Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- E Receipt - Cons 0614373464Dokument1 SeiteE Receipt - Cons 0614373464yaswanthkapoorNoch keine Bewertungen

- Blasting EconomicsDokument36 SeitenBlasting EconomicsRezaNoch keine Bewertungen

- Economy Shipping (HBS Case) - MSN SolutionDokument24 SeitenEconomy Shipping (HBS Case) - MSN SolutionPrasanta Mondal100% (2)

- Positive Money - Modernising Money by Andrew Jackson, Ben DysonDokument251 SeitenPositive Money - Modernising Money by Andrew Jackson, Ben DysonHelyi Pénz100% (4)

- City of Manila, Et Al vs. Judge Colet, and Malaysian Airline SystemDokument2 SeitenCity of Manila, Et Al vs. Judge Colet, and Malaysian Airline SystemRaquel DoqueniaNoch keine Bewertungen

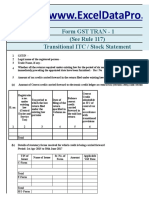

- GST TRAN 1 Return Excel TemplateDokument14 SeitenGST TRAN 1 Return Excel TemplateRaju Ranjan KumarNoch keine Bewertungen

- Research On DemonetizationDokument61 SeitenResearch On DemonetizationHARSHITA CHAURASIYANoch keine Bewertungen

- H Aptitude GACH PDFDokument71 SeitenH Aptitude GACH PDFEmebet ShibieNoch keine Bewertungen

- CIR V COFA - VAT ExemptionDokument2 SeitenCIR V COFA - VAT ExemptionJose MasarateNoch keine Bewertungen

- CompanyDokument2 SeitenCompanyhusse fokNoch keine Bewertungen

- Audit Report On Sales TaxDokument27 SeitenAudit Report On Sales TaxharshNoch keine Bewertungen

- Tax 1Dokument29 SeitenTax 1LoNoch keine Bewertungen

- Eic FrameworkDokument37 SeitenEic FrameworkABSDJIGY0% (1)

- Business Studies Past PaperDokument4 SeitenBusiness Studies Past Paperbereket tesfayeNoch keine Bewertungen

- Legal NoteDokument4 SeitenLegal NoteShubham Jain ModiNoch keine Bewertungen

- 0455 - m18 - 2 - 2 - QP IGCSEDokument8 Seiten0455 - m18 - 2 - 2 - QP IGCSEloveupdownNoch keine Bewertungen

- Offshore Banking Definition, Benefits & Offshore AccountDokument8 SeitenOffshore Banking Definition, Benefits & Offshore AccountRoy Navarro VispoNoch keine Bewertungen

- Cpa Review School of The Philippines ManilaDokument2 SeitenCpa Review School of The Philippines ManilaAljur SalamedaNoch keine Bewertungen

- Narayana Group of Schools: Bill of Supply OriginalDokument1 SeiteNarayana Group of Schools: Bill of Supply OriginalSk NurhasanNoch keine Bewertungen

- Section 5 - Pro Forma Contract - 210084Dokument55 SeitenSection 5 - Pro Forma Contract - 210084OQC PetroleumNoch keine Bewertungen

- Queries Related To ITR FilingDokument3 SeitenQueries Related To ITR FilingRajesh KashyapNoch keine Bewertungen

- Morgan Stanley Case LawDokument2 SeitenMorgan Stanley Case LawakshNoch keine Bewertungen

- Income Taxation Chapter 9Dokument11 SeitenIncome Taxation Chapter 9Kim Patrice NavarraNoch keine Bewertungen

- Cases On Partnerships/ Co-Ownership/ Joint Venture: Tax 1 ReportDokument40 SeitenCases On Partnerships/ Co-Ownership/ Joint Venture: Tax 1 ReportNaomi CorpuzNoch keine Bewertungen

- Answers To CivilDokument3 SeitenAnswers To CivilDenee Vem MatorresNoch keine Bewertungen

- Advanced Engineering Economics For Engineer Managers: Mcgraw-Hill/IrwinDokument27 SeitenAdvanced Engineering Economics For Engineer Managers: Mcgraw-Hill/IrwincamilodomesaNoch keine Bewertungen

- Analysis of The Influence of Local Tax Revenue, Regional Retribution and Results of Separate Regional Wealth Management On Regional Original Revenue (PAD) of North Sumatra Regency/CityDokument12 SeitenAnalysis of The Influence of Local Tax Revenue, Regional Retribution and Results of Separate Regional Wealth Management On Regional Original Revenue (PAD) of North Sumatra Regency/CityM IqbalNoch keine Bewertungen

- Unit 1 Notes TaxDokument14 SeitenUnit 1 Notes TaxSuryansh MunjalNoch keine Bewertungen

- Annex C Tax ClearanceDokument1 SeiteAnnex C Tax Clearanceanalisa sealmoyNoch keine Bewertungen

- Invoice TemplateDokument2 SeitenInvoice TemplateMM Fakhrul IslamNoch keine Bewertungen