Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- 2012 Aug Isbank Bank Asya ReviewDokument4 Seiten2012 Aug Isbank Bank Asya ReviewisfinturkNoch keine Bewertungen

- 2012 June 20 Moody's RatingsDokument4 Seiten2012 June 20 Moody's RatingsisfinturkNoch keine Bewertungen

- 2012 April JCR Albaraka RatingsDokument1 Seite2012 April JCR Albaraka RatingsisfinturkNoch keine Bewertungen

- Programme MCS - ForeignDokument1 SeiteProgramme MCS - ForeignisfinturkNoch keine Bewertungen

- 2012 May Sukuk Conference World Bank AgendaDokument2 Seiten2012 May Sukuk Conference World Bank AgendaisfinturkNoch keine Bewertungen

- 2012 Feb Isyatirim Albaraka TRKDokument4 Seiten2012 Feb Isyatirim Albaraka TRKisfinturkNoch keine Bewertungen

- 2012 May Isyatirim Bank Asya ReportDokument4 Seiten2012 May Isyatirim Bank Asya ReportisfinturkNoch keine Bewertungen

- 2012 May 30 Aibim TKBB MouDokument1 Seite2012 May 30 Aibim TKBB MouisfinturkNoch keine Bewertungen

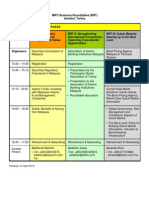

- MIFC Business Roundtables - RevisedDokument1 SeiteMIFC Business Roundtables - RevisedisfinturkNoch keine Bewertungen

- 2012 Islamic Indonesia Call Papers TurkeyDokument3 Seiten2012 Islamic Indonesia Call Papers TurkeyisfininNoch keine Bewertungen

- 2012 Gulf Research MeetingDokument1 Seite2012 Gulf Research MeetingisfinturkNoch keine Bewertungen

- 2011 Islamic Turkey Article Bicer IfnDokument2 Seiten2011 Islamic Turkey Article Bicer IfnisfinturkNoch keine Bewertungen

- 2011 Oct 21 JCR Eurasia Albaraka Islamic TurkDokument1 Seite2011 Oct 21 JCR Eurasia Albaraka Islamic TurkisfinturkNoch keine Bewertungen

- 2011nov Isyatirim Turkey Albaraka TurkDokument4 Seiten2011nov Isyatirim Turkey Albaraka TurkisfinturkNoch keine Bewertungen

- 2010 Yavuz YeterDokument11 Seiten2010 Yavuz YeterisfinturkNoch keine Bewertungen

- 2010 Nov IFN TurkeyDokument3 Seiten2010 Nov IFN TurkeyisfinturkNoch keine Bewertungen

- 2010 September Singapore Law Gazette Use of Contracts of Sale - DocxDokument10 Seiten2010 September Singapore Law Gazette Use of Contracts of Sale - DocxisfinturkNoch keine Bewertungen

- 2010 IFSB-11 - Standard On Solvency Requirements For Takaful (Islamic Insurance) UndertakingsDokument34 Seiten2010 IFSB-11 - Standard On Solvency Requirements For Takaful (Islamic Insurance) UndertakingsisfinturkNoch keine Bewertungen

- 2010 Eng - IFSB-11 - Standard On Solvency Requirements For Takaful (Islamic Insurance) UndertakingsDokument34 Seiten2010 Eng - IFSB-11 - Standard On Solvency Requirements For Takaful (Islamic Insurance) UndertakingsisfinturkNoch keine Bewertungen

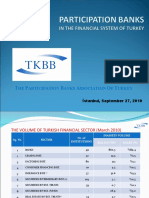

- 2010 Sept Participation Banks PresentationDokument26 Seiten2010 Sept Participation Banks PresentationisfinturkNoch keine Bewertungen

- Islamic vs. Conventional BankingDokument44 SeitenIslamic vs. Conventional BankingSyed Shaker AhmedNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Fin Analysis - Tvs Motor CompanyDokument16 SeitenFin Analysis - Tvs Motor Companygarconfrancais06Noch keine Bewertungen

- Module 13 Notes Payable - Debt ResructuringDokument10 SeitenModule 13 Notes Payable - Debt ResructuringryanNoch keine Bewertungen

- Jaclyn Resume New 1Dokument4 SeitenJaclyn Resume New 1api-297244528Noch keine Bewertungen

- QuestionsDokument87 SeitenQuestionsramu_n16100% (2)

- Telangana Strike Salary Loan 42 DaysDokument2 SeitenTelangana Strike Salary Loan 42 DaysSEKHARNoch keine Bewertungen

- Political Economy Students Group and Individual AchievementsDokument7 SeitenPolitical Economy Students Group and Individual AchievementsMaricar BautistaNoch keine Bewertungen

- Chapter 12 - Solution ManualDokument23 SeitenChapter 12 - Solution Manualjuan100% (2)

- Equipment Management - Mr. Gautam AroraDokument31 SeitenEquipment Management - Mr. Gautam AroraDevendra Pratap Singh Rajput100% (1)

- Property Sales Agreement TemplateDokument3 SeitenProperty Sales Agreement TemplateAnonymous 7vC1ljNoch keine Bewertungen

- Accounting RatiosDokument5 SeitenAccounting RatiosNaga NikhilNoch keine Bewertungen

- 300 Million Engines of Growth: A Middle-Out Plan For Jobs, Business, and A Growing EconomyDokument252 Seiten300 Million Engines of Growth: A Middle-Out Plan For Jobs, Business, and A Growing EconomyCenter for American ProgressNoch keine Bewertungen

- Heavy Engineeiring Coporation at A Glance: Public Sector Undertaking IndiaDokument19 SeitenHeavy Engineeiring Coporation at A Glance: Public Sector Undertaking IndiaNitish Kumar TiwaryNoch keine Bewertungen

- Oblicon DigestsDokument33 SeitenOblicon Digestsjlumbres100% (1)

- Working Capital ManagementDokument56 SeitenWorking Capital ManagementSahil KhanNoch keine Bewertungen

- Financial Literacy ProjectDokument20 SeitenFinancial Literacy Projectapi-286182524Noch keine Bewertungen

- Government Budget and Its Components: Neeraj GarwalDokument39 SeitenGovernment Budget and Its Components: Neeraj GarwalShubh Somani67% (3)

- Highlander Club Aug2003Dokument8 SeitenHighlander Club Aug2003choileoNoch keine Bewertungen

- ProspectusDokument17 SeitenProspectusPallavi Varshney100% (1)

- Branch Accounting TestbankDokument5 SeitenBranch Accounting TestbankCyanLouiseM.Ellixir100% (6)

- Special Power AttorneyDokument2 SeitenSpecial Power Attorneymcjeff32Noch keine Bewertungen

- NCBP (NGO) ProfileDokument34 SeitenNCBP (NGO) ProfileNCBP100% (1)

- Work Measurement Techniques Methods TypesDokument5 SeitenWork Measurement Techniques Methods TypesManoj BallaNoch keine Bewertungen

- 15 - Country Bankers Insurance Corp Vs Lianga BayDokument8 Seiten15 - Country Bankers Insurance Corp Vs Lianga BayVincent OngNoch keine Bewertungen

- Competition in South African Banking SectorDokument171 SeitenCompetition in South African Banking SectordffinanceethiopiaNoch keine Bewertungen

- Deed of Sale of Motor VehicleDokument7 SeitenDeed of Sale of Motor VehicleMarc CalderonNoch keine Bewertungen

- DOP Guidelines AML KYC For MTSS and Forex13112018Dokument19 SeitenDOP Guidelines AML KYC For MTSS and Forex13112018DEBADITYA CHAKRABORTYNoch keine Bewertungen

- PNB Vs CADokument2 SeitenPNB Vs CAArnold Rosario ManzanoNoch keine Bewertungen

- Microeconomics - Problem Set 4Dokument4 SeitenMicroeconomics - Problem Set 4Juho ViljanenNoch keine Bewertungen

- Money Markets ReviewerDokument4 SeitenMoney Markets ReviewerHazel Jane EsclamadaNoch keine Bewertungen

- Money MarketDokument67 SeitenMoney MarketAvinash Veerendra TakNoch keine Bewertungen