Das könnte Ihnen auch gefallen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Health & Wellbeing Programmes: Royal Mail GroupDokument15 SeitenHealth & Wellbeing Programmes: Royal Mail GroupLiam BrewsterNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Economic, Social Impacts and Operation of Smart Factories in Industry 4.0 Focusing On Simulation and Artificial Intelligence of Collaborating RobotsDokument20 SeitenEconomic, Social Impacts and Operation of Smart Factories in Industry 4.0 Focusing On Simulation and Artificial Intelligence of Collaborating RobotsDrakzNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Scientia L 2023Dokument244 SeitenScientia L 2023john umaru rikkaNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- How To Write A Salt Room Business PlanDokument15 SeitenHow To Write A Salt Room Business Planwaleed saeedNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Session6 - OD InterventionDokument4 SeitenSession6 - OD InterventionPriyam BatraNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Parate EksekusiDokument15 SeitenParate EksekusiWanda WandaNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Artist Self Promotion BookDokument218 SeitenArtist Self Promotion BookGregori Veverka100% (5)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Culinarian CookwareDokument8 SeitenCulinarian CookwarePratip BeraNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- 01JUNIDokument1 Seite01JUNISteven Kuang01Noch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- SS - 9 - Forfeiture of SharesDokument3 SeitenSS - 9 - Forfeiture of SharesMihir MehtaNoch keine Bewertungen

- Neelima Prabhala - IndiaDokument3 SeitenNeelima Prabhala - Indiadharmendratyagi232Noch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- SL - No. Company Building Name Unit No. Floor NoDokument25 SeitenSL - No. Company Building Name Unit No. Floor Novijay kumar anantNoch keine Bewertungen

- Gerund Infinitive ParticipleDokument4 SeitenGerund Infinitive ParticiplemertNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- International Accounting Standard With ExamplesDokument15 SeitenInternational Accounting Standard With ExamplesAmna MirzaNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Intitulé Du Module: Business English Durée de La Formation: 30 Hours Déroulé J1Dokument5 SeitenIntitulé Du Module: Business English Durée de La Formation: 30 Hours Déroulé J1benzidaNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- SAPTP-4058 - CNH Brand Vendor Consignment Process - SAP Estimate v0.4Dokument13 SeitenSAPTP-4058 - CNH Brand Vendor Consignment Process - SAP Estimate v0.4Chandra MathiNoch keine Bewertungen

- Finance Lecturers by Course and Size UNSWDokument2 SeitenFinance Lecturers by Course and Size UNSWhello248Noch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Calasanz V CIRDokument6 SeitenCalasanz V CIRevelyn b t.Noch keine Bewertungen

- Chiefdissertation 161006221902 PDFDokument59 SeitenChiefdissertation 161006221902 PDFManoj Kumar100% (1)

- Phrasal Verbs DialogueDokument5 SeitenPhrasal Verbs DialogueAna NedeljkovicNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Manac Quiz 2 With AnswersDokument2 SeitenManac Quiz 2 With AnswersHanabusa Kawaii IdouNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Waqar Ahmed & Kashif Shafiq: Question Number: 1 Nowadays Business Environment Is Filled With Uncertainty. KeepingDokument4 SeitenWaqar Ahmed & Kashif Shafiq: Question Number: 1 Nowadays Business Environment Is Filled With Uncertainty. KeepingAhad Sultan100% (1)

- Population Growth and DevelopmentDokument22 SeitenPopulation Growth and DevelopmentKathrine CadalsoNoch keine Bewertungen

- A Personal Selling Strategy: DevelopingDokument14 SeitenA Personal Selling Strategy: DevelopingAdeesh KakkarNoch keine Bewertungen

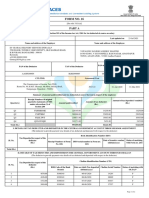

- Form No. 16: Part ADokument6 SeitenForm No. 16: Part AVinuthna ChinnapaNoch keine Bewertungen

- CHPT 1...... The Foundations of EntrepreneurshipDokument62 SeitenCHPT 1...... The Foundations of EntrepreneurshipHashim MalikNoch keine Bewertungen

- Yahoo Symbol ListDokument21 SeitenYahoo Symbol ListShubham RohatgiNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- RE: POLICY #: A13267806PLA NAME OF INSURED: Ossilien ThimotDokument1 SeiteRE: POLICY #: A13267806PLA NAME OF INSURED: Ossilien ThimotAndre SenabNoch keine Bewertungen

- EnrollmentDokument4 SeitenEnrollmentJet Boclaras100% (1)

- SLT eBill-00372777690152ImageDokument1 SeiteSLT eBill-00372777690152ImageDushshantha Gayashan0% (1)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)