Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Financial Due DiligenceDokument10 SeitenFinancial Due Diligenceapi-3822396100% (6)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Partition Deed (Huf)Dokument3 SeitenPartition Deed (Huf)api-382239685% (13)

- Vinay Shraff CVDokument4 SeitenVinay Shraff CVapi-3822396Noch keine Bewertungen

- Service TaxDokument3 SeitenService Taxapi-3822396Noch keine Bewertungen

- Valuation Under Central ExciseDokument3 SeitenValuation Under Central Exciseapi-3822396100% (1)

- Transfer PricingDokument1 SeiteTransfer Pricingapi-3822396Noch keine Bewertungen

- Value Added TaxationDokument6 SeitenValue Added Taxationapi-3822396Noch keine Bewertungen

- NRI InvestmentDokument9 SeitenNRI Investmentapi-3822396100% (2)

- SSI BenefitDokument3 SeitenSSI Benefitapi-3822396Noch keine Bewertungen

- Music 3d-VeDokument4 SeitenMusic 3d-Veapi-3822396100% (3)

- Central Excise ScopeDokument2 SeitenCentral Excise Scopeapi-3822396100% (3)

- CertificateDokument2 SeitenCertificateapi-3822396Noch keine Bewertungen

- Budget 2004-05 UpdateDokument5 SeitenBudget 2004-05 Updateapi-3822396Noch keine Bewertungen

- Why VATDokument10 SeitenWhy VATapi-3822396Noch keine Bewertungen

- List of Movable Properties Belonging To The Coparcenary Consisting of The Parties of The First, Second and Third PartDokument7 SeitenList of Movable Properties Belonging To The Coparcenary Consisting of The Parties of The First, Second and Third Partapi-3822396Noch keine Bewertungen

- Applicability of ST On ISPDokument3 SeitenApplicability of ST On ISPapi-3822396Noch keine Bewertungen

- Declaration - 2005Dokument1 SeiteDeclaration - 2005api-3822396Noch keine Bewertungen

- BT ST SaDokument2 SeitenBT ST Saapi-3822396100% (1)

- Credit Management: by Prof Sameer LakhaniDokument50 SeitenCredit Management: by Prof Sameer LakhaniDarshana Thakkar100% (3)

- G.R. No. 138197 (Fine Not Exceed 200k) PDFDokument4 SeitenG.R. No. 138197 (Fine Not Exceed 200k) PDFFrancis Ray Arbon FilipinasNoch keine Bewertungen

- Apply For A U.S. Visa - Receipt For PaymentDokument2 SeitenApply For A U.S. Visa - Receipt For Paymentsyedamadihafatima055Noch keine Bewertungen

- EPC014-20 v3.0 SEPA RTP Scheme Rulebook - 0Dokument125 SeitenEPC014-20 v3.0 SEPA RTP Scheme Rulebook - 0Thierry IshimweNoch keine Bewertungen

- Nobrokerhood App UserManualDokument13 SeitenNobrokerhood App UserManualAncy NobyNoch keine Bewertungen

- Action 2Dokument458 SeitenAction 2Stanciu Diana AndreeaNoch keine Bewertungen

- Proposal For Mobile APPDokument6 SeitenProposal For Mobile APPArunn RachuriNoch keine Bewertungen

- Byrd in Forma Pauperis Motion GrantedDokument2 SeitenByrd in Forma Pauperis Motion GrantedJ RohrlichNoch keine Bewertungen

- 2018 Us Consumer Payment Study PDFDokument52 Seiten2018 Us Consumer Payment Study PDFAshishBohraNoch keine Bewertungen

- FI Process Wise Training Plan: Sl. No Functionality Description T.CodeDokument18 SeitenFI Process Wise Training Plan: Sl. No Functionality Description T.CodeAnil SinghNoch keine Bewertungen

- Ontario Standard Lease 2021Dokument1 SeiteOntario Standard Lease 2021exohguilianaNoch keine Bewertungen

- Cembrano Vs City of Butuan GR No 163605Dokument20 SeitenCembrano Vs City of Butuan GR No 163605JamesAnthonyNoch keine Bewertungen

- Repayment Notification 123583047 2014-12-16Dokument2 SeitenRepayment Notification 123583047 2014-12-16MiguelThaxNoch keine Bewertungen

- Crossing of ChecksDokument6 SeitenCrossing of ChecksMuhammad Shifaz MamurNoch keine Bewertungen

- Social ScienceDokument4 SeitenSocial Sciencesthandwa98mailNoch keine Bewertungen

- The Banking System, What Banks Do.Dokument25 SeitenThe Banking System, What Banks Do.Andreas Widhi100% (1)

- Imp. Points of SDDokument14 SeitenImp. Points of SDjigavia80% (5)

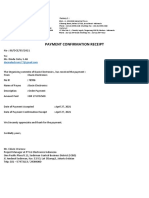

- Payment Confirmation Receipt: No: 88/DCE/05/2021Dokument2 SeitenPayment Confirmation Receipt: No: 88/DCE/05/2021Dinda Cinta NainggolanNoch keine Bewertungen

- Payment of Wages ActDokument6 SeitenPayment of Wages ActKirti YadavNoch keine Bewertungen

- IBGC - Mullapudi, Veera Venkata Satyanarayana - A00168313 - 201801Dokument2 SeitenIBGC - Mullapudi, Veera Venkata Satyanarayana - A00168313 - 201801Satya Chowdary MullapudiNoch keine Bewertungen

- RFP For Selection of Transaction Advisor For Development of Multi-Level Car Parking at Sadar Bazar, Gurugram, HaryanaDokument54 SeitenRFP For Selection of Transaction Advisor For Development of Multi-Level Car Parking at Sadar Bazar, Gurugram, HaryanabhartiNoch keine Bewertungen

- MB-800 Business Central Functional Consultant Instructor Module 4Dokument65 SeitenMB-800 Business Central Functional Consultant Instructor Module 4Mohamed HamedNoch keine Bewertungen

- Taxation 1 Case Digest by TopicDokument23 SeitenTaxation 1 Case Digest by TopicDiane JulianNoch keine Bewertungen

- 호주 La Lingua 시드니 LOTE Enrolment formDokument2 Seiten호주 La Lingua 시드니 LOTE Enrolment formJoins 세계유학Noch keine Bewertungen

- Assignment Business Law.2Dokument12 SeitenAssignment Business Law.2Abe ManNoch keine Bewertungen

- August 2020 (Al) SBLC Lease - Doa (11+2)Dokument26 SeitenAugust 2020 (Al) SBLC Lease - Doa (11+2)JosephNoch keine Bewertungen

- Metavante Technologies, Inc. 10-K (Annual Reports) 2009-02-20Dokument176 SeitenMetavante Technologies, Inc. 10-K (Annual Reports) 2009-02-20http://secwatch.comNoch keine Bewertungen

- Addon NRE NRO Savings Acc FormDokument6 SeitenAddon NRE NRO Savings Acc Formwinston11Noch keine Bewertungen

- Fundamental Forces of Change in Banking 2869Dokument50 SeitenFundamental Forces of Change in Banking 2869Pankaj_Kuamr_3748Noch keine Bewertungen

- Interest Rates and Interest ChargesDokument5 SeitenInterest Rates and Interest ChargesAlex LagunesNoch keine Bewertungen