Das könnte Ihnen auch gefallen

- Schaum's Outline of Basic Business Mathematics, 2edVon EverandSchaum's Outline of Basic Business Mathematics, 2edBewertung: 5 von 5 Sternen5/5 (1)

- Rules Dar Land AcquisitionDokument315 SeitenRules Dar Land AcquisitionTreborSelasorNoch keine Bewertungen

- OilGas DCF NAV ModelDokument21 SeitenOilGas DCF NAV ModelbankiesoleNoch keine Bewertungen

- NBA Happy Hour Co - DCF Model - Task 4 - Revised TemplateDokument10 SeitenNBA Happy Hour Co - DCF Model - Task 4 - Revised Templateww weNoch keine Bewertungen

- Void Ab InitioDokument73 SeitenVoid Ab InitioKundalini NagarajaNoch keine Bewertungen

- Basic Statistics For Business and Economics Canadian 5th Edition Lind Solutions ManualDokument15 SeitenBasic Statistics For Business and Economics Canadian 5th Edition Lind Solutions ManualKristinGreenewgdmNoch keine Bewertungen

- Property Case ReviewerDokument33 SeitenProperty Case ReviewerJanz Serrano100% (4)

- Marriott Corporation (A) Harvard Business School Case 9-394-085 Courseware 9-307-703Dokument3 SeitenMarriott Corporation (A) Harvard Business School Case 9-394-085 Courseware 9-307-703CH NAIR100% (1)

- Barangay Piapi v. TalipDokument1 SeiteBarangay Piapi v. TalipAngela ConejeroNoch keine Bewertungen

- Nba Advanced - Happy Hour Co - DCF Model v2Dokument10 SeitenNba Advanced - Happy Hour Co - DCF Model v221BAM045 Sandhiya SNoch keine Bewertungen

- RES614 Part A and Part B CFAP225 5B Group 1Dokument110 SeitenRES614 Part A and Part B CFAP225 5B Group 1umairhakim30100% (1)

- LTD - Latest Jurisprudence - SF NavarroDokument2 SeitenLTD - Latest Jurisprudence - SF NavarroRustom IbanezNoch keine Bewertungen

- Provisions Common To Pledge and MortgageDokument18 SeitenProvisions Common To Pledge and MortgageColee StiflerNoch keine Bewertungen

- Propery Case DigestDokument21 SeitenPropery Case DigestEdenFiel100% (3)

- Mindanao Bus Co. vs. City AssessorDokument6 SeitenMindanao Bus Co. vs. City Assessorred gynNoch keine Bewertungen

- Pledge Key AnswerDokument16 SeitenPledge Key AnswerAndrea GarinNoch keine Bewertungen

- Philadelphia Pa DemosDokument3 SeitenPhiladelphia Pa Demosapi-3834193Noch keine Bewertungen

- PowerPiont Presentation of Project " Analysis of Financial Statements of Glaxosmithkline Pakistan"Dokument41 SeitenPowerPiont Presentation of Project " Analysis of Financial Statements of Glaxosmithkline Pakistan"Aamir HayatNoch keine Bewertungen

- ITC LTD.: Presented ByDokument12 SeitenITC LTD.: Presented BypavanNoch keine Bewertungen

- Start Startup Financial ModelDokument5 SeitenStart Startup Financial ModelRaman TiwariNoch keine Bewertungen

- Plywood Mill Case: Variables TABLE 1-3 Spider DiagramDokument8 SeitenPlywood Mill Case: Variables TABLE 1-3 Spider DiagramYury BarqueroNoch keine Bewertungen

- Activity 3 in StatDokument13 SeitenActivity 3 in StatIanna ManieboNoch keine Bewertungen

- Laporan Cabang / Depo / Tku: Ds Jakarta 1 Monday, March 01, 2021 / Panas - Hujan - Mendung - KabutDokument31 SeitenLaporan Cabang / Depo / Tku: Ds Jakarta 1 Monday, March 01, 2021 / Panas - Hujan - Mendung - KabutTofan sofyanNoch keine Bewertungen

- Werner - Financial Model - Final VersionDokument2 SeitenWerner - Financial Model - Final VersionAmit JainNoch keine Bewertungen

- 100 50% ROIC (%) 10% Multiple 10 Valuation 1000 Current Earnings Power ($) Earnings Retained (%)Dokument5 Seiten100 50% ROIC (%) 10% Multiple 10 Valuation 1000 Current Earnings Power ($) Earnings Retained (%)Rishab WahalNoch keine Bewertungen

- Calculating Trend PercentageDokument2 SeitenCalculating Trend PercentageSaravananSrvnNoch keine Bewertungen

- Excel Dashboard Templates 06Dokument10 SeitenExcel Dashboard Templates 06Akhil RajNoch keine Bewertungen

- Quiz # 6Dokument2 SeitenQuiz # 6arslan mumtazNoch keine Bewertungen

- Price R 1 6 1 100 2 8 2 100 3 9.5 3 100 4 10.5 4 100 5 11 5 100 Coupon (Annual, %) Maturity (Years) B (Discount Factor)Dokument11 SeitenPrice R 1 6 1 100 2 8 2 100 3 9.5 3 100 4 10.5 4 100 5 11 5 100 Coupon (Annual, %) Maturity (Years) B (Discount Factor)Archit PateriaNoch keine Bewertungen

- Assumptions: Cell LockDokument21 SeitenAssumptions: Cell LockUmar YaqoobNoch keine Bewertungen

- 6 Polaroid Corporation 1996Dokument64 Seiten6 Polaroid Corporation 1996jk kumarNoch keine Bewertungen

- Kel 2Dokument1 SeiteKel 2EVI DAMAYANTI SIREGARNoch keine Bewertungen

- Financial Analysis Part 4Dokument9 SeitenFinancial Analysis Part 4Llyod Francis LaylayNoch keine Bewertungen

- Appendix A BudgetDokument1 SeiteAppendix A BudgetJack ChappelNoch keine Bewertungen

- Nike Case Study VrindaDokument4 SeitenNike Case Study VrindaAnchal ChokhaniNoch keine Bewertungen

- The Bass Model Unscrambling Regression Coefficients For P&QDokument4 SeitenThe Bass Model Unscrambling Regression Coefficients For P&QCristhianNoch keine Bewertungen

- Name Company Years Data GatheringDokument59 SeitenName Company Years Data GatheringJessa Sabrina AvilaNoch keine Bewertungen

- Nguyen Duc Anh. CA7-010Dokument5 SeitenNguyen Duc Anh. CA7-010Đức Anh LeoNoch keine Bewertungen

- Tourism Data 2015Dokument6 SeitenTourism Data 2015aakansha.limbasiyaNoch keine Bewertungen

- Polaroid 1996 CalculationDokument8 SeitenPolaroid 1996 CalculationDev AnandNoch keine Bewertungen

- Uv0052 Xls EngDokument12 SeitenUv0052 Xls Engpriyanshu14Noch keine Bewertungen

- FS CanvassingDokument3 SeitenFS CanvassingziannahamarahfaithNoch keine Bewertungen

- G2 - Sample ######1### 0 30 30 Per 1 9 15 20 10 G1 - 44 55 ###2### 0 100 100 Num 0 9 15 70 30Dokument22 SeitenG2 - Sample ######1### 0 30 30 Per 1 9 15 20 10 G1 - 44 55 ###2### 0 100 100 Num 0 9 15 70 30The HoangNoch keine Bewertungen

- Share of Total Amount Amongst Salesmenin ABC CompanyDokument23 SeitenShare of Total Amount Amongst Salesmenin ABC CompanyNoah TeshomeNoch keine Bewertungen

- Time Study Observation Form: Element No. and DescriptionDokument6 SeitenTime Study Observation Form: Element No. and DescriptionLiz FernandezNoch keine Bewertungen

- Moving Average: 130 140 Actual ForecastDokument12 SeitenMoving Average: 130 140 Actual ForecastFaith MateoNoch keine Bewertungen

- Pesanan Produk Kapasitas Produksi Periode Quantity Periode Reguler Overtime SubkontrakDokument28 SeitenPesanan Produk Kapasitas Produksi Periode Quantity Periode Reguler Overtime SubkontrakThitha MeistaNoch keine Bewertungen

- Hero Motocorp EvaDokument1 SeiteHero Motocorp EvaproNoch keine Bewertungen

- Utilities Stock Guide: WeeklyDokument16 SeitenUtilities Stock Guide: WeeklyManuel Jeremias CaldasNoch keine Bewertungen

- Analysis of Financial Statements: Muhammad SarwarDokument9 SeitenAnalysis of Financial Statements: Muhammad SarwarawaischeemaNoch keine Bewertungen

- 20 ChartDokument7 Seiten20 ChartYashwant MaruNoch keine Bewertungen

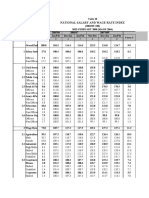

- National Salary and Wage Rate Index - Mid-February - 08Dokument4 SeitenNational Salary and Wage Rate Index - Mid-February - 08Madhav BaralNoch keine Bewertungen

- Frequency TableDokument6 SeitenFrequency TableLê Hoàng VyNoch keine Bewertungen

- Statistical TechniquesDokument11 SeitenStatistical TechniquesLipika DasNoch keine Bewertungen

- 102 Sol 1104Dokument10 Seiten102 Sol 1104api-3701114Noch keine Bewertungen

- SOLVED Business StatisticsDokument21 SeitenSOLVED Business StatisticsRajni KumariNoch keine Bewertungen

- Initial investment Time horizon (years) Return µ σ Stock marketDokument17 SeitenInitial investment Time horizon (years) Return µ σ Stock marketvaskoreNoch keine Bewertungen

- The Beer Cafe FOFO - Business Model - JodhpurDokument1 SeiteThe Beer Cafe FOFO - Business Model - JodhpurTarunNoch keine Bewertungen

- Declining BalanceDokument15 SeitenDeclining BalanceGigih Adi PambudiNoch keine Bewertungen

- Unair Setting TimeDokument26 SeitenUnair Setting TimeNaufal AlieefNoch keine Bewertungen

- Full Smolov Program: Fill in Light Grey Boxes 1RMDokument12 SeitenFull Smolov Program: Fill in Light Grey Boxes 1RMEd de BonbonNoch keine Bewertungen

- Spss ResultDokument13 SeitenSpss Resultapi-561566045Noch keine Bewertungen

- Summary Output: Regression StatisticsDokument6 SeitenSummary Output: Regression StatisticsJo MalaluanNoch keine Bewertungen

- H. Paul Barringer, P.E.: (In Red)Dokument7 SeitenH. Paul Barringer, P.E.: (In Red)api-19921807Noch keine Bewertungen

- Assignment 2 - 27110079 - Shahmir Abdullah ShahidDokument7 SeitenAssignment 2 - 27110079 - Shahmir Abdullah ShahidShahmir AbdullahNoch keine Bewertungen

- Discounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No FormulasDokument2 SeitenDiscounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No Formulasrito2005Noch keine Bewertungen

- 5 Herman Miller Presentation Group Final 1Dokument31 Seiten5 Herman Miller Presentation Group Final 1lynklynkNoch keine Bewertungen

- Mean, Median, and ModeDokument4 SeitenMean, Median, and ModeMarjenette Del ValleNoch keine Bewertungen

- IE 343 Section 1 Engineering Economy Exam 1 Review Problems - SolutionDokument6 SeitenIE 343 Section 1 Engineering Economy Exam 1 Review Problems - SolutionSeb TegNoch keine Bewertungen

- Bond ValueDokument12 SeitenBond ValuePhuntru PhiNoch keine Bewertungen

- Assam Non Agricultural Urban Areas Tenancy Act1955Dokument8 SeitenAssam Non Agricultural Urban Areas Tenancy Act1955Latest Laws TeamNoch keine Bewertungen

- AMAR Power Point Presentation 602601 7Dokument22 SeitenAMAR Power Point Presentation 602601 7Dennis JudsonNoch keine Bewertungen

- Sas Diamond Towers Commercial BrochureDokument8 SeitenSas Diamond Towers Commercial Brochureyehitsme4uNoch keine Bewertungen

- Points To Be Added For Goa Land Due DiligenceDokument5 SeitenPoints To Be Added For Goa Land Due Diligenceparasshah.kljNoch keine Bewertungen

- 425 24th Ave N Purchase Agreement Gregg Karnis Steven MeldahlDokument7 Seiten425 24th Ave N Purchase Agreement Gregg Karnis Steven MeldahlCamdenCanaryNoch keine Bewertungen

- Leonardo V RepublicDokument5 SeitenLeonardo V Republicbenipayo. lawNoch keine Bewertungen

- Redemption: Exists Only in Real Estate Mortgage Enclosure. The Period ToDokument27 SeitenRedemption: Exists Only in Real Estate Mortgage Enclosure. The Period ToReign Christel EstefanioNoch keine Bewertungen

- As of December 2, 2010: MHA Handbook v3.0 1Dokument170 SeitenAs of December 2, 2010: MHA Handbook v3.0 1jadlao8000dNoch keine Bewertungen

- Deed of AdjudicationDokument1 SeiteDeed of AdjudicationBrian SususcoNoch keine Bewertungen

- Rent Summary SheetDokument4 SeitenRent Summary SheetfairwellmdNoch keine Bewertungen

- Protax 04Dokument10 SeitenProtax 04aptureincNoch keine Bewertungen

- Ong V Ong DigestDokument2 SeitenOng V Ong DigestFrancisCarloL.FlameñoNoch keine Bewertungen

- Obq 6 - Answer FullyDokument2 SeitenObq 6 - Answer FullyYralli MendozaNoch keine Bewertungen

- Only For Information: Index EntryDokument2 SeitenOnly For Information: Index EntryManjunathNoch keine Bewertungen

- Seraspi v. CADokument5 SeitenSeraspi v. CABianca Marie FlorNoch keine Bewertungen

- Rules andDokument30 SeitenRules andBabaji BautistaNoch keine Bewertungen

- CPM Listing-20160106Dokument9 SeitenCPM Listing-20160106SenyumSajerNoch keine Bewertungen

- Nitshill Road, GlasgowDokument2 SeitenNitshill Road, GlasgowAppletonCraigNoch keine Bewertungen

- 2nd Assignment PDFDokument36 Seiten2nd Assignment PDFbobNoch keine Bewertungen

- Juja Land Owners To Be Issued With Title DeedsDokument2 SeitenJuja Land Owners To Be Issued With Title DeedsJamesMMureithiNoch keine Bewertungen