Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Financial-Forecast AFN FinMgmt 13e BrighamDokument19 SeitenFinancial-Forecast AFN FinMgmt 13e BrighamRimpy SondhNoch keine Bewertungen

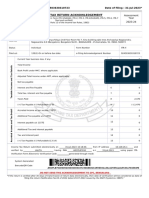

- Indian Income Tax Return Acknowledgement: Acknowledgement Number:924503630310723 Date of Filing: 31-Jul-2023Dokument1 SeiteIndian Income Tax Return Acknowledgement: Acknowledgement Number:924503630310723 Date of Filing: 31-Jul-2023bluetrans expressNoch keine Bewertungen

- Advanced Accounting Part 1 Dayag 2015 Chapter 8Dokument5 SeitenAdvanced Accounting Part 1 Dayag 2015 Chapter 8Killua Zoldyck67% (3)

- Sample of New Format of Audit Report IN BANKDokument17 SeitenSample of New Format of Audit Report IN BANKAmit Malshe0% (1)

- Income Tax Study MaterialDokument303 SeitenIncome Tax Study MaterialAbith Mathew77% (217)

- Creba v. Romulo Case DigestDokument2 SeitenCreba v. Romulo Case DigestApril Rose Villamor67% (6)

- Salary Slip (31837722 February, 2019) PDFDokument1 SeiteSalary Slip (31837722 February, 2019) PDFUsman AwanNoch keine Bewertungen

- Test Bank For Residential Construction Academy Plumbing 2nd EditionDokument24 SeitenTest Bank For Residential Construction Academy Plumbing 2nd Editionreginasaundersxwdcprtayb100% (40)

- Add or Drop Product DecisionsDokument6 SeitenAdd or Drop Product DecisionsksnsatishNoch keine Bewertungen

- China Fishery Group Limited: Rooms 3312-14, Hong Kong Plaza, 188 Connaught Road West, Hong KongDokument6 SeitenChina Fishery Group Limited: Rooms 3312-14, Hong Kong Plaza, 188 Connaught Road West, Hong Kongtungaas20011Noch keine Bewertungen

- 919e 2020-01-05 1578224820631Dokument10 Seiten919e 2020-01-05 1578224820631BrianHwang100% (1)

- Mohawk Carpet Corporation Dental/Vision PlanDokument32 SeitenMohawk Carpet Corporation Dental/Vision PlanvdkvaibhavNoch keine Bewertungen

- Managerial Accounting Chapter 1 ExercisesDokument3 SeitenManagerial Accounting Chapter 1 ExercisesAngelica Lorenz100% (2)

- Ifrs Gapp InfosysDokument21 SeitenIfrs Gapp Infosysashishsuman0% (1)

- Financial Management Assessment QuestionnaireDokument4 SeitenFinancial Management Assessment QuestionnaireJatin GoyalNoch keine Bewertungen

- Company Structure. Q1) A Company S Balance Sheet Shows The Following Capital StructureDokument6 SeitenCompany Structure. Q1) A Company S Balance Sheet Shows The Following Capital StructureDullah AllyNoch keine Bewertungen

- RMC No 23-2012 - Withholding of TaxesDokument7 SeitenRMC No 23-2012 - Withholding of TaxesJOHAYNIENoch keine Bewertungen

- Financial Ratio AnalysisDokument6 SeitenFinancial Ratio AnalysisSatishNoch keine Bewertungen

- TCDNDokument6 SeitenTCDNDiep NguyenNoch keine Bewertungen

- Form Jvat 409Dokument2 SeitenForm Jvat 409Suzanne BradyNoch keine Bewertungen

- ICDS - 3 Construction ContractsDokument13 SeitenICDS - 3 Construction Contractskavita.m.yadavNoch keine Bewertungen

- Auditibg Problems Purchase CommitmentDokument1 SeiteAuditibg Problems Purchase Commitmentnivea gumayagay0% (1)

- IFRS 16: The Leases Standard Is Changing: Are You Ready?Dokument16 SeitenIFRS 16: The Leases Standard Is Changing: Are You Ready?romNoch keine Bewertungen

- Exxon Mobil Corporation: Stock Report - December 04, 2020 - NYSE Symbol: XOM - XOM Is in The S&P 500Dokument9 SeitenExxon Mobil Corporation: Stock Report - December 04, 2020 - NYSE Symbol: XOM - XOM Is in The S&P 500garikai masawiNoch keine Bewertungen

- School Annual Gender and Development (Gad) Plan and Budget BP 400/ FY 20Dokument5 SeitenSchool Annual Gender and Development (Gad) Plan and Budget BP 400/ FY 20DAVID TITAN JR.Noch keine Bewertungen

- Orchid Hotel-An IntroductionDokument1 SeiteOrchid Hotel-An IntroductionSai VasudevanNoch keine Bewertungen

- CorpLiq Draft (Recovered)Dokument9 SeitenCorpLiq Draft (Recovered)Via Samantha de AustriaNoch keine Bewertungen

- 1 Session OneDokument6 Seiten1 Session OneHardik ShahNoch keine Bewertungen

- Introduction To Active Portfolio ManagementDokument31 SeitenIntroduction To Active Portfolio ManagementPooja AgarwalNoch keine Bewertungen

- HW - AFM - E7-25, E7-28, P7-42 - Kelompok 8Dokument7 SeitenHW - AFM - E7-25, E7-28, P7-42 - Kelompok 8swear to the skyNoch keine Bewertungen