Das könnte Ihnen auch gefallen

- Fertilizer Sector: Urea Production Witnessed A Five Year LowDokument2 SeitenFertilizer Sector: Urea Production Witnessed A Five Year LowMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: LUCK - FY11 Result ExpectationDokument1 SeiteCement Sector: LUCK - FY11 Result ExpectationMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Automotive Sector: June'11 - Car Sales Fall For A Good ReasonDokument1 SeiteAutomotive Sector: June'11 - Car Sales Fall For A Good ReasonMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFBL Result PreviewDokument1 SeiteFertilizer Sector: FFBL Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: FY2011 - A Year Dominated by Devils of Poor Demand and Rise in Input CostsDokument2 SeitenCement Sector: FY2011 - A Year Dominated by Devils of Poor Demand and Rise in Input CostsMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFC Result PreviewDokument1 SeiteFertilizer Sector: FFC Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFC Result PreviewDokument1 SeiteFertilizer Sector: FFC Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: Dispatches Slow Down ContinuesDokument1 SeiteCement Sector: Dispatches Slow Down ContinuesMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: ACPL - Easing Coal Prices Expected To Bode WellDokument1 SeiteCement Sector: ACPL - Easing Coal Prices Expected To Bode WellMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: Poor Demand Continues To Hamper DispatchesDokument2 SeitenCement Sector: Poor Demand Continues To Hamper DispatchesMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector - Yet Another Episode of Substantial Growth in EarningsDokument2 SeitenFertilizer Sector - Yet Another Episode of Substantial Growth in EarningsMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector - CY10 Ended Up With Rock Solid EarningsDokument2 SeitenFertilizer Sector - CY10 Ended Up With Rock Solid EarningsMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Automotive Sector: May - Not A Holy MonthDokument1 SeiteAutomotive Sector: May - Not A Holy MonthMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector - Yet Another Episode of Substantial Growth in EarningsDokument2 SeitenFertilizer Sector - Yet Another Episode of Substantial Growth in EarningsMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: Export Demand Bounces BackDokument1 SeiteCement Sector: Export Demand Bounces BackMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement: DGKC - 9MFY11 Financial Performance PreviewDokument1 SeiteCement: DGKC - 9MFY11 Financial Performance PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFBL Result PreviewDokument1 SeiteFertilizer Sector: FFBL Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFBL - A Good BUYDokument1 SeiteFertilizer Sector: FFBL - A Good BUYMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: Numbers Spell Out An Upshot of Soaring PricesDokument1 SeiteFertilizer Sector: Numbers Spell Out An Upshot of Soaring PricesMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: FFBL Result PreviewDokument1 SeiteFertilizer Sector: FFBL Result PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: DGKC - Subdued Demand and Rising Input Costs Hurting Core BusinessDokument2 SeitenCement Sector: DGKC - Subdued Demand and Rising Input Costs Hurting Core BusinessMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Fertilizer Sector: Offtake Dropped by 22% YoYDokument1 SeiteFertilizer Sector: Offtake Dropped by 22% YoYMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: All Eyes On 2HFY11Dokument1 SeiteCement Sector: All Eyes On 2HFY11Muhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement: DGKC - 9MFY11 Financial Performance PreviewDokument1 SeiteCement: DGKC - 9MFY11 Financial Performance PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement: DGKC - 1HY11 Financial Performance PreviewDokument1 SeiteCement: DGKC - 1HY11 Financial Performance PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: ACPL - 1HFY11 Financial Performance ReviewDokument1 SeiteCement Sector: ACPL - 1HFY11 Financial Performance ReviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: The War of Survival Is Still OnDokument2 SeitenCement Sector: The War of Survival Is Still OnMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: LUCK - 1H/FY11 Results PreviewDokument2 SeitenCement Sector: LUCK - 1H/FY11 Results PreviewMuhammad Sarfraz AbbasiNoch keine Bewertungen

- Cement Sector: LUCK Missing Luck As Volumes Remain DoomedDokument2 SeitenCement Sector: LUCK Missing Luck As Volumes Remain DoomedMuhammad Sarfraz AbbasiNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- 500 Usd To Idr - Google SearchDokument1 Seite500 Usd To Idr - Google SearchparamagandiNoch keine Bewertungen

- Iccr QuestionsDokument4 SeitenIccr QuestionsEASSANoch keine Bewertungen

- OpTransactionHistory03 11 2023Dokument9 SeitenOpTransactionHistory03 11 2023abhay singhNoch keine Bewertungen

- PPTDokument19 SeitenPPTShivika Chanda100% (1)

- Price List For Fiesta Homes by SJR PrimecorpDokument1 SeitePrice List For Fiesta Homes by SJR PrimecorpAswath FarookNoch keine Bewertungen

- Project ProposalDokument5 SeitenProject ProposalVineet GargNoch keine Bewertungen

- Ey - Report - Ipo Q1 2019Dokument37 SeitenEy - Report - Ipo Q1 2019JimmyNoch keine Bewertungen

- Special Release Goat Situation ReportDokument8 SeitenSpecial Release Goat Situation ReportYumie YamazukiNoch keine Bewertungen

- Real Estate in Israel - Y.H. Dimri Construction - Israel ExporterDokument1 SeiteReal Estate in Israel - Y.H. Dimri Construction - Israel ExporterIsrael ExporterNoch keine Bewertungen

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDokument1 SeiteBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountVivek Tiwari VTNoch keine Bewertungen

- 4 Government Initiatives BOP BOTDokument18 Seiten4 Government Initiatives BOP BOTsaranya sivakumarNoch keine Bewertungen

- UntitledDokument45 SeitenUntitledfdwfwffNoch keine Bewertungen

- October 5, 2018: Andrew M. Cuomo Robert F. Mujica Jr. Sandra L. BeattieDokument2 SeitenOctober 5, 2018: Andrew M. Cuomo Robert F. Mujica Jr. Sandra L. BeattieNick ReismanNoch keine Bewertungen

- 31 DECAMBER FromDokument8 Seiten31 DECAMBER FromMd Rajikul IslamNoch keine Bewertungen

- Ethiopia Agriculture Market AnalysisDokument5 SeitenEthiopia Agriculture Market Analysiskeder abubkerNoch keine Bewertungen

- Payslip - 2021 03 05Dokument1 SeitePayslip - 2021 03 05Mark Lawrence Yusi100% (1)

- Boosting Agriculture and Its Effect On Pakistan's Economy: OutlineDokument1 SeiteBoosting Agriculture and Its Effect On Pakistan's Economy: OutlineHaider AliNoch keine Bewertungen

- FY23 Budget One-PagerDokument2 SeitenFY23 Budget One-PagerWDIV/ClickOnDetroitNoch keine Bewertungen

- Companies For SIC 8888 - FOREIGN GOVERNMENTSDokument2 SeitenCompanies For SIC 8888 - FOREIGN GOVERNMENTSBrave Powers100% (2)

- ITLP - Notes2Dokument9 SeitenITLP - Notes2Louis MalaybalayNoch keine Bewertungen

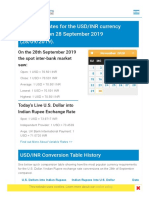

- U.S. Dollar To Indian Rupee Exchange Rate History - 28 September 2019 (28 - 09 - 2019) UsdDokument6 SeitenU.S. Dollar To Indian Rupee Exchange Rate History - 28 September 2019 (28 - 09 - 2019) UsdAnish KumarNoch keine Bewertungen

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument39 SeitenDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancemayur bhargaNoch keine Bewertungen

- BRAHMAKAMALDokument1 SeiteBRAHMAKAMALsales Brahma KamalNoch keine Bewertungen

- Ecommerce in MPDokument26 SeitenEcommerce in MPishanhbmehtaNoch keine Bewertungen

- BOSCHDokument1 SeiteBOSCHKolkata Jyote MotorsNoch keine Bewertungen

- E-Way Bill - 7Dokument2 SeitenE-Way Bill - 7AshishTrivediNoch keine Bewertungen

- Silicon Valley BankDokument1 SeiteSilicon Valley BankDaisy BajarNoch keine Bewertungen

- PESCO ONLINE BILL NovemberDokument2 SeitenPESCO ONLINE BILL NovemberSyed Ali ShahNoch keine Bewertungen

- "An Analytical Study of Foreign Direct Investment in IndiaDokument11 Seiten"An Analytical Study of Foreign Direct Investment in IndiaGokul krishnanNoch keine Bewertungen

- Inventory Still Low As Buyers Struggle To Find Properties in AlabamaDokument14 SeitenInventory Still Low As Buyers Struggle To Find Properties in AlabamaJeff WyattNoch keine Bewertungen