Das könnte Ihnen auch gefallen

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementVon EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNoch keine Bewertungen

- Foreign Currency Exchangeable BondsDokument7 SeitenForeign Currency Exchangeable BondsDheeraj VijayNoch keine Bewertungen

- Foreign Currency Exchangeable BondsDokument2 SeitenForeign Currency Exchangeable BondsGovind RathiNoch keine Bewertungen

- Foreign Currency Convertible Bonds FinalDokument15 SeitenForeign Currency Convertible Bonds FinalGautam JainNoch keine Bewertungen

- Investment Law MarketingDokument6 SeitenInvestment Law MarketingJust RandomNoch keine Bewertungen

- What Is A Foreign Currency Convertible Bond (FCCB) ? A ForeignDokument9 SeitenWhat Is A Foreign Currency Convertible Bond (FCCB) ? A ForeignParas R AsharaNoch keine Bewertungen

- Convertible Notes Open Doors To Foreign Investments For StartupsDokument4 SeitenConvertible Notes Open Doors To Foreign Investments For StartupsFelix AdvisoryNoch keine Bewertungen

- FCCBDokument8 SeitenFCCBRadha RampalliNoch keine Bewertungen

- Powerpoint Presentation On FIIDokument13 SeitenPowerpoint Presentation On FIIManali Rana100% (1)

- Foreign Currency Convertible Bond 100 Marks ProjectDokument47 SeitenForeign Currency Convertible Bond 100 Marks ProjectSalman Corleone100% (1)

- Updates SMAIT June 2016Dokument11 SeitenUpdates SMAIT June 2016Harsh SharmaNoch keine Bewertungen

- Foreign Investment in IndiaDokument13 SeitenForeign Investment in Indiagolu1985Noch keine Bewertungen

- II Regulations in India:: Foreign Institutional Investors (FII's) SebiDokument17 SeitenII Regulations in India:: Foreign Institutional Investors (FII's) SebiKumar DayanidhiNoch keine Bewertungen

- Foreign Collaborations in IndiaDokument17 SeitenForeign Collaborations in IndiacagopalchaturvediNoch keine Bewertungen

- Investment Routes: India's Debt Markets, The Way Forward Available at Last Visited On 8 April, 2019Dokument3 SeitenInvestment Routes: India's Debt Markets, The Way Forward Available at Last Visited On 8 April, 2019Kunwar AbhudayNoch keine Bewertungen

- Debt Funding in India, Nishith Desai Associates, Available At, Last Visited On 8 April, 2019 External Commercial Borrowings & Trade Credits, Available at Last Visited On 9 April 2019Dokument3 SeitenDebt Funding in India, Nishith Desai Associates, Available At, Last Visited On 8 April, 2019 External Commercial Borrowings & Trade Credits, Available at Last Visited On 9 April 2019Kunwar AbhudayNoch keine Bewertungen

- Ecb and Trade CreditsDokument10 SeitenEcb and Trade CreditsVarun JainNoch keine Bewertungen

- FCCBDokument17 SeitenFCCBcoffytoffyNoch keine Bewertungen

- Role of Fii in Share MarketDokument7 SeitenRole of Fii in Share MarketMukesh Kumar MishraNoch keine Bewertungen

- The Role of FIIDokument3 SeitenThe Role of FIIkushalsaxenaNoch keine Bewertungen

- Sources of Foreign Financing or Foreign Currency Finance For Indian CompaniesDokument3 SeitenSources of Foreign Financing or Foreign Currency Finance For Indian Companiesarshad391Noch keine Bewertungen

- Deepanshu'sDokument5 SeitenDeepanshu'sdeepu0787Noch keine Bewertungen

- CA Final May'23 Amendment VfinalDokument18 SeitenCA Final May'23 Amendment VfinalPooja SurveNoch keine Bewertungen

- FCCB 1Dokument6 SeitenFCCB 1krishr25Noch keine Bewertungen

- Foreign Direct InvestmentDokument6 SeitenForeign Direct Investmentrohitalbert5Noch keine Bewertungen

- Indian Investment AbroadDokument17 SeitenIndian Investment Abroadapi-3716588Noch keine Bewertungen

- FCCB in IndiaDokument24 SeitenFCCB in IndiaSana Riyaz KhalifeNoch keine Bewertungen

- Startup Series 7 - Exchange Control Provisions For StartupsDokument12 SeitenStartup Series 7 - Exchange Control Provisions For StartupsRavi PatelNoch keine Bewertungen

- Capital Market Regulatory Insight - P.S.rao & AssociatesDokument43 SeitenCapital Market Regulatory Insight - P.S.rao & AssociatesSharath Srinivas Budugunte100% (1)

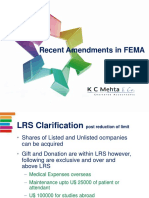

- Recent Amendments in FemaDokument14 SeitenRecent Amendments in FemaSarath Kumar Vijaya KumarNoch keine Bewertungen

- MM M M MMDokument17 SeitenMM M M MMDhiraj K DalalNoch keine Bewertungen

- FII Investment in IndiaDokument38 SeitenFII Investment in IndiaKhushbu GosherNoch keine Bewertungen

- Investment by The Foreign Institutional Investors: DR Sanjeev KumarDokument4 SeitenInvestment by The Foreign Institutional Investors: DR Sanjeev KumarDr. Mohammad Noor AlamNoch keine Bewertungen

- Join Caiib With Ashok On Youtube & App: BFM Module - ADokument34 SeitenJoin Caiib With Ashok On Youtube & App: BFM Module - ASamir BuddheNoch keine Bewertungen

- Foreign Currency Exchangeable BondsDokument5 SeitenForeign Currency Exchangeable BondsMitesh LadNoch keine Bewertungen

- QIPsDokument19 SeitenQIPsJyothsna RanganathNoch keine Bewertungen

- Overseas Direct InvestmentDokument61 SeitenOverseas Direct InvestmentSutonu BasuNoch keine Bewertungen

- International Business: Key Compliances in Investing AbroadDokument73 SeitenInternational Business: Key Compliances in Investing AbroadSunny KumarNoch keine Bewertungen

- 220ecb and Trade Credits1Dokument10 Seiten220ecb and Trade Credits1Mohd ParvezNoch keine Bewertungen

- Regulatory Provisions Under EcbDokument6 SeitenRegulatory Provisions Under EcbAllwyn FlowNoch keine Bewertungen

- Q&a FemaDokument7 SeitenQ&a FemaVijay MakhijaniNoch keine Bewertungen

- Foreign Instituitional InvestorsDokument8 SeitenForeign Instituitional InvestorsJayneel JadejaNoch keine Bewertungen

- External Commercial BorrowingDokument14 SeitenExternal Commercial BorrowingKK SinghNoch keine Bewertungen

- Fema Rbi Org inDokument11 SeitenFema Rbi Org inamishtheanalystNoch keine Bewertungen

- Mahindra & Mahindra Financial Services Limited Dividend Distribution PolicyDokument6 SeitenMahindra & Mahindra Financial Services Limited Dividend Distribution PolicyJuan Carlos CalderonNoch keine Bewertungen

- Private Equity StructureDokument14 SeitenPrivate Equity Structurewww.pubg3.co.inNoch keine Bewertungen

- Refresh Changing Regulatory Landscape July August 2014Dokument30 SeitenRefresh Changing Regulatory Landscape July August 2014Aayushi AroraNoch keine Bewertungen

- Public Issue and Listing of Non-Convertible Debt SecuritiesDokument1 SeitePublic Issue and Listing of Non-Convertible Debt SecuritiesKhushiNoch keine Bewertungen

- RBI FAQ of FDI in IndiaDokument53 SeitenRBI FAQ of FDI in Indiaaironderon1Noch keine Bewertungen

- Qualified Institutional Placement: Presented by - Sandeep Singh 09-II-247 Shyamu Pandey 09-II-250Dokument11 SeitenQualified Institutional Placement: Presented by - Sandeep Singh 09-II-247 Shyamu Pandey 09-II-250sandeep-bhatia-911Noch keine Bewertungen

- Non-Banking Financial Companies (NBFCS) FinalDokument29 SeitenNon-Banking Financial Companies (NBFCS) FinalAnsumanNathNoch keine Bewertungen

- Commercial PaperDokument15 SeitenCommercial PaperKrishna Chandran Pallippuram100% (1)

- By Geet Arora Bba 3 Year Roll No - 4204Dokument15 SeitenBy Geet Arora Bba 3 Year Roll No - 4204geet882004Noch keine Bewertungen

- 52MCC160107IDokument7 Seiten52MCC160107IPrasad NayakNoch keine Bewertungen

- External Commercial Borrowings (Ecbs)Dokument5 SeitenExternal Commercial Borrowings (Ecbs)Prateek MallNoch keine Bewertungen

- Ecb and Trade CreditDokument8 SeitenEcb and Trade CreditSatyanag VenishettyNoch keine Bewertungen

- Global Depository ReceiptsDokument4 SeitenGlobal Depository ReceiptsSaiyam ChaturvediNoch keine Bewertungen

- Foreign Investment Regime in IndiaDokument4 SeitenForeign Investment Regime in IndiaKriti KaushikNoch keine Bewertungen

- Private Equity 2015Dokument47 SeitenPrivate Equity 2015Apurva SoodNoch keine Bewertungen

- Summary (SDL: Continuing The Evolution)Dokument2 SeitenSummary (SDL: Continuing The Evolution)ahsanlone100% (2)

- The Consequences of Using Incorrect TerminologyDokument6 SeitenThe Consequences of Using Incorrect TerminologyPastor DavidNoch keine Bewertungen

- MA-2012-Nico Vriend Het Informatiesysteem en Netwerk Van de VOCDokument105 SeitenMA-2012-Nico Vriend Het Informatiesysteem en Netwerk Van de VOCPrisca RaniNoch keine Bewertungen

- Scraper SiteDokument3 SeitenScraper Sitelinda976Noch keine Bewertungen

- English (202) Tutor Marked Assignment: NoteDokument3 SeitenEnglish (202) Tutor Marked Assignment: NoteLubabath IsmailNoch keine Bewertungen

- PrecedentialDokument41 SeitenPrecedentialScribd Government DocsNoch keine Bewertungen

- Gladys Ruiz, ResumeDokument2 SeitenGladys Ruiz, Resumeapi-284904141Noch keine Bewertungen

- IBA High Frequency Words PDFDokument18 SeitenIBA High Frequency Words PDFReduanul Chowdhury NitulNoch keine Bewertungen

- SAHANA Disaster Management System and Tracking Disaster VictimsDokument30 SeitenSAHANA Disaster Management System and Tracking Disaster VictimsAmalkrishnaNoch keine Bewertungen

- Module 2Dokument6 SeitenModule 2MonicaMartirosyanNoch keine Bewertungen

- Chapter 6-Contracting PartiesDokument49 SeitenChapter 6-Contracting PartiesNUR AISYAH NABILA RASHIMYNoch keine Bewertungen

- Glossary of Fashion Terms: Powered by Mambo Generated: 7 October, 2009, 00:47Dokument4 SeitenGlossary of Fashion Terms: Powered by Mambo Generated: 7 October, 2009, 00:47Chetna Shetty DikkarNoch keine Bewertungen

- Bhagwanti's Resume (1) - 2Dokument1 SeiteBhagwanti's Resume (1) - 2muski rajputNoch keine Bewertungen

- Case Studies in Entrepreneurship-3MDokument3 SeitenCase Studies in Entrepreneurship-3MAshish ThakurNoch keine Bewertungen

- Philips AZ 100 B Service ManualDokument8 SeitenPhilips AZ 100 B Service ManualВладислав ПаршутінNoch keine Bewertungen

- Nittscher vs. NittscherDokument4 SeitenNittscher vs. NittscherKeej DalonosNoch keine Bewertungen

- Case Study No. 8-Managing Floods in Metro ManilaDokument22 SeitenCase Study No. 8-Managing Floods in Metro ManilapicefeatiNoch keine Bewertungen

- 6 Habits of True Strategic ThinkersDokument64 Seiten6 Habits of True Strategic ThinkersPraveen Kumar JhaNoch keine Bewertungen

- Carbon Pricing: State and Trends ofDokument74 SeitenCarbon Pricing: State and Trends ofdcc ccNoch keine Bewertungen

- Postgame Notes 0901 PDFDokument1 SeitePostgame Notes 0901 PDFRyan DivishNoch keine Bewertungen

- Ch02 Choice in World of ScarcityDokument14 SeitenCh02 Choice in World of ScarcitydankNoch keine Bewertungen

- Commercial Law 11 DR Caroline Mwaura NotesDokument16 SeitenCommercial Law 11 DR Caroline Mwaura NotesNaomi CampbellNoch keine Bewertungen

- AICPADokument5 SeitenAICPAMikaela SalvadorNoch keine Bewertungen

- Chapter 12 - Bank ReconciliationDokument29 SeitenChapter 12 - Bank Reconciliationshemida100% (7)

- Heat Resisting Steels and Nickel Alloys: British Standard Bs en 10095:1999Dokument30 SeitenHeat Resisting Steels and Nickel Alloys: British Standard Bs en 10095:1999amanduhqsmNoch keine Bewertungen

- Qualitative KPIDokument7 SeitenQualitative KPIMas AgusNoch keine Bewertungen

- Little White Book of Hilmy Cader's Wisdom Strategic Reflections at One's Fingertip!Dokument8 SeitenLittle White Book of Hilmy Cader's Wisdom Strategic Reflections at One's Fingertip!Thavam RatnaNoch keine Bewertungen

- Front Cover NME Music MagazineDokument5 SeitenFront Cover NME Music Magazineasmediae12Noch keine Bewertungen

- Retrato Alvin YapanDokument8 SeitenRetrato Alvin YapanAngel Jan AgpalzaNoch keine Bewertungen