name: Averrhoa Carambola Family: Oxalidaceae Origin: Indonesia Chromosome No: 2n 24Gopu ChiyaanNoch keine Bewertungen

- Teknik Budidaya Dan Kolam Terpal: Azolla Microphylla PADA MEDIA EMBERDokument5 SeitenTeknik Budidaya Dan Kolam Terpal: Azolla Microphylla PADA MEDIA EMBERAde MulyanaNoch keine Bewertungen

- English Iii I. Objective Learning CompetenciesDokument7 SeitenEnglish Iii I. Objective Learning CompetenciesJohn Lister Candido Mondia100% (1)

- Botany Fourth Sem Unit 1 Origin and Domestication of Cultivated PlantsDokument7 SeitenBotany Fourth Sem Unit 1 Origin and Domestication of Cultivated PlantsIsha KhanNoch keine Bewertungen

- Characteristics) Updated (For Info)Dokument4 SeitenCharacteristics) Updated (For Info)Ana BelleNoch keine Bewertungen

- Seed Sowing Guide: Month by Month Cool Climate (Daylesford)Dokument1 SeiteSeed Sowing Guide: Month by Month Cool Climate (Daylesford)Anonymous sqER4o7BNoch keine Bewertungen

- Hydroponic Vegetables: Plants PH CF EC PPMDokument1 SeiteHydroponic Vegetables: Plants PH CF EC PPMlongez87Noch keine Bewertungen

- HSN Codes ListDokument564 SeitenHSN Codes ListpurushottamNoch keine Bewertungen

- Gmo PresentationDokument26 SeitenGmo PresentationRoshi Desai67% (3)

- Lead The Way 1 Worksheets Vocabulary Complete PDFDokument18 SeitenLead The Way 1 Worksheets Vocabulary Complete PDFngonzalezlegazpeNoch keine Bewertungen

- Tomatoes Determinate PDFDokument1 SeiteTomatoes Determinate PDFOcelio MucudosNoch keine Bewertungen

- Cash Price Report 030810Dokument1 SeiteCash Price Report 030810wsocNoch keine Bewertungen

- Intercropping in Oil Palm Plantations A Technical GuideDokument56 SeitenIntercropping in Oil Palm Plantations A Technical GuideHafizul HisyamNoch keine Bewertungen

- Variety of Fresh & Frozen Seafood ProductsDokument18 SeitenVariety of Fresh & Frozen Seafood ProductsASDFNoch keine Bewertungen