Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Modern Legal DraftingDokument274 SeitenModern Legal DraftingVishal Jain100% (12)

- Chapter 1 - Introduction To Food MarketingDokument42 SeitenChapter 1 - Introduction To Food MarketingMong Titya79% (14)

- Prospecting GuideDokument16 SeitenProspecting Guideabsolutemax100% (5)

- Supply and DemandDokument9 SeitenSupply and DemandHeather SandersNoch keine Bewertungen

- ASPAC Indirect Tax Guide 2013Dokument60 SeitenASPAC Indirect Tax Guide 2013culpable2Noch keine Bewertungen

- Web FareDokument24 SeitenWeb Fareesjey3900Noch keine Bewertungen

- R&D Roadmap Blast FurnaceDokument37 SeitenR&D Roadmap Blast FurnaceVishal JainNoch keine Bewertungen

- Real EstateDokument398 SeitenReal EstateVishal Jain100% (1)

- CA Ethics PlusDokument16 SeitenCA Ethics PlusVishal JainNoch keine Bewertungen

- Asean Tax GuideDokument92 SeitenAsean Tax GuideVishal JainNoch keine Bewertungen

- VV IMP File of Codes by RBI - Sectrol & Region WiseDokument60 SeitenVV IMP File of Codes by RBI - Sectrol & Region WiseVishal JainNoch keine Bewertungen

- List of Service Units Eligible For VAT Loan - DICDokument1 SeiteList of Service Units Eligible For VAT Loan - DICVishal JainNoch keine Bewertungen

- 21 Labour Laws ChartDokument17 Seiten21 Labour Laws ChartVishal JainNoch keine Bewertungen

- Tax Alert SEZ-1Dokument2 SeitenTax Alert SEZ-1Vishal JainNoch keine Bewertungen

- FINAL Tax Alert April 2014 MyanmarDokument3 SeitenFINAL Tax Alert April 2014 MyanmarVishal JainNoch keine Bewertungen

- Myanmar Tax GuideDokument12 SeitenMyanmar Tax GuideVenkatesh GorurNoch keine Bewertungen

- Asean Tax GuideDokument92 SeitenAsean Tax GuideVishal JainNoch keine Bewertungen

- Roller Flour Mill Project in MP for Grain ProcessingDokument5 SeitenRoller Flour Mill Project in MP for Grain ProcessingAlisha Kothari100% (1)

- Roller Flour Mill Project in MP for Grain ProcessingDokument5 SeitenRoller Flour Mill Project in MP for Grain ProcessingAlisha Kothari100% (1)

- Khyati Tor PresnetationDokument20 SeitenKhyati Tor PresnetationVishal JainNoch keine Bewertungen

- Auditing Revenue Process & Accounts ReceivableDokument17 SeitenAuditing Revenue Process & Accounts ReceivableDaniel TadejaNoch keine Bewertungen

- Pulp & Paper Industry Process Flow Data SheetsDokument26 SeitenPulp & Paper Industry Process Flow Data SheetsJaime Zea100% (1)

- Baby Food Production ProfileDokument14 SeitenBaby Food Production Profileuegagod100% (1)

- BiscuitDokument16 SeitenBiscuitVishal JainNoch keine Bewertungen

- Cattle Feed Manf. PlantDokument15 SeitenCattle Feed Manf. PlantVishal JainNoch keine Bewertungen

- Travelling ExpenseDokument1 SeiteTravelling ExpenseVishal JainNoch keine Bewertungen

- Apricot Juice and SyrupDokument17 SeitenApricot Juice and SyrupVishal JainNoch keine Bewertungen

- Checklist For Statutory AuditDokument66 SeitenChecklist For Statutory Auditsmartmanpratik100% (1)

- Hotel Industries An OverviewDokument36 SeitenHotel Industries An OverviewVishal Jain100% (1)

- Apple Juice and SyrupDokument18 SeitenApple Juice and SyrupVishal JainNoch keine Bewertungen

- Audit Process / Procedure / Checklist: Page 1 of 3Dokument3 SeitenAudit Process / Procedure / Checklist: Page 1 of 3Vishal JainNoch keine Bewertungen

- 9 Assessment ProcedureDokument5 Seiten9 Assessment ProcedureHarry Singh ButtarNoch keine Bewertungen

- Audit ReqDokument367 SeitenAudit ReqVishal JainNoch keine Bewertungen

- Business Plan for C2R Research Project FundingDokument42 SeitenBusiness Plan for C2R Research Project FundingMuhammad FadhlullahNoch keine Bewertungen

- Exam Prep Short Answer QuestionsDokument16 SeitenExam Prep Short Answer Questionsطه احمدNoch keine Bewertungen

- Lesson 3 - TAX Its Characteristics and ClassificationDokument18 SeitenLesson 3 - TAX Its Characteristics and ClassificationAbigail MangaoangNoch keine Bewertungen

- E Jeep Co.: Electronic Jeepney CorporationDokument30 SeitenE Jeep Co.: Electronic Jeepney CorporationAshyyy123 GomezNoch keine Bewertungen

- Marketing of ServicesDokument8 SeitenMarketing of ServicesShreya GoyalNoch keine Bewertungen

- Joshua Kennon What Is A FranchiseDokument6 SeitenJoshua Kennon What Is A FranchiseNico A. Cotzias Jr.Noch keine Bewertungen

- Impact of Globalization on International BusinessesDokument21 SeitenImpact of Globalization on International BusinessesNishtha ShaktawatNoch keine Bewertungen

- Mission of Dell CompanyDokument40 SeitenMission of Dell Companyxyz skillNoch keine Bewertungen

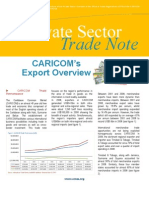

- OTN - Private Sector Trade Note - Vol 16 2010Dokument4 SeitenOTN - Private Sector Trade Note - Vol 16 2010Office of Trade Negotiations (OTN), CARICOM SecretariatNoch keine Bewertungen

- Aznar v. YapdiangcoDokument3 SeitenAznar v. YapdiangcoKps12Noch keine Bewertungen

- Market Structure Original Unit 3Dokument32 SeitenMarket Structure Original Unit 3Priya SonuNoch keine Bewertungen

- SCL - I. Letters of CreditDokument5 SeitenSCL - I. Letters of CreditlealdeosaNoch keine Bewertungen

- FINAL PROJECT Outlook - PrateekDokument57 SeitenFINAL PROJECT Outlook - PrateekPrateek MendirattaNoch keine Bewertungen

- Equiteq Data Analytics Consulting Ma Report 2019 Full ReportDokument14 SeitenEquiteq Data Analytics Consulting Ma Report 2019 Full ReportanaNoch keine Bewertungen

- GST CompDokument14 SeitenGST CompNeerav DoshiNoch keine Bewertungen

- Gasbill 7849961000 202307 20230726135704Dokument1 SeiteGasbill 7849961000 202307 20230726135704AaFi SoomroNoch keine Bewertungen

- Osbert Oglesby Case StudyDokument48 SeitenOsbert Oglesby Case Studymallikarjun BandaNoch keine Bewertungen

- Resume 1Dokument2 SeitenResume 1api-298164137Noch keine Bewertungen

- Sap Retail Two Step PricingDokument4 SeitenSap Retail Two Step PricingShams TabrezNoch keine Bewertungen

- Business 1 Marketing 1168933Dokument10 SeitenBusiness 1 Marketing 1168933Ravi KumawatNoch keine Bewertungen

- Tagatac Vs Jimenez To EDCA Vs SantosDokument2 SeitenTagatac Vs Jimenez To EDCA Vs SantosMariaAyraCelinaBatacan100% (1)

- Frooti CaseDokument4 SeitenFrooti Caseakankshachauhan29100% (2)

- Business Plan EntrepDokument13 SeitenBusiness Plan EntrepKim VillanuevaNoch keine Bewertungen

- Customer Perception Towards Bajaj's VehiclesDokument85 SeitenCustomer Perception Towards Bajaj's VehiclesЯoнiт Яagнavaи100% (1)

- SDMDokument19 SeitenSDMNakul PatelNoch keine Bewertungen

- GrammarDokument70 SeitenGrammarManjuNoch keine Bewertungen

- Name: Zubash Durrani Class: Bba 2 Roll #: 43 Subject: Economics Submmited To: Maam KhatibaDokument7 SeitenName: Zubash Durrani Class: Bba 2 Roll #: 43 Subject: Economics Submmited To: Maam KhatibaAash KhanNoch keine Bewertungen