Das könnte Ihnen auch gefallen

- Australian Housing Chartbook July 2012Dokument13 SeitenAustralian Housing Chartbook July 2012scribdooNoch keine Bewertungen

- Credit COnditions of The EconomyDokument4 SeitenCredit COnditions of The EconomyLigaya ValmonteNoch keine Bewertungen

- RBNZ Perspectives On Housing (April 2013)Dokument12 SeitenRBNZ Perspectives On Housing (April 2013)leithvanonselenNoch keine Bewertungen

- The Dinkum Index - Q211Dokument13 SeitenThe Dinkum Index - Q211economicdelusionNoch keine Bewertungen

- Strategy Radar - 2012 - 1005 XX Peak CarDokument3 SeitenStrategy Radar - 2012 - 1005 XX Peak CarStrategicInnovationNoch keine Bewertungen

- Property Report MelbourneDokument0 SeitenProperty Report MelbourneMichael JordanNoch keine Bewertungen

- 2008 CrisisDokument10 Seiten2008 Crisisaleezeazhar92Noch keine Bewertungen

- Worst Yet To ComeDokument13 SeitenWorst Yet To ComesmcjgNoch keine Bewertungen

- 2013 March 27 NZ Outlook Housing and InflationDokument3 Seiten2013 March 27 NZ Outlook Housing and InflationjomanousNoch keine Bewertungen

- Australian Interest Rates - OI #33 2012Dokument2 SeitenAustralian Interest Rates - OI #33 2012anon_370534332Noch keine Bewertungen

- ANZ Property Industry Confidence Survey December 2013Dokument7 SeitenANZ Property Industry Confidence Survey December 2013leithvanonselenNoch keine Bewertungen

- Subprime Mortgage CrisisDokument82 SeitenSubprime Mortgage Crisisbrian3442Noch keine Bewertungen

- Financial Crisis of 2007Dokument27 SeitenFinancial Crisis of 2007Houssem Eddine BoumallougaNoch keine Bewertungen

- Financial Crisis of 2007-2010Dokument30 SeitenFinancial Crisis of 2007-2010Haris AzizNoch keine Bewertungen

- Personal Finance 101 Canada’S Housing Market Analysis Buying Vs Renting a Home: A Case StudyVon EverandPersonal Finance 101 Canada’S Housing Market Analysis Buying Vs Renting a Home: A Case StudyNoch keine Bewertungen

- Nomura Special HousingDokument7 SeitenNomura Special Housingjanos_torok_4Noch keine Bewertungen

- February Housing FinanceDokument7 SeitenFebruary Housing FinanceBelinda WinkelmanNoch keine Bewertungen

- Housing Snapshot - October 2011Dokument11 SeitenHousing Snapshot - October 2011economicdelusionNoch keine Bewertungen

- Global Financial Crisis During 2008-2010Dokument12 SeitenGlobal Financial Crisis During 2008-2010Mega Pop LockerNoch keine Bewertungen

- Ric Battellino: Some Observations On Financial TrendsDokument11 SeitenRic Battellino: Some Observations On Financial Trendspeter_martin9335Noch keine Bewertungen

- Exhibit 1: House Price ChangeDokument7 SeitenExhibit 1: House Price ChangeSudhir PrajapatiNoch keine Bewertungen

- Australian Interest Rate SwaptionsDokument4 SeitenAustralian Interest Rate SwaptionsOMiNYCNoch keine Bewertungen

- ANZ Economics Toolbox 20111507Dokument14 SeitenANZ Economics Toolbox 20111507Khoa TranNoch keine Bewertungen

- Chap 9 NDokument19 SeitenChap 9 NMohammadTabbalNoch keine Bewertungen

- BIS Shrapnel OutlookDokument64 SeitenBIS Shrapnel OutlookshengizNoch keine Bewertungen

- Onsumer Atch Anada: Canadian Housing Prices - Beware of The AverageDokument4 SeitenOnsumer Atch Anada: Canadian Housing Prices - Beware of The AverageSteve LadurantayeNoch keine Bewertungen

- Global Economic Crisis 2008Dokument9 SeitenGlobal Economic Crisis 2008madhav KaushalNoch keine Bewertungen

- US Subprime Mortgage CrisisDokument23 SeitenUS Subprime Mortgage Crisiskid.hahn100% (1)

- Global Economic Crisis 2008Dokument9 SeitenGlobal Economic Crisis 2008madhav KaushalNoch keine Bewertungen

- Accounts ProjectDokument28 SeitenAccounts Projectsakshi14991Noch keine Bewertungen

- Housing Market HeadwindsDokument5 SeitenHousing Market Headwindsea12345Noch keine Bewertungen

- AIA Quarterly Investment InsightsDokument10 SeitenAIA Quarterly Investment InsightsdesmondNoch keine Bewertungen

- Ebook - Ebfl20121019part5Dokument0 SeitenEbook - Ebfl20121019part5Teresa WalterNoch keine Bewertungen

- Real Estate Built To WithstandDokument6 SeitenReal Estate Built To WithstandNephenteNoch keine Bewertungen

- 49 - Moody's Analytics-StressTesting Australias Housing Market Mar2014Dokument17 Seiten49 - Moody's Analytics-StressTesting Australias Housing Market Mar2014girishrajsNoch keine Bewertungen

- Imla The New Normalprospects For 2020 and 2021 1Dokument25 SeitenImla The New Normalprospects For 2020 and 2021 1Aminul IslamNoch keine Bewertungen

- A View On Banks FinalDokument22 SeitenA View On Banks FinaljustinsofoNoch keine Bewertungen

- Performing Credit Quarterly 3q2022Dokument22 SeitenPerforming Credit Quarterly 3q2022Kaida TeyNoch keine Bewertungen

- Aust House Prices OI 21 2012Dokument2 SeitenAust House Prices OI 21 2012TihoNoch keine Bewertungen

- Household Debt - Final Dec 13,2018Dokument3 SeitenHousehold Debt - Final Dec 13,2018The Hamilton SpectatorNoch keine Bewertungen

- Napier University MSC Accounting and Finance Module - Finance ManagementDokument13 SeitenNapier University MSC Accounting and Finance Module - Finance ManagementDharmesh PrajapatiNoch keine Bewertungen

- Westpac - Where Have The FHBs Gone (August 2013)Dokument6 SeitenWestpac - Where Have The FHBs Gone (August 2013)leithvanonselenNoch keine Bewertungen

- Subprime Mortgage CrisisDokument41 SeitenSubprime Mortgage CrisisRinkesh ShrishrimalNoch keine Bewertungen

- Alan Greenspan: Understanding Household Debt Obligations: Introduction: Credit Unions and Consumer LendingDokument3 SeitenAlan Greenspan: Understanding Household Debt Obligations: Introduction: Credit Unions and Consumer LendingMarianinaTrandafirNoch keine Bewertungen

- er20130211BullAusHousingfinanceDec12 PDFDokument3 Seitener20130211BullAusHousingfinanceDec12 PDFAmanda MooreNoch keine Bewertungen

- Real Estate Outlook Global Edition March 2023Dokument6 SeitenReal Estate Outlook Global Edition March 2023Saif MonajedNoch keine Bewertungen

- Australia (Commonwealth Of) : Major Rating Factors Rationale Outlook Related Criteria and ResearchDokument7 SeitenAustralia (Commonwealth Of) : Major Rating Factors Rationale Outlook Related Criteria and Researchapi-124274003Noch keine Bewertungen

- Article On Bond Yields 26 March 2015Dokument4 SeitenArticle On Bond Yields 26 March 2015mitul tamakuwalaNoch keine Bewertungen

- EY Could Uncertainty Be Your Best Opportunity For GrowthDokument6 SeitenEY Could Uncertainty Be Your Best Opportunity For GrowthShreyas RajanNoch keine Bewertungen

- Are US HH Living Beyond Their MeansDokument4 SeitenAre US HH Living Beyond Their Meansmarineland27127979Noch keine Bewertungen

- The Subprime Mortgage Crisis: Ann Dunn Andracchio Preeti Arunapuram Shailja Amin Arjun AjmaniDokument22 SeitenThe Subprime Mortgage Crisis: Ann Dunn Andracchio Preeti Arunapuram Shailja Amin Arjun AjmaniAnirban DubeyNoch keine Bewertungen

- The US Economic Crisis of 2008: Cause and AftermathDokument31 SeitenThe US Economic Crisis of 2008: Cause and AftermathAmrit RazNoch keine Bewertungen

- New Zealand Economics: Anz ResearchDokument16 SeitenNew Zealand Economics: Anz ResearchshreyakarNoch keine Bewertungen

- Strategy Radar - 2012 - 1012 XX Potential Housing BubbleDokument2 SeitenStrategy Radar - 2012 - 1012 XX Potential Housing BubbleStrategicInnovationNoch keine Bewertungen

- Surge in Liar Loans' From Major Aussie Bank Is Concerning'Dokument6 SeitenSurge in Liar Loans' From Major Aussie Bank Is Concerning'Rajiv RajNoch keine Bewertungen

- AAR December 2022-2Dokument14 SeitenAAR December 2022-2julian.waggNoch keine Bewertungen

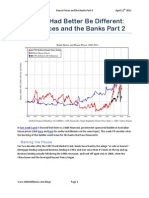

- This Time Had Better Be Different: House Prices and The Banks Part 2Dokument39 SeitenThis Time Had Better Be Different: House Prices and The Banks Part 2KamizoriNoch keine Bewertungen

- International Finance FinalDokument27 SeitenInternational Finance FinalRishabh RaiNoch keine Bewertungen

- Finance Assignment Financial CrisisDokument3 SeitenFinance Assignment Financial CrisisTayyaba TariqNoch keine Bewertungen

- Pci Dec 2013 Revised ReportDokument2 SeitenPci Dec 2013 Revised ReporteconomicdelusionNoch keine Bewertungen

- 2014.01.06 China Services PMI - December - Report PUBLICDokument3 Seiten2014.01.06 China Services PMI - December - Report PUBLICeconomicdelusionNoch keine Bewertungen

- Phat Dragon The Chart Pack January 2014Dokument101 SeitenPhat Dragon The Chart Pack January 2014economicdelusionNoch keine Bewertungen

- ABS - BoT Nov 2013Dokument44 SeitenABS - BoT Nov 2013economicdelusionNoch keine Bewertungen

- 2014.01.06 Press Release HSBC China Services PMI - December - PUBLICDokument3 Seiten2014.01.06 Press Release HSBC China Services PMI - December - PUBLICeconomicdelusionNoch keine Bewertungen

- AIG Dec 2013 PSIDokument2 SeitenAIG Dec 2013 PSIeconomicdelusionNoch keine Bewertungen

- Business Activity Expected To Lift in 2014Dokument9 SeitenBusiness Activity Expected To Lift in 2014economicdelusionNoch keine Bewertungen

- FearfulSymmetry The Chart Pack Jan 2014Dokument76 SeitenFearfulSymmetry The Chart Pack Jan 2014economicdelusionNoch keine Bewertungen

- RPData Weekend Market Summary Week Ending 2013 December 22Dokument3 SeitenRPData Weekend Market Summary Week Ending 2013 December 22economicdelusionNoch keine Bewertungen

- RP Data Rismark Home Value Index 2 January 2014MediaReleaseDokument4 SeitenRP Data Rismark Home Value Index 2 January 2014MediaReleaseeconomicdelusionNoch keine Bewertungen

- Pmi Dec 2013 Report FinalDokument2 SeitenPmi Dec 2013 Report FinaleconomicdelusionNoch keine Bewertungen

- China PMI Dec 2013Dokument4 SeitenChina PMI Dec 2013economicdelusionNoch keine Bewertungen

- Second Estimate For The Q2 2013 Euro GDPDokument6 SeitenSecond Estimate For The Q2 2013 Euro GDPeconomicdelusionNoch keine Bewertungen

- Markit Eurozone Flash PMI Sept 23 2013Dokument4 SeitenMarkit Eurozone Flash PMI Sept 23 2013economicdelusionNoch keine Bewertungen

- Euro Manufacturing PMI June 2013Dokument3 SeitenEuro Manufacturing PMI June 2013economicdelusionNoch keine Bewertungen

- Markit Flash Eurozone PMI June 2013Dokument4 SeitenMarkit Flash Eurozone PMI June 2013economicdelusionNoch keine Bewertungen

- Markit Flash Eurozone PMI July 2013Dokument4 SeitenMarkit Flash Eurozone PMI July 2013economicdelusionNoch keine Bewertungen

- EuroZone Composite PMI August 5th 2013Dokument4 SeitenEuroZone Composite PMI August 5th 2013economicdelusionNoch keine Bewertungen

- Markit Eurozone Manufacturing PMI 1st Aug 2013Dokument3 SeitenMarkit Eurozone Manufacturing PMI 1st Aug 2013economicdelusionNoch keine Bewertungen

- Euro Composite PMI June 2013Dokument4 SeitenEuro Composite PMI June 2013economicdelusionNoch keine Bewertungen

- Imf SDRDokument49 SeitenImf SDReconomicdelusionNoch keine Bewertungen

- EuroZone Composite PMI May 2013Dokument4 SeitenEuroZone Composite PMI May 2013economicdelusionNoch keine Bewertungen

- Eurozone Manufacturing PMI - May 2013Dokument3 SeitenEurozone Manufacturing PMI - May 2013economicdelusionNoch keine Bewertungen

- Markit Economics EZ PMI May 2013Dokument4 SeitenMarkit Economics EZ PMI May 2013economicdelusionNoch keine Bewertungen

- Euro PMI March 2013Dokument3 SeitenEuro PMI March 2013economicdelusionNoch keine Bewertungen

- ECB Monetary Developments April 2013Dokument6 SeitenECB Monetary Developments April 2013economicdelusionNoch keine Bewertungen

- ECB Bank Lending Survey April 2013Dokument46 SeitenECB Bank Lending Survey April 2013economicdelusionNoch keine Bewertungen

- Markit Eurozone Manufacturing PMI - 2nd May 2013Dokument3 SeitenMarkit Eurozone Manufacturing PMI - 2nd May 2013economicdelusionNoch keine Bewertungen

- Bank of Spain Economic Projects Report March2013Dokument12 SeitenBank of Spain Economic Projects Report March2013economicdelusionNoch keine Bewertungen

- March 2013 Euro Flash PMIDokument4 SeitenMarch 2013 Euro Flash PMIeconomicdelusionNoch keine Bewertungen

- Compliance Portal - Non-Filing of Return - User Guide - V2.0Dokument94 SeitenCompliance Portal - Non-Filing of Return - User Guide - V2.0Videesh Kakarla0% (1)

- Insurance Past Bar QuestionsDokument3 SeitenInsurance Past Bar QuestionsMichelle Mae Mabano100% (2)

- Investment Banking Cover Letter TemplateDokument2 SeitenInvestment Banking Cover Letter TemplateMihnea CraciunescuNoch keine Bewertungen

- Introduction of Euro As Common CurrencyDokument53 SeitenIntroduction of Euro As Common Currencysuhaspatel84Noch keine Bewertungen

- Chapter 6: Government Influence On Exchange Rate Exchange Rate System Fixed Exchange Rate SystemDokument5 SeitenChapter 6: Government Influence On Exchange Rate Exchange Rate System Fixed Exchange Rate SystemMayliya Alfi NurritaNoch keine Bewertungen

- Sps. Dela Cruz V Asian Consumer FactsDokument1 SeiteSps. Dela Cruz V Asian Consumer FactsHyuga NejiNoch keine Bewertungen

- Cost Accounting - Prelim Exam Questionaires 2Dokument2 SeitenCost Accounting - Prelim Exam Questionaires 2rowilson reyNoch keine Bewertungen

- Customer Services of ICICI and HDFC BankDokument64 SeitenCustomer Services of ICICI and HDFC BankShahzad Saif100% (1)

- Accepted Version of RevisionDokument40 SeitenAccepted Version of RevisionMunir HussainNoch keine Bewertungen

- Failed Work Needs ResitDokument15 SeitenFailed Work Needs ResitrashidaNoch keine Bewertungen

- AC Resume (English - March 2017)Dokument2 SeitenAC Resume (English - March 2017)Angelo CaraballoNoch keine Bewertungen

- Finance AccountingDokument178 SeitenFinance AccountingcostinNoch keine Bewertungen

- 17-20513 - HJK Status Report Oct 2016 PDFDokument70 Seiten17-20513 - HJK Status Report Oct 2016 PDFRecordTrac - City of OaklandNoch keine Bewertungen

- 1.1 Introduction About The Internship:: "A Study On Financial Statement Analysis"Dokument69 Seiten1.1 Introduction About The Internship:: "A Study On Financial Statement Analysis"Brian Shepherd50% (2)

- Lucky Cement Supply ChainDokument40 SeitenLucky Cement Supply ChainMohammed UbaidNoch keine Bewertungen

- Sanjay Moti LaminDokument38 SeitenSanjay Moti LaminprakashpatelkNoch keine Bewertungen

- Date Work Summary/Daily Activities Duration RemarksDokument15 SeitenDate Work Summary/Daily Activities Duration RemarksFaazila AidaNoch keine Bewertungen

- Taser International Inc.: Case AnalysisDokument21 SeitenTaser International Inc.: Case Analysisbobby B100% (1)

- FEDERAL PACER DOCKET Chapter 11 in Re Magellan Health Services IncDokument173 SeitenFEDERAL PACER DOCKET Chapter 11 in Re Magellan Health Services IncRobert Davidson, M.D., Ph.D.100% (2)

- Lesson Plan in General Mathematics Grade 11 Grade 11 - Humss/Gas/ Tvl-H.E./Tvl-SmawDokument8 SeitenLesson Plan in General Mathematics Grade 11 Grade 11 - Humss/Gas/ Tvl-H.E./Tvl-SmawRolly Dominguez BaloNoch keine Bewertungen

- Camarilla EquationDokument6 SeitenCamarilla EquationediNoch keine Bewertungen

- Establishing The Effectiveness of Market Ratios in Predicting Financial Distress of Listed Firms in Nairobi Security Exchange MarketDokument13 SeitenEstablishing The Effectiveness of Market Ratios in Predicting Financial Distress of Listed Firms in Nairobi Security Exchange MarketOIRCNoch keine Bewertungen

- A Project Report: in Partial Fulfillment For The Award of The Degree ofDokument56 SeitenA Project Report: in Partial Fulfillment For The Award of The Degree ofTushar PatelNoch keine Bewertungen

- Equity Analytics - Modern Portfolio Theory-Jonathan KinlayDokument7 SeitenEquity Analytics - Modern Portfolio Theory-Jonathan KinlaymoinNoch keine Bewertungen

- 09 Auto-Trol Technology PDFDokument28 Seiten09 Auto-Trol Technology PDFshivagetjrpNoch keine Bewertungen

- Sudhir Anand and Amartya SenDokument34 SeitenSudhir Anand and Amartya SenAnkur SinghNoch keine Bewertungen

- Notes On Commercial BankDokument8 SeitenNotes On Commercial BankMr. Rain ManNoch keine Bewertungen

- Contoh Paraphrasing, Sumarising, Quoting and AbstractDokument3 SeitenContoh Paraphrasing, Sumarising, Quoting and AbstractLuhan RinaNoch keine Bewertungen

- Hester-Biosciences Karvy 010915 PDFDokument17 SeitenHester-Biosciences Karvy 010915 PDFmannimanojNoch keine Bewertungen

- Reviewer Business Law Auto Saved)Dokument17 SeitenReviewer Business Law Auto Saved)Maria MariaNoch keine Bewertungen