Das könnte Ihnen auch gefallen

- Health and Hatha Yoga by Swami Sivananda CompressDokument356 SeitenHealth and Hatha Yoga by Swami Sivananda CompressLama Fera with Yachna JainNoch keine Bewertungen

- The Skylane Pilot's CompanionDokument221 SeitenThe Skylane Pilot's CompanionItayefrat100% (6)

- GIllette Marketing ReportDokument91 SeitenGIllette Marketing ReportAbhishek Anand96% (27)

- Rudolf Steiner - Twelve Senses in Man GA 206Dokument67 SeitenRudolf Steiner - Twelve Senses in Man GA 206Raul PopescuNoch keine Bewertungen

- Economics and Agricultural EconomicsDokument28 SeitenEconomics and Agricultural EconomicsM Hossain AliNoch keine Bewertungen

- Real Estate Valuation Case Study: IIM Indore Abhishek Anand Team Name: Analyst 09833167105Dokument20 SeitenReal Estate Valuation Case Study: IIM Indore Abhishek Anand Team Name: Analyst 09833167105Abhishek Anand100% (1)

- (Adolescence and Education) Tim Urdan, Frank Pajares - Academic Motivation of Adolescents-IAP - Information Age Publishing (2004) PDFDokument384 Seiten(Adolescence and Education) Tim Urdan, Frank Pajares - Academic Motivation of Adolescents-IAP - Information Age Publishing (2004) PDFAllenNoch keine Bewertungen

- Talbros AutomotiveDokument6 SeitenTalbros AutomotiveAhmed NiazNoch keine Bewertungen

- TrematodesDokument95 SeitenTrematodesFarlogy100% (3)

- Lecture 8 - 8 Point and EV To EBITDA by CA Rachana RanadeDokument8 SeitenLecture 8 - 8 Point and EV To EBITDA by CA Rachana RanadeMufaddal DaginawalaNoch keine Bewertungen

- Bond Stock Valuation Gr2 07-03Dokument13 SeitenBond Stock Valuation Gr2 07-03Himanshu GuptaNoch keine Bewertungen

- Krakatau Steel A CaseDokument9 SeitenKrakatau Steel A CaseFarhan SoepraptoNoch keine Bewertungen

- Nifty50 Q2 FY18 Quarterly EstimatesDokument8 SeitenNifty50 Q2 FY18 Quarterly Estimatessrinivas NNoch keine Bewertungen

- Balance Sheet AnalysisDokument25 SeitenBalance Sheet Analysissinger0% (1)

- CHapter 4 - ThesisDokument34 SeitenCHapter 4 - ThesisPradipta KafleNoch keine Bewertungen

- Orange FinancialDokument35 SeitenOrange Financialosama aboualamNoch keine Bewertungen

- Manappuram Finance Investor PresentationDokument43 SeitenManappuram Finance Investor PresentationabmahendruNoch keine Bewertungen

- Matriks Valuasi Saham Sharia 11 May 2020Dokument4 SeitenMatriks Valuasi Saham Sharia 11 May 2020hendarwinNoch keine Bewertungen

- Dividend Yield Stocks: Retail ResearchDokument2 SeitenDividend Yield Stocks: Retail ResearchrajivNoch keine Bewertungen

- Analisis Keuangan Semen IndonesiaDokument17 SeitenAnalisis Keuangan Semen IndonesiaAnnas Rozi JuliantoNoch keine Bewertungen

- Matriks Valuasi Saham Sharia 18 May 2020Dokument1 SeiteMatriks Valuasi Saham Sharia 18 May 2020hendarwinNoch keine Bewertungen

- Dominic InterpretationDokument11 SeitenDominic Interpretationdominic wurdaNoch keine Bewertungen

- GR I Crew XV 2018 TcsDokument79 SeitenGR I Crew XV 2018 TcsMUKESH KUMARNoch keine Bewertungen

- Matriks Valuasi Saham 22 Juni 2020 PDFDokument2 SeitenMatriks Valuasi Saham 22 Juni 2020 PDFbala gamerNoch keine Bewertungen

- Matrix Valuasi Saham Syariah 1 Mar 21Dokument1 SeiteMatrix Valuasi Saham Syariah 1 Mar 21haji atinNoch keine Bewertungen

- Mahindra & Mahindra: 3 August 2009Dokument8 SeitenMahindra & Mahindra: 3 August 2009Chandni OzaNoch keine Bewertungen

- Pacific Grove Spice CompanyDokument3 SeitenPacific Grove Spice CompanyLaura JavelaNoch keine Bewertungen

- Analysis of 10 Stocks On The Basis of Sales by Expenses and Other Ratios Which Covered in First Part of Finance SessionsDokument10 SeitenAnalysis of 10 Stocks On The Basis of Sales by Expenses and Other Ratios Which Covered in First Part of Finance SessionsPRADIP.KUMAR SHUKLANoch keine Bewertungen

- Chapter I: Introduction1Dokument53 SeitenChapter I: Introduction1Raz BinadiNoch keine Bewertungen

- Al Shaheer CompsDokument4 SeitenAl Shaheer CompsAbdullah YousufNoch keine Bewertungen

- Ten Years 2006Dokument2 SeitenTen Years 2006Zeeshan SiddiqueNoch keine Bewertungen

- Performance Analysis of Tata Motors and Maruti SuzukiDokument13 SeitenPerformance Analysis of Tata Motors and Maruti SuzukisherlyNoch keine Bewertungen

- Key Ratio Analysis: Profitability RatiosDokument27 SeitenKey Ratio Analysis: Profitability RatioskritikaNoch keine Bewertungen

- Statement For AAPLDokument1 SeiteStatement For AAPLEzequiel FriossoNoch keine Bewertungen

- DCF NHLDokument5 SeitenDCF NHLMittal Kirti MukeshNoch keine Bewertungen

- Britannia IndustriesDokument12 SeitenBritannia Industriesmundadaharsh1Noch keine Bewertungen

- Ashok Leyland Kotak 050218Dokument4 SeitenAshok Leyland Kotak 050218suprabhattNoch keine Bewertungen

- Top 50 World BanksDokument1 SeiteTop 50 World BanksKicki AnderssonNoch keine Bewertungen

- Krakatau Steel Case Financial Management Assignment - Syndicate 6Dokument10 SeitenKrakatau Steel Case Financial Management Assignment - Syndicate 6Ayustina GiustiNoch keine Bewertungen

- Top Picks-June 2015Dokument9 SeitenTop Picks-June 2015saveclipNoch keine Bewertungen

- Ambuja Cements: NeutralDokument8 SeitenAmbuja Cements: Neutral张迪Noch keine Bewertungen

- PSE Dividend InvestingDokument92 SeitenPSE Dividend InvestingAVNoch keine Bewertungen

- ST BK of IndiaDokument42 SeitenST BK of IndiaSuyaesh SinghaniyaNoch keine Bewertungen

- Rasio PT Indofood 2015 2016 2017 Rasio Likuiditas: PT Myor PT Sari PT UltjDokument3 SeitenRasio PT Indofood 2015 2016 2017 Rasio Likuiditas: PT Myor PT Sari PT UltjThatavirgin MarthaliaNoch keine Bewertungen

- Lakshmi Electrical Control SupportDokument14 SeitenLakshmi Electrical Control SupportAmeesha DubeyNoch keine Bewertungen

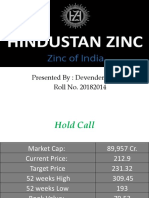

- Hindustan ZincDokument8 SeitenHindustan ZincDevender SharmaNoch keine Bewertungen

- Alro SA (ALR RO) - Adj HighlightsDokument147 SeitenAlro SA (ALR RO) - Adj HighlightsAlexLupescuNoch keine Bewertungen

- Fundamental Sheet Bharat RasayanDokument28 SeitenFundamental Sheet Bharat RasayanVishal WaghNoch keine Bewertungen

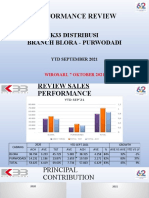

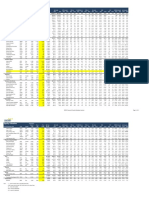

- Performance Review: K33 Distribusi Branch Blora - PurwodadiDokument14 SeitenPerformance Review: K33 Distribusi Branch Blora - PurwodadiCipto Saritomo S.PNoch keine Bewertungen

- Radico KhaitanDokument38 SeitenRadico Khaitantapasya khanijouNoch keine Bewertungen

- FM Assigment 14 FebDokument6 SeitenFM Assigment 14 FebSubhajit HazraNoch keine Bewertungen

- Equity Valuation: REDS-Research Equity Database System Page 1 of 2Dokument2 SeitenEquity Valuation: REDS-Research Equity Database System Page 1 of 2srijokoNoch keine Bewertungen

- Top 17 Stocks BuyDokument13 SeitenTop 17 Stocks BuySushilNoch keine Bewertungen

- Marks & Spencer PLCDokument7 SeitenMarks & Spencer PLCMoona AwanNoch keine Bewertungen

- Cfin2 HW1Dokument25 SeitenCfin2 HW1Anirudh BharNoch keine Bewertungen

- Polaroid 1996 CalculationDokument8 SeitenPolaroid 1996 CalculationDev AnandNoch keine Bewertungen

- Valuation ModelsDokument11 SeitenValuation ModelsPIYA THAKURNoch keine Bewertungen

- Doddy Bicara InvestasiDokument38 SeitenDoddy Bicara InvestasiNur Cholik Widyan SaNoch keine Bewertungen

- Freefincal Stock Analyzer May 2017 SCR Edition Earnings Power Box 1Dokument1.257 SeitenFreefincal Stock Analyzer May 2017 SCR Edition Earnings Power Box 1Positive ThinkerNoch keine Bewertungen

- Q3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleDokument12 SeitenQ3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleSAGAR VAZIRANINoch keine Bewertungen

- Campbell Soups Company: Year 11 Year 10 Year 9 Net Sales Costs and ExpensesDokument2 SeitenCampbell Soups Company: Year 11 Year 10 Year 9 Net Sales Costs and ExpensesBhavesh MotwaniNoch keine Bewertungen

- Campbell SoupsDokument2 SeitenCampbell SoupsBhavesh MotwaniNoch keine Bewertungen

- Name of The Company Last Financial Year First Projected Year CurrencyDokument15 SeitenName of The Company Last Financial Year First Projected Year CurrencygabegwNoch keine Bewertungen

- Cummins India Financial ModelDokument52 SeitenCummins India Financial ModelJitendra YadavNoch keine Bewertungen

- ValueResearchFundcard JMCore11Fund 2019apr18Dokument4 SeitenValueResearchFundcard JMCore11Fund 2019apr18ChittaNoch keine Bewertungen

- Sec-A - Group 8 - SecureNowDokument7 SeitenSec-A - Group 8 - SecureNowPuneet GargNoch keine Bewertungen

- Hoàng Lê Hải Yến-Internal AuditDokument3 SeitenHoàng Lê Hải Yến-Internal AuditHoàng Lê Hải YếnNoch keine Bewertungen

- CAMEL Analysis For Indian BanksDokument10 SeitenCAMEL Analysis For Indian BanksAbhishek Anand75% (4)

- Risk at Freddie MacDokument10 SeitenRisk at Freddie MacAbhishek Anand100% (2)

- Hawkins Cooker LTD: Stable Business, Limited Growth OpportunitiesDokument8 SeitenHawkins Cooker LTD: Stable Business, Limited Growth OpportunitiesAbhishek Anand100% (4)

- Formats Vs FeelingDokument5 SeitenFormats Vs FeelingAbhishek AnandNoch keine Bewertungen

- Astm D1895 17Dokument4 SeitenAstm D1895 17Sonia Goncalves100% (1)

- Ra 7877Dokument16 SeitenRa 7877Anonymous FExJPnCNoch keine Bewertungen

- Circular No 02 2014 TA DA 010115 PDFDokument10 SeitenCircular No 02 2014 TA DA 010115 PDFsachin sonawane100% (1)

- Chemical BondingDokument7 SeitenChemical BondingSanaa SamkoNoch keine Bewertungen

- Abnormal PsychologyDokument4 SeitenAbnormal PsychologyTania LodiNoch keine Bewertungen

- Iluminadores y DipolosDokument9 SeitenIluminadores y DipolosRamonNoch keine Bewertungen

- Approach To A Case of ScoliosisDokument54 SeitenApproach To A Case of ScoliosisJocuri KosoNoch keine Bewertungen

- Quiz 07Dokument15 SeitenQuiz 07Ije Love100% (1)

- HDFC Bank-Centurion Bank of Punjab: Presented By: Sachi Bani Perhar Mba-Ib 2010-2012Dokument40 SeitenHDFC Bank-Centurion Bank of Punjab: Presented By: Sachi Bani Perhar Mba-Ib 2010-2012Sumit MalikNoch keine Bewertungen

- Green Campus Concept - A Broader View of A Sustainable CampusDokument14 SeitenGreen Campus Concept - A Broader View of A Sustainable CampusHari HaranNoch keine Bewertungen

- Linkedin Job Invite MessageDokument4 SeitenLinkedin Job Invite MessageAxiom IntNoch keine Bewertungen

- KB000120-MRK456-01-HR SamplingDokument15 SeitenKB000120-MRK456-01-HR SamplingMiguel Zuniga MarconiNoch keine Bewertungen

- Responsive Docs - CREW Versus Department of Justice (DOJ) : Regarding Investigation Records of Magliocchetti: 11/12/13 - Part 3Dokument172 SeitenResponsive Docs - CREW Versus Department of Justice (DOJ) : Regarding Investigation Records of Magliocchetti: 11/12/13 - Part 3CREWNoch keine Bewertungen

- Duterte Vs SandiganbayanDokument17 SeitenDuterte Vs SandiganbayanAnonymous KvztB3Noch keine Bewertungen

- Spice Processing UnitDokument3 SeitenSpice Processing UnitKSHETRIMAYUM MONIKA DEVINoch keine Bewertungen

- AI in HealthDokument105 SeitenAI in HealthxenoachNoch keine Bewertungen

- Lifelong Learning: Undergraduate Programs YouDokument8 SeitenLifelong Learning: Undergraduate Programs YouJavier Pereira StraubeNoch keine Bewertungen

- OPSS 415 Feb90Dokument7 SeitenOPSS 415 Feb90Muhammad UmarNoch keine Bewertungen

- Foucault, M.-Experience-Book (Trombadori Interview)Dokument11 SeitenFoucault, M.-Experience-Book (Trombadori Interview)YashinNoch keine Bewertungen

- Aqualab ClinicDokument12 SeitenAqualab ClinichonyarnamiqNoch keine Bewertungen

- Picc Lite ManualDokument366 SeitenPicc Lite Manualtanny_03Noch keine Bewertungen

- Jewish Standard, September 16, 2016Dokument72 SeitenJewish Standard, September 16, 2016New Jersey Jewish StandardNoch keine Bewertungen

- Describe The Forms of Agency CompensationDokument2 SeitenDescribe The Forms of Agency CompensationFizza HassanNoch keine Bewertungen

- Haloperidol PDFDokument4 SeitenHaloperidol PDFfatimahNoch keine Bewertungen