Das könnte Ihnen auch gefallen

- Assignment International Economic LawDokument16 SeitenAssignment International Economic LawreazNoch keine Bewertungen

- WtoDokument46 SeitenWtoEmelie Marie DiezNoch keine Bewertungen

- Most Favoured Nation Concept in WtoDokument23 SeitenMost Favoured Nation Concept in Wtorishabhsingh261100% (1)

- History of GattDokument38 SeitenHistory of GattAdil100% (3)

- The Implication of Iraqi Invasion of Kuwait, A Legal Study Within The Framework of The UN CharterDokument25 SeitenThe Implication of Iraqi Invasion of Kuwait, A Legal Study Within The Framework of The UN CharterPhung Thi Minh YenNoch keine Bewertungen

- Free Trade, Wto and Regional Grouping ofDokument54 SeitenFree Trade, Wto and Regional Grouping ofSoumendra RoyNoch keine Bewertungen

- Emergence of WtoDokument2 SeitenEmergence of Wtorash4ever2uNoch keine Bewertungen

- GattDokument14 SeitenGattSan Santiago Chapel Muzon0% (1)

- Institutional Reform of The WTODokument27 SeitenInstitutional Reform of The WTOOxfamNoch keine Bewertungen

- Direct Effect + SupremacyDokument10 SeitenDirect Effect + Supremacynayab tNoch keine Bewertungen

- Martin and Anthony On AminoilDokument36 SeitenMartin and Anthony On AminoilBello FolakemiNoch keine Bewertungen

- Issues Raised by Parallel Proceedings and Possible SolutionsDokument9 SeitenIssues Raised by Parallel Proceedings and Possible SolutionsGroove'N'Move GNM100% (1)

- Dispute Settlement in WtoDokument23 SeitenDispute Settlement in Wtorishabhsingh261Noch keine Bewertungen

- Functions of WTODokument3 SeitenFunctions of WTORajeev PoudelNoch keine Bewertungen

- Conflicts Between ITLOS and ICJDokument13 SeitenConflicts Between ITLOS and ICJManu Lemente100% (1)

- Public International LawDokument6 SeitenPublic International LawEllis DavidsonNoch keine Bewertungen

- Orld Rade Rganization: Presented by Amee Nagar Sachin Dhanke Satabdi MandalDokument23 SeitenOrld Rade Rganization: Presented by Amee Nagar Sachin Dhanke Satabdi MandalRohan RodriguesNoch keine Bewertungen

- International Investment Law - Module 1 and 4 BITs FinalDokument38 SeitenInternational Investment Law - Module 1 and 4 BITs FinalNeha SachdevaNoch keine Bewertungen

- Individual Assignment WtoDokument12 SeitenIndividual Assignment WtoRaimi MardhiahNoch keine Bewertungen

- The Role of The Security Council in The Use of Force Against The Islamic State' (2016)Dokument35 SeitenThe Role of The Security Council in The Use of Force Against The Islamic State' (2016)Antonio HenriqueNoch keine Bewertungen

- Adv of CisgDokument8 SeitenAdv of CisgKhushi SharmaNoch keine Bewertungen

- Judicial Review of Government ProcurementDokument22 SeitenJudicial Review of Government ProcurementMargaret RoseNoch keine Bewertungen

- Settlement of DisputesDokument3 SeitenSettlement of DisputesJassey Jane OrapaNoch keine Bewertungen

- Only The Workers Can Free The Workers: The Origin of The Workers' Control Tradition and The Trade Union Advisory Coordinating Committee (TUACC), 1970-1979.Dokument284 SeitenOnly The Workers Can Free The Workers: The Origin of The Workers' Control Tradition and The Trade Union Advisory Coordinating Committee (TUACC), 1970-1979.TigersEye99100% (1)

- The Need To Amend Article 38 of The Statue of The International Court of JusticeDokument11 SeitenThe Need To Amend Article 38 of The Statue of The International Court of JusticeGlobal Research and Development ServicesNoch keine Bewertungen

- Globalization and Environmental Degradation of Developing CountriesDokument22 SeitenGlobalization and Environmental Degradation of Developing CountriesMd. Badrul Islam100% (2)

- Fundamental Breach and The CISG - A Unique Treatment or Failed Experiment? Bruno ZellerDokument12 SeitenFundamental Breach and The CISG - A Unique Treatment or Failed Experiment? Bruno ZellerGuillermo C. DurelliNoch keine Bewertungen

- International Law of The Sea SyllabusDokument7 SeitenInternational Law of The Sea SyllabusTony George PuthucherrilNoch keine Bewertungen

- What Is The Difference Between GATT and WTO?Dokument3 SeitenWhat Is The Difference Between GATT and WTO?Crystal TayNoch keine Bewertungen

- The Treaty of Basseterre & OECS Economic UnionDokument15 SeitenThe Treaty of Basseterre & OECS Economic UnionOffice of Trade Negotiations (OTN), CARICOM SecretariatNoch keine Bewertungen

- Revision Notes Commercial Law CoursesDokument17 SeitenRevision Notes Commercial Law CoursesAlison MoklaNoch keine Bewertungen

- WTODokument48 SeitenWTOcrabrajesh007100% (4)

- Inter-State Maritime Territorial Conflict: A Study On Malaysia's Conflict Resolution Through Peaceful Means (Mohammad Zaki Ahmad and Musafir Kelana)Dokument17 SeitenInter-State Maritime Territorial Conflict: A Study On Malaysia's Conflict Resolution Through Peaceful Means (Mohammad Zaki Ahmad and Musafir Kelana)Vina ArisTantiaNoch keine Bewertungen

- Implementation of Cisg and of The System of International Commercial Arbitration in Southeast EuropeDokument49 SeitenImplementation of Cisg and of The System of International Commercial Arbitration in Southeast EuropeeucaleaNoch keine Bewertungen

- Statehood Territory Recognition and International Law Their Interrelationships by Emmanuel Yaw BennehDokument21 SeitenStatehood Territory Recognition and International Law Their Interrelationships by Emmanuel Yaw BennehHaruna-Rasheed MohammedNoch keine Bewertungen

- International TradeDokument19 SeitenInternational Tradelegalmatters89% (9)

- When Is The United Nations Charter Authorize The Use of Force by Gukiina PatrickDokument9 SeitenWhen Is The United Nations Charter Authorize The Use of Force by Gukiina PatrickGukiina PatrickNoch keine Bewertungen

- Assignment-GAAT WTODokument9 SeitenAssignment-GAAT WTOMohit Manandhar100% (1)

- WTO - Faculty NotesDokument23 SeitenWTO - Faculty Notesprashaant4uNoch keine Bewertungen

- Chapter 17 Interpretation and Application of Existing Wto RulesDokument11 SeitenChapter 17 Interpretation and Application of Existing Wto RulesWilliam HenryNoch keine Bewertungen

- Interim Measures and Emergency Arbitrator ProceedingsDokument26 SeitenInterim Measures and Emergency Arbitrator ProceedingsmutyokaNoch keine Bewertungen

- Treaties - Public International Law Group AssignmentDokument17 SeitenTreaties - Public International Law Group AssignmentKagi MogaeNoch keine Bewertungen

- Agreement On Subsidies and Countervailing Measures 16022011Dokument32 SeitenAgreement On Subsidies and Countervailing Measures 16022011Raja Chako Malhotra100% (1)

- Dispute SettlementDokument10 SeitenDispute SettlementdebasishroutNoch keine Bewertungen

- EU Law Exam Notes PDFDokument51 SeitenEU Law Exam Notes PDFstraNoch keine Bewertungen

- LAW3840 Worksheet1ADROverviewDokument11 SeitenLAW3840 Worksheet1ADROverviewRondelleKellerNoch keine Bewertungen

- Influence of Bilateral Investment Treaties On Customary International LawDokument4 SeitenInfluence of Bilateral Investment Treaties On Customary International LawBhavana ChowdaryNoch keine Bewertungen

- Controlling The Use of Force A Role For Human Rights Norms in Contemporary Armed ConflictDokument35 SeitenControlling The Use of Force A Role For Human Rights Norms in Contemporary Armed Conflict107625049Noch keine Bewertungen

- Commercial Dispute Resolution in China: An Annual Review and Preview 2020Von EverandCommercial Dispute Resolution in China: An Annual Review and Preview 2020Noch keine Bewertungen

- Regional Trade AgreementsDokument8 SeitenRegional Trade AgreementsAditya SharmaNoch keine Bewertungen

- World Trade OrganizationDokument7 SeitenWorld Trade OrganizationManav BathijaNoch keine Bewertungen

- International Trade Trade Barriers Trading BlocsDokument67 SeitenInternational Trade Trade Barriers Trading BlocsArvind BhardwajNoch keine Bewertungen

- The Problem of Grudge InformerDokument21 SeitenThe Problem of Grudge InformerArnav Kumar SharmaNoch keine Bewertungen

- 137 - Gatt, Gats, TripsDokument6 Seiten137 - Gatt, Gats, Tripsirma makharoblidze100% (1)

- Free Movement of Eu and Non-Eu CitizensDokument6 SeitenFree Movement of Eu and Non-Eu CitizensDajana GrgicNoch keine Bewertungen

- Dispute Settlement Mechanisms in International TradeDokument55 SeitenDispute Settlement Mechanisms in International TradeTamrika TyagiNoch keine Bewertungen

- Buddy Notes PILDokument37 SeitenBuddy Notes PILAbhinav KumarNoch keine Bewertungen

- International Economic LawDokument3 SeitenInternational Economic LawAnna Maria Kagaoan100% (1)

- Current Trends in FdiDokument14 SeitenCurrent Trends in Fdipunitrnair100% (1)

- Depsrtment: of @lucutionDokument34 SeitenDepsrtment: of @lucutionRaymond PasiliaoNoch keine Bewertungen

- 'Tffii: DepartmefiDokument32 Seiten'Tffii: DepartmefiRaymond PasiliaoNoch keine Bewertungen

- Department: @ducationDokument65 SeitenDepartment: @ducationRaymond PasiliaoNoch keine Bewertungen

- IPOPHL Memorandum Circular No. 2021 - 008 Extension of Deadlines For Filing and PaymentsDokument2 SeitenIPOPHL Memorandum Circular No. 2021 - 008 Extension of Deadlines For Filing and PaymentsRaymond PasiliaoNoch keine Bewertungen

- IPOPHL Memorandum Circular No. 2021-011 - Extension of Deadlines For Filings and PaymentsDokument2 SeitenIPOPHL Memorandum Circular No. 2021-011 - Extension of Deadlines For Filings and PaymentsRaymond PasiliaoNoch keine Bewertungen

- IPOPHL Memorandum Circular No. 2021 - 005 Extension of Deadlines in Light of The Declaration of An Enhanced Community QuarantineDokument2 SeitenIPOPHL Memorandum Circular No. 2021 - 005 Extension of Deadlines in Light of The Declaration of An Enhanced Community QuarantineRaymond PasiliaoNoch keine Bewertungen

- IPOPHL Memorandum Circular No. 2021-010 - Alternative Work Arrangment During The Modified Enhanced Community QuarantineDokument2 SeitenIPOPHL Memorandum Circular No. 2021-010 - Alternative Work Arrangment During The Modified Enhanced Community QuarantineRaymond PasiliaoNoch keine Bewertungen

- DTI Directory of Key OfficialsDokument15 SeitenDTI Directory of Key OfficialsRaymond PasiliaoNoch keine Bewertungen

- CONTEMPORARY-WORLD-REPORTDokument9 SeitenCONTEMPORARY-WORLD-REPORTPrincess Anne MendozaNoch keine Bewertungen

- International Business Chapter 1Dokument61 SeitenInternational Business Chapter 1Zahur AhmedNoch keine Bewertungen

- Consider The Following Illustrative Exchange Rates U S DollarsDokument1 SeiteConsider The Following Illustrative Exchange Rates U S DollarsAmit PandeyNoch keine Bewertungen

- International Trade and Capital FlowsDokument34 SeitenInternational Trade and Capital FlowsPrince AgrawalNoch keine Bewertungen

- C1 - Overview of International MarketingDokument9 SeitenC1 - Overview of International Marketinghương nguyễnNoch keine Bewertungen

- Certificate of Origin: North American Free Trade AgreementDokument1 SeiteCertificate of Origin: North American Free Trade AgreementSamir MiddyaNoch keine Bewertungen

- Ib Module 4 - NmimsDokument127 SeitenIb Module 4 - NmimsVed SolankiNoch keine Bewertungen

- Oj C 2023 241 Full en TXTDokument8 SeitenOj C 2023 241 Full en TXTRaluca IvanNoch keine Bewertungen

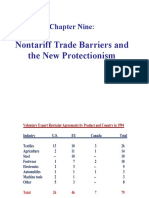

- Chapter Nine:: Nontariff Trade Barriers and The New ProtectionismDokument26 SeitenChapter Nine:: Nontariff Trade Barriers and The New ProtectionismAhmad RonyNoch keine Bewertungen

- Essentials of Wto LawDokument126 SeitenEssentials of Wto LawRitaEspindolaNoch keine Bewertungen

- Balance of PaymentDokument4 SeitenBalance of PaymentAMALA ANoch keine Bewertungen

- Img 20230804 0001Dokument6 SeitenImg 20230804 0001movpj1994Noch keine Bewertungen

- DissertationDokument27 SeitenDissertationWilmore Tendai Hasan ChisiiwaNoch keine Bewertungen

- Air Export PresentationDokument20 SeitenAir Export PresentationHardeepsehrawatNoch keine Bewertungen

- International Trade Theory: Eighth EditionDokument29 SeitenInternational Trade Theory: Eighth EditionCường ViNoch keine Bewertungen

- The Globalization of Economic RelationsDokument55 SeitenThe Globalization of Economic RelationsMark Anthony LegaspiNoch keine Bewertungen

- Bài tập Unit 3Dokument9 SeitenBài tập Unit 3Thu HàNoch keine Bewertungen

- Transcription Doc Foreign Trade: Speaker: Chris OatesDokument9 SeitenTranscription Doc Foreign Trade: Speaker: Chris OatesAnirban BhattacharyaNoch keine Bewertungen

- Terms and Concepts Associated With Caribbean Economies NotesDokument6 SeitenTerms and Concepts Associated With Caribbean Economies NotesKhaleel KothdiwalaNoch keine Bewertungen

- The Policy of Economic and International TradeDokument14 SeitenThe Policy of Economic and International TradeMohammad Ali RamadhanNoch keine Bewertungen

- Xam Idea Economics Chapter 5Dokument1 SeiteXam Idea Economics Chapter 5Kajal RanaNoch keine Bewertungen

- Gabay Sa PagwawastoDokument1 SeiteGabay Sa PagwawastoVINES100% (1)

- DE51660700240097750400 Mike Jefferson Mike Jefferson Mike JeffersonDokument1 SeiteDE51660700240097750400 Mike Jefferson Mike Jefferson Mike Jeffersonandres torresNoch keine Bewertungen

- NazewegukasubedeDokument2 SeitenNazewegukasubedeshaft181Noch keine Bewertungen

- Exchange RatesDokument10 SeitenExchange RatesMinhaj TariqNoch keine Bewertungen

- Lecture 4 - WTODokument36 SeitenLecture 4 - WTOVăn Trần Hoài PhươngNoch keine Bewertungen

- Caiib BFM Study Notes PDFDokument200 SeitenCaiib BFM Study Notes PDFRahul Pandey100% (1)

- Ani Dobanda/an Randament (%) Valoare Bani La Inceputul Anului Valoare Bani La Sfarsitul AnuluiDokument4 SeitenAni Dobanda/an Randament (%) Valoare Bani La Inceputul Anului Valoare Bani La Sfarsitul AnuluiAlexandru HalauNoch keine Bewertungen

- Jobsheet PMDokument49 SeitenJobsheet PMwindhy fitrianaNoch keine Bewertungen

- 3-Types of IndustriesDokument16 Seiten3-Types of Industriesbias si jakeNoch keine Bewertungen