Das könnte Ihnen auch gefallen

- Problems On Contract CostingDokument11 SeitenProblems On Contract CostingRoguewolfx VFX50% (2)

- Contarct CostingDokument13 SeitenContarct CostingBuddhadev NathNoch keine Bewertungen

- Contract Costing (Unsolved)Dokument6 SeitenContract Costing (Unsolved)ArnavNoch keine Bewertungen

- Group - I Paper - 1 Accounting V2 Chapter 13 PDFDokument13 SeitenGroup - I Paper - 1 Accounting V2 Chapter 13 PDFjashveer rekhiNoch keine Bewertungen

- Chapter 11 Hire Purchase and Instalment Sale Transactions PDFDokument52 SeitenChapter 11 Hire Purchase and Instalment Sale Transactions PDFEswari GkNoch keine Bewertungen

- Cost Acc Nov06Dokument27 SeitenCost Acc Nov06api-3825774100% (1)

- Chapter 22 Contract Costing - NoRestrictionDokument18 SeitenChapter 22 Contract Costing - NoRestrictionMohammad SaadmanNoch keine Bewertungen

- Branch AccountsDokument12 SeitenBranch AccountsRobert Henson100% (1)

- Royalty AccountsDokument5 SeitenRoyalty AccountsRobert Henson100% (2)

- Hire Purchase Notes 10 YrDokument80 SeitenHire Purchase Notes 10 YrLalitKukreja100% (2)

- Job CostingDokument18 SeitenJob CostingBiswajeet DashNoch keine Bewertungen

- Cost Sheet ProblemsDokument2 SeitenCost Sheet ProblemsPridhvi Raj ReddyNoch keine Bewertungen

- 02 Per. Invest 26-30Dokument5 Seiten02 Per. Invest 26-30Ritu SahaniNoch keine Bewertungen

- Specimen of Cost Sheet and Problems-Unit-1 Cost SheetDokument11 SeitenSpecimen of Cost Sheet and Problems-Unit-1 Cost SheetRavi shankar100% (1)

- Cost Sheet - Pages 16Dokument16 SeitenCost Sheet - Pages 16omikron omNoch keine Bewertungen

- Chapter 8 Operating CostingDokument13 SeitenChapter 8 Operating CostingDerrick LewisNoch keine Bewertungen

- As-2 Inventory Valuation: 1) IntroductionDokument17 SeitenAs-2 Inventory Valuation: 1) IntroductionDipen AdhikariNoch keine Bewertungen

- 7948final Adv Acc Nov05Dokument16 Seiten7948final Adv Acc Nov05Kushan MistryNoch keine Bewertungen

- Study Note 4.3, Page 198-263Dokument66 SeitenStudy Note 4.3, Page 198-263s4sahithNoch keine Bewertungen

- Royalty AccountsDokument11 SeitenRoyalty AccountsVipin Mandyam Kadubi0% (1)

- Chapter 2 Hire Purchase & Installment SystemDokument26 SeitenChapter 2 Hire Purchase & Installment SystemSuku Thomas Samuel100% (1)

- Hire Purchase Short NotesDokument26 SeitenHire Purchase Short NotesULTIMATE FACTS HINDINoch keine Bewertungen

- 5 6084915055709651012Dokument8 Seiten5 6084915055709651012Ajit Yadav100% (1)

- Operating Costing - Pages 32Dokument32 SeitenOperating Costing - Pages 32omikron omNoch keine Bewertungen

- Revision Test Paper: Cap-Ii: Advanced Accounting: QuestionsDokument158 SeitenRevision Test Paper: Cap-Ii: Advanced Accounting: Questionsshankar k.c.Noch keine Bewertungen

- 13 17227rtp Ipcc Nov09 Paper3aDokument24 Seiten13 17227rtp Ipcc Nov09 Paper3aemmanuel JohnyNoch keine Bewertungen

- Branch AccountsDokument57 SeitenBranch Accountsasadqhse50% (2)

- Costing AssignmentDokument15 SeitenCosting AssignmentSumit SumanNoch keine Bewertungen

- Income From House PropertyDokument26 SeitenIncome From House PropertySuyash Patwa100% (1)

- Foreign Currency QuestionsDokument2 SeitenForeign Currency QuestionsAbhijeetNoch keine Bewertungen

- Cost Sheet PDF - 20210623 - 142101Dokument10 SeitenCost Sheet PDF - 20210623 - 142101Raju Lal100% (1)

- Fin Account-Sole Trading AnswersDokument10 SeitenFin Account-Sole Trading AnswersAR Ananth Rohith BhatNoch keine Bewertungen

- Income From Other Sources IllustrationDokument5 SeitenIncome From Other Sources IllustrationSarvar PathanNoch keine Bewertungen

- Study Note 3, Page 114-142Dokument29 SeitenStudy Note 3, Page 114-142s4sahithNoch keine Bewertungen

- Capinew Account June13Dokument7 SeitenCapinew Account June13ashwinNoch keine Bewertungen

- Coc Departmental Accounting Ca/Cma Santosh KumarDokument11 SeitenCoc Departmental Accounting Ca/Cma Santosh KumarAyush AcharyaNoch keine Bewertungen

- 5 6168179598107345065Dokument14 Seiten5 6168179598107345065Madhan Aadhvick0% (1)

- 19732ipcc CA Vol2 Cp3Dokument43 Seiten19732ipcc CA Vol2 Cp3PALADUGU MOUNIKANoch keine Bewertungen

- Chapter 9 Accounting For Branches Including Foreign Branches PDFDokument61 SeitenChapter 9 Accounting For Branches Including Foreign Branches PDFAkshansh MahajanNoch keine Bewertungen

- 6 - As-16 Borrowing CostsDokument15 Seiten6 - As-16 Borrowing CostsKrishna JhaNoch keine Bewertungen

- Unit - V Budget and Budgetary Control ProblemsDokument2 SeitenUnit - V Budget and Budgetary Control ProblemsalexanderNoch keine Bewertungen

- 18 Chapter4 Unit 1 2 Hire Purchase and Instalment PaymentDokument17 Seiten18 Chapter4 Unit 1 2 Hire Purchase and Instalment Paymentnarasimha_gudiNoch keine Bewertungen

- Chapter 12 Service CostingDokument3 SeitenChapter 12 Service CostingMS Raju100% (1)

- Course Name: 2T7 - Cost AccountingDokument56 SeitenCourse Name: 2T7 - Cost Accountingjhggd100% (1)

- UNIT 3 Income From House PropertyDokument104 SeitenUNIT 3 Income From House Propertydob BoysNoch keine Bewertungen

- Business & Profession Q - A 02.9.2020Dokument42 SeitenBusiness & Profession Q - A 02.9.2020shyamiliNoch keine Bewertungen

- Hire PurchaseDokument6 SeitenHire PurchaseGanesh Bokkisam100% (1)

- 6 - COMPUTATION OF TAXABLE VALUE - Q - As - AFTER SESSION - 9Dokument21 Seiten6 - COMPUTATION OF TAXABLE VALUE - Q - As - AFTER SESSION - 9Mighty SinghNoch keine Bewertungen

- Chapter 7 - Value of Supply - NotesDokument16 SeitenChapter 7 - Value of Supply - NotesPuran GuptaNoch keine Bewertungen

- Problems On Taxable Salary Income Additional PDFDokument24 SeitenProblems On Taxable Salary Income Additional PDFNALIN MEHTA 1713068Noch keine Bewertungen

- 12 Accountancy sp04Dokument45 Seiten12 Accountancy sp04Priyansh AryaNoch keine Bewertungen

- Consignment - SolutionDokument18 SeitenConsignment - Solution203 596 Reuben RoyNoch keine Bewertungen

- Chapter 9 Accounting For Branches Including Foreign Branches PMDokument48 SeitenChapter 9 Accounting For Branches Including Foreign Branches PMviji88mba60% (5)

- 3 Pre - PostDokument7 Seiten3 Pre - PostParul Bhardwaj VaidyaNoch keine Bewertungen

- Cost Sheet Practical ProblemsDokument2 SeitenCost Sheet Practical Problemssameer_kini100% (1)

- Cost Sheet Practical ProblemsDokument2 SeitenCost Sheet Practical Problemssameer_kiniNoch keine Bewertungen

- Capital Gain Sums With SolutionDokument10 SeitenCapital Gain Sums With Solutionkomil bogharaNoch keine Bewertungen

- Contract CostingDokument12 SeitenContract Costingvivek rajakNoch keine Bewertungen

- Contract Costing - Practise ProblemsDokument3 SeitenContract Costing - Practise ProblemsMadhavasadasivan Pothiyil50% (2)

- IFRS 15 Q and ADokument27 SeitenIFRS 15 Q and AaliNoch keine Bewertungen

- New Issues SEBI GuidelineDokument55 SeitenNew Issues SEBI Guidelineapi-3701467100% (1)

- Suitability, BenefitsDokument2 SeitenSuitability, BenefitsFreddy Savio D'souzaNoch keine Bewertungen

- Keyman Insurance New InfoDokument10 SeitenKeyman Insurance New InfoFreddy Savio D'souzaNoch keine Bewertungen

- 3G Technology and INDIADokument21 Seiten3G Technology and INDIAFreddy Savio D'souzaNoch keine Bewertungen

- Maximum Management Review Front PageDokument1 SeiteMaximum Management Review Front PageFreddy Savio D'souzaNoch keine Bewertungen

- Asgnmnt 1 - Q PAPER1Dokument11 SeitenAsgnmnt 1 - Q PAPER1Freddy Savio D'souzaNoch keine Bewertungen

- Reference Books: Introduction To Life Insurance Basics of Life Insurance Principles of Life InsuranceDokument10 SeitenReference Books: Introduction To Life Insurance Basics of Life Insurance Principles of Life InsuranceFreddy Savio D'souzaNoch keine Bewertungen

- Life InsuranceDokument2 SeitenLife InsuranceFreddy Savio D'souzaNoch keine Bewertungen

- BM Asgnmnt Q1Dokument7 SeitenBM Asgnmnt Q1Freddy Savio D'souzaNoch keine Bewertungen

- Final KMI ChaptersDokument57 SeitenFinal KMI ChaptersFreddy Savio D'souzaNoch keine Bewertungen

- Keyman InfoDokument15 SeitenKeyman InfoFreddy Savio D'souzaNoch keine Bewertungen

- Keyman Info 2Dokument17 SeitenKeyman Info 2Freddy Savio D'souzaNoch keine Bewertungen

- Key ManDokument7 SeitenKey ManFreddy Savio D'souzaNoch keine Bewertungen

- "Potential of Life Insurance Industry in Surat Market": Under The Guidance ofDokument51 Seiten"Potential of Life Insurance Industry in Surat Market": Under The Guidance ofFreddy Savio D'souzaNoch keine Bewertungen

- Keyman Insurance New Info2Dokument3 SeitenKeyman Insurance New Info2Freddy Savio D'souzaNoch keine Bewertungen

- Handling The Day-To-Day Operations.: What Can The Money Be Used ForDokument13 SeitenHandling The Day-To-Day Operations.: What Can The Money Be Used ForFreddy Savio D'souzaNoch keine Bewertungen

- Basic Principles of Life InsuranceDokument44 SeitenBasic Principles of Life InsuranceAlanNoch keine Bewertungen

- Case Study-Misrepresentation by Life InsuredDokument3 SeitenCase Study-Misrepresentation by Life InsuredFreddy Savio D'souzaNoch keine Bewertungen

- EIFM Tutorial 3Dokument2 SeitenEIFM Tutorial 3Chi YenNoch keine Bewertungen

- 0504 PDFDokument22 Seiten0504 PDFAnonymous VwHMX3ZNoch keine Bewertungen

- Cost of Equity Risk Free Rate of Return + Beta × (Market Rate of Return - Risk Free Rate of Return)Dokument7 SeitenCost of Equity Risk Free Rate of Return + Beta × (Market Rate of Return - Risk Free Rate of Return)chatterjee rikNoch keine Bewertungen

- Working Capital Estimation ProblemsDokument3 SeitenWorking Capital Estimation ProblemsBunny MathaiNoch keine Bewertungen

- AE 25 Module 1 Lesson 1Dokument99 SeitenAE 25 Module 1 Lesson 1Queeny Mae Cantre ReutaNoch keine Bewertungen

- Contract of LeaseDokument2 SeitenContract of LeaseElain OrtizNoch keine Bewertungen

- eDocumentFile 2Dokument2 SeiteneDocumentFile 29z8925bxm8Noch keine Bewertungen

- FNCE3000-Group Assignment-WilliamWhiteford, NivPatel PDFDokument20 SeitenFNCE3000-Group Assignment-WilliamWhiteford, NivPatel PDFNiv PatelNoch keine Bewertungen

- Chapter 17Dokument3 SeitenChapter 17Juan Rafael FernandezNoch keine Bewertungen

- Vardhan Consulting Finance Internship Task 1Dokument6 SeitenVardhan Consulting Finance Internship Task 1Ravi KapoorNoch keine Bewertungen

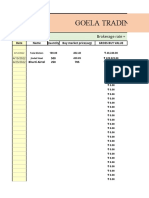

- Goela Trading JournalDokument621 SeitenGoela Trading JournalrohankananiNoch keine Bewertungen

- Basel III and Its Implications On Banking SectorDokument56 SeitenBasel III and Its Implications On Banking Sectoradityavikram009Noch keine Bewertungen

- Ias 16 Property Plant and Equipment SummaryDokument8 SeitenIas 16 Property Plant and Equipment SummaryFelice FeliceNoch keine Bewertungen

- Market Analysis - CourseworkThe Competitive Advantage of FinlandDokument10 SeitenMarket Analysis - CourseworkThe Competitive Advantage of FinlandscrimaniaNoch keine Bewertungen

- BEGP2 OutDokument28 SeitenBEGP2 OutSainadha Reddy PonnapureddyNoch keine Bewertungen

- List of Preference Shares 27.11.20Dokument360 SeitenList of Preference Shares 27.11.20kishoreNoch keine Bewertungen

- Banking On Big Data - A Case Study PDFDokument4 SeitenBanking On Big Data - A Case Study PDFMuthiani MuokaNoch keine Bewertungen

- 8th ATMA by Dalta Rsi - AnalysisDokument44 Seiten8th ATMA by Dalta Rsi - Analysissuresh100% (2)

- Inventory Cost Flow Biological AssetsDokument7 SeitenInventory Cost Flow Biological Assetsemman neriNoch keine Bewertungen

- Major Assignment - FM303 PDFDokument5 SeitenMajor Assignment - FM303 PDFfrancisNoch keine Bewertungen

- Castillo V PascoDokument2 SeitenCastillo V PascoSui50% (2)

- Case Study Finding WACC For A Project BoltaDokument1 SeiteCase Study Finding WACC For A Project BoltaebeNoch keine Bewertungen

- Form 3Dokument6 SeitenForm 3ShyamgNoch keine Bewertungen

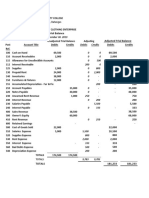

- Horizontal Balance Sheet: Total Equity&LiabilitiesDokument7 SeitenHorizontal Balance Sheet: Total Equity&LiabilitiesM.TalhaNoch keine Bewertungen

- Public Procurement Rules 2004Dokument19 SeitenPublic Procurement Rules 2004Hafiz MehmoodNoch keine Bewertungen

- Ch14 - Audit ReportsDokument25 SeitenCh14 - Audit ReportsShinny Lee G. UlaNoch keine Bewertungen

- RAYMONDSDokument1 SeiteRAYMONDSsalman KhanNoch keine Bewertungen

- Banking Notes BBA PDFDokument19 SeitenBanking Notes BBA PDFSekar Murugan50% (2)

- The Nigerian Tourism Sector and The Impact of Fiscal PolicyDokument73 SeitenThe Nigerian Tourism Sector and The Impact of Fiscal PolicyAttah Andung PeterNoch keine Bewertungen

- Ia MidtermDokument5 SeitenIa MidtermCindy CrausNoch keine Bewertungen