Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Uses and Limitations of Profitability Ratio Analysis in Managerial PracticeDokument6 SeitenUses and Limitations of Profitability Ratio Analysis in Managerial PracticeAlexandra AxNoch keine Bewertungen

- WWW - Capitalwaters.nl: Capital Waters Convertible Loan Agreement A.1.0 Page 1 of 9Dokument9 SeitenWWW - Capitalwaters.nl: Capital Waters Convertible Loan Agreement A.1.0 Page 1 of 9Anouar El HajiNoch keine Bewertungen

- Updates (Company Update)Dokument1 SeiteUpdates (Company Update)Shyam SunderNoch keine Bewertungen

- Dissolution of PartnershipDokument17 SeitenDissolution of PartnershipJASKARANNoch keine Bewertungen

- 2 Ceng 6108Dokument49 Seiten2 Ceng 6108addisu SissayNoch keine Bewertungen

- Loan Applicatinaniagsloauwvjwon FormDokument6 SeitenLoan Applicatinaniagsloauwvjwon FormSantosh Kumar GuptaNoch keine Bewertungen

- Introduction To Accounting: Pg. 1 Compiled By: Abdul Ahad ButtDokument38 SeitenIntroduction To Accounting: Pg. 1 Compiled By: Abdul Ahad ButtMuhammad FaisalNoch keine Bewertungen

- Commonwealth Bank StatementDokument5 SeitenCommonwealth Bank Statementsattazee1992100% (1)

- Social Entrepreneurship ManualDokument54 SeitenSocial Entrepreneurship ManualAndreea AcxinteNoch keine Bewertungen

- Indebtedness Assumed Exceeds Tax Basis of Property SoldDokument3 SeitenIndebtedness Assumed Exceeds Tax Basis of Property SoldJemalyn De Guzman TuringanNoch keine Bewertungen

- What If Gafa Replaced Traditional Banks?: Translation: Wency-Wenceslas MOUNDOUNGADokument10 SeitenWhat If Gafa Replaced Traditional Banks?: Translation: Wency-Wenceslas MOUNDOUNGAMike BurdickNoch keine Bewertungen

- Internship Report On Meezan Bank CompleteDokument86 SeitenInternship Report On Meezan Bank CompleteArslan96% (27)

- Chap 013Dokument30 SeitenChap 013sueernNoch keine Bewertungen

- UBS Investment Fund Account/Custody Account RegulationsDokument2 SeitenUBS Investment Fund Account/Custody Account RegulationsLeonardo RivasNoch keine Bewertungen

- Chapter 12 - Leverage - Text and End of Chapter Questions - 1Dokument39 SeitenChapter 12 - Leverage - Text and End of Chapter Questions - 1naimenimNoch keine Bewertungen

- For The Year Ended Year 1 Year 2 Year 3 Year 4: Income Statement ParticularsDokument5 SeitenFor The Year Ended Year 1 Year 2 Year 3 Year 4: Income Statement ParticularsTanya SinghNoch keine Bewertungen

- Drill 1 (15 Marks) : General Direction: Place On A Separate Sheet of Paper and Show Supporting Solutions in Good FormDokument3 SeitenDrill 1 (15 Marks) : General Direction: Place On A Separate Sheet of Paper and Show Supporting Solutions in Good FormKaye GonxalesNoch keine Bewertungen

- NBFC in IndiaDokument19 SeitenNBFC in IndiaBharath ReddyNoch keine Bewertungen

- Riding The South Sea Bubble (Peter Temin e Hans-Joachim Voth)Dokument52 SeitenRiding The South Sea Bubble (Peter Temin e Hans-Joachim Voth)João Henrique F. VieiraNoch keine Bewertungen

- Multiple Choice QuestionsDokument6 SeitenMultiple Choice QuestionsCandy DollNoch keine Bewertungen

- Credit Card ApplicationsDokument36 SeitenCredit Card Applicationsapi-333146577Noch keine Bewertungen

- FAR B41 Final Pre-Board Exam (Questions, Answers - Solutions)Dokument14 SeitenFAR B41 Final Pre-Board Exam (Questions, Answers - Solutions)Joanna MalubayNoch keine Bewertungen

- Rupee Max FormccbDokument2 SeitenRupee Max FormccbDesikanNoch keine Bewertungen

- Investment Risk Tolerance QuizDokument3 SeitenInvestment Risk Tolerance QuizPrabriti NeupaneNoch keine Bewertungen

- البنك الضامنDokument21 Seitenالبنك الضامنNada QiseerNoch keine Bewertungen

- Fundamental Analysis SeminarDokument18 SeitenFundamental Analysis SeminarAndrew WangNoch keine Bewertungen

- 02 2024 2 02446996 Fee VoucherDokument1 Seite02 2024 2 02446996 Fee Vouchersaeed123awan566Noch keine Bewertungen

- Questions Chapter 7Dokument22 SeitenQuestions Chapter 7SA 10Noch keine Bewertungen

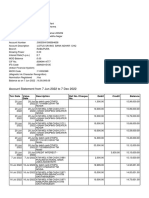

- Account Statement From 7 Jun 2022 To 7 Dec 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument3 SeitenAccount Statement From 7 Jun 2022 To 7 Dec 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRdb TalkNoch keine Bewertungen

- Arslan Rahim Financial and Risk ManagementDokument21 SeitenArslan Rahim Financial and Risk ManagementTehreem ZafarNoch keine Bewertungen