Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Ge Capital Mar19-09 PresentationDokument88 SeitenGe Capital Mar19-09 PresentationCarneades100% (2)

- Lorna Lamotte Motion To Dismiss 2ND Amended ComplaintDokument81 SeitenLorna Lamotte Motion To Dismiss 2ND Amended ComplaintSLAVEFATHERNoch keine Bewertungen

- Project Report Consumer Behaviour (Icici Pru)Dokument90 SeitenProject Report Consumer Behaviour (Icici Pru)balaji bysani67% (6)

- BURTON, The Roman Imperial State, Provincial Governors and The Public Finances of Provincial Cities, 27 B.C.-A.D. 235Dokument33 SeitenBURTON, The Roman Imperial State, Provincial Governors and The Public Finances of Provincial Cities, 27 B.C.-A.D. 235seminariodigenovaNoch keine Bewertungen

- Cancellation of MortgageDokument1 SeiteCancellation of MortgageARCHILE100% (1)

- XYZ Trading Exercise: Balance Sheet Class Notes Business TransactionsDokument3 SeitenXYZ Trading Exercise: Balance Sheet Class Notes Business TransactionsMisu NguyenNoch keine Bewertungen

- Framework For Employee-Incentive PlanDokument21 SeitenFramework For Employee-Incentive PlanRezaNoch keine Bewertungen

- Domestic Credit Related Service Charges: Head Office, BangaloreDokument27 SeitenDomestic Credit Related Service Charges: Head Office, BangaloreAnwesha SinghNoch keine Bewertungen

- Account OriginationDokument23 SeitenAccount Originationsans1234Noch keine Bewertungen

- Banking Structure in IndiaDokument49 SeitenBanking Structure in IndiaAjay RapelliNoch keine Bewertungen

- University of The Philippines vs. de Los Angeles 35 Scra 102Dokument5 SeitenUniversity of The Philippines vs. de Los Angeles 35 Scra 102Gale Charm SeñerezNoch keine Bewertungen

- Automatic Dissolution of Lis Pendens Notice, Rule 1.420 (F)Dokument14 SeitenAutomatic Dissolution of Lis Pendens Notice, Rule 1.420 (F)Albertelli_Law100% (1)

- SGV and Co Presentation On TRAIN LawDokument48 SeitenSGV and Co Presentation On TRAIN LawPortCalls100% (8)

- Trust DocumentsDokument7 SeitenTrust DocumentsDreanetics media67% (3)

- Account Information: Danielle D. PascuaDokument2 SeitenAccount Information: Danielle D. PascuaKaye AnnNoch keine Bewertungen

- Rule of Marshalling: Damodaram Sanjivayya National Law University VisakhapatnamDokument10 SeitenRule of Marshalling: Damodaram Sanjivayya National Law University VisakhapatnamNaveen Choudary100% (1)

- Tuscaloosa Short-Term Rental Properties PolicyDokument18 SeitenTuscaloosa Short-Term Rental Properties Policyjafranklin-1Noch keine Bewertungen

- CMS ReportDokument81 SeitenCMS ReportRecordTrac - City of OaklandNoch keine Bewertungen

- FEBTC Vs Diaz RealtyDokument8 SeitenFEBTC Vs Diaz RealtyVictor LimNoch keine Bewertungen

- Ravi Panwar FIIB CIP-2019-Report PDFDokument53 SeitenRavi Panwar FIIB CIP-2019-Report PDFRavi SinghNoch keine Bewertungen

- General AnnuityDokument21 SeitenGeneral AnnuityMark Alconaba GeronimoNoch keine Bewertungen

- SecuritizationDokument11 SeitenSecuritizationyash nathaniNoch keine Bewertungen

- Reviewer in PPEDokument16 SeitenReviewer in PPEDewi Leigh Ann Mangubat50% (2)

- CIV2 Tip SheetDokument23 SeitenCIV2 Tip Sheetdenbar15Noch keine Bewertungen

- Chapter 1 Saunders Cornett McGrawDokument58 SeitenChapter 1 Saunders Cornett McGrawAlice WenNoch keine Bewertungen

- Relationship Between GDP, Consumption, Savings and InvestmentDokument16 SeitenRelationship Between GDP, Consumption, Savings and InvestmentBharath NaikNoch keine Bewertungen

- Suntrust Bank v. John H. Ruiz, 11th Cir. (2016)Dokument12 SeitenSuntrust Bank v. John H. Ruiz, 11th Cir. (2016)Scribd Government DocsNoch keine Bewertungen

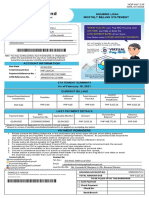

- Payment SlipDokument2 SeitenPayment SlipEmeka NkemNoch keine Bewertungen

- 05 Quiz 1Dokument2 Seiten05 Quiz 1ab galeNoch keine Bewertungen

- Annex Consolidated SpaDokument2 SeitenAnnex Consolidated Spamcjeff32Noch keine Bewertungen