Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Mcq-For-Sdm - 2Dokument52 SeitenMcq-For-Sdm - 2jaitripathi2667% (3)

- Hindle Dar Es Salaam 20 Sept 2013, PaperDokument8 SeitenHindle Dar Es Salaam 20 Sept 2013, PaperFrank Victor MushiNoch keine Bewertungen

- Hotel Service Quality: The Impact of Service Quality On Customer Satisfaction in HospitalityDokument16 SeitenHotel Service Quality: The Impact of Service Quality On Customer Satisfaction in HospitalityDenray Responde100% (1)

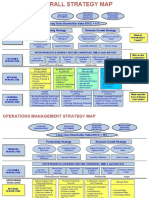

- Long-Term Shareholder Value ROCE 15% Productivity Strategy Revenue Growth StrategyDokument7 SeitenLong-Term Shareholder Value ROCE 15% Productivity Strategy Revenue Growth StrategyKamarulzaman Darus100% (2)

- ACC 121 - Chapter 2Dokument15 SeitenACC 121 - Chapter 2Rose Ann LazatinNoch keine Bewertungen

- GatnauVera Cornell 0058O 10991Dokument84 SeitenGatnauVera Cornell 0058O 10991Gorbi RrrrNoch keine Bewertungen

- Customer Satisfaction in BankDokument86 SeitenCustomer Satisfaction in Bankshreya shresthaNoch keine Bewertungen

- Filipino Style Sushi: The Business Concept and The Business ModelDokument5 SeitenFilipino Style Sushi: The Business Concept and The Business ModelkathleenNoch keine Bewertungen

- Service Delivery and Customer Satifaction by KENEAN BEDANEDokument75 SeitenService Delivery and Customer Satifaction by KENEAN BEDANEKENE AN100% (1)

- Khatabook Vs RazorpayDokument4 SeitenKhatabook Vs RazorpayRyan SequeiraNoch keine Bewertungen

- A Study On Customer Satisfaction Towards Samsung Smartphone With Special Reference To Chengalpattu DistrictDokument8 SeitenA Study On Customer Satisfaction Towards Samsung Smartphone With Special Reference To Chengalpattu DistrictJayaram JaiNoch keine Bewertungen

- CRM S1Dokument197 SeitenCRM S1spam ashishNoch keine Bewertungen

- Chapter 15 Improving Service Quality and ProductivityDokument24 SeitenChapter 15 Improving Service Quality and ProductivityKaalaivaani Narayanan50% (2)

- Literature ReviewDokument25 SeitenLiterature ReviewAravinth PrakashNoch keine Bewertungen

- Samad A. Hadji Madid - Case Study HHDokument3 SeitenSamad A. Hadji Madid - Case Study HHSamkol AragasíNoch keine Bewertungen

- SHS Abm GR11 PM Q1 M1 Marketing-Principles-And-Strategies FinalDokument28 SeitenSHS Abm GR11 PM Q1 M1 Marketing-Principles-And-Strategies FinalLee Arne BarayugaNoch keine Bewertungen

- BBM NotesDokument47 SeitenBBM NotesPraise Worthy100% (1)

- Deloitte Managed Analytics (DMA) Application CatalogDokument33 SeitenDeloitte Managed Analytics (DMA) Application CatalogDeloitte Analytics100% (3)

- TH4051Dokument118 SeitenTH4051gishan gamageNoch keine Bewertungen

- Customer Satisfaction For ISO 9001 - 2015 With ExamplesDokument5 SeitenCustomer Satisfaction For ISO 9001 - 2015 With ExamplesSudheer23984Noch keine Bewertungen

- Food QualityDokument2 SeitenFood QualityKida GoombaNoch keine Bewertungen

- Supply Chain ManagementDokument22 SeitenSupply Chain ManagementMario SubašićNoch keine Bewertungen

- Group6 SO Project StarbucksDokument6 SeitenGroup6 SO Project StarbucksAnkit VarshneyNoch keine Bewertungen

- Costumer Satisfaction Towards Nike and AdidasDokument60 SeitenCostumer Satisfaction Towards Nike and Adidasanuja_solanki890350% (2)

- Marketing Research Customer Satisfaction of The City Bank LTDDokument5 SeitenMarketing Research Customer Satisfaction of The City Bank LTDMd.Rakibuzzaman ShishirNoch keine Bewertungen

- Umbrex Sales Operations Diagnostic GuideDokument47 SeitenUmbrex Sales Operations Diagnostic GuideJoshuaNoch keine Bewertungen

- Study of Consumer Buying Behaviour Towards A New Product in Modern Trade"Dokument42 SeitenStudy of Consumer Buying Behaviour Towards A New Product in Modern Trade"shubham mahawarNoch keine Bewertungen

- Bba Final Year ProjectDokument57 SeitenBba Final Year Projectanitika74% (39)

- A Multidimensional Scale Measuring Theme Park PerformanceDokument17 SeitenA Multidimensional Scale Measuring Theme Park PerformanceiraniansmallbusinessNoch keine Bewertungen

- Union Bank of IndiaDokument58 SeitenUnion Bank of IndiaRakesh Prabhakar ShrivastavaNoch keine Bewertungen