Das könnte Ihnen auch gefallen

- Sample PMP Earned Value Questions ScenarioDokument13 SeitenSample PMP Earned Value Questions ScenarioAsfurix Mesfin100% (1)

- SolutionsDokument54 SeitenSolutionskarenNoch keine Bewertungen

- 2010 ERPStudy GuideDokument16 Seiten2010 ERPStudy GuideWinston Kasongo100% (1)

- Rothmueller MuseumDokument22 SeitenRothmueller MuseumAnonymous vlSlMI0% (1)

- Energy Finance and Economics: Analysis and Valuation, Risk Management, and the Future of EnergyVon EverandEnergy Finance and Economics: Analysis and Valuation, Risk Management, and the Future of EnergyBewertung: 5 von 5 Sternen5/5 (2)

- CH 04Dokument51 SeitenCH 04Quỳnh Anh Nguyễn TháiNoch keine Bewertungen

- CHP 4Dokument49 SeitenCHP 4Muhammad BilalNoch keine Bewertungen

- Risk Analysis and Exploration Economics - KjemperudDokument45 SeitenRisk Analysis and Exploration Economics - KjemperudSuta VijayaNoch keine Bewertungen

- ProbabilityDokument62 SeitenProbabilityMohit BholaNoch keine Bewertungen

- Petroleum Economic EvaluationDokument24 SeitenPetroleum Economic EvaluationSanjeev Singh NegiNoch keine Bewertungen

- Wasting Assets: ReferencesDokument7 SeitenWasting Assets: ReferencesMaeNoch keine Bewertungen

- BS Session 3-4Dokument56 SeitenBS Session 3-4SRINIVASNoch keine Bewertungen

- Review Class For Final Exam 2016, For Moodle, With SolutionDokument17 SeitenReview Class For Final Exam 2016, For Moodle, With SolutionMaxNoch keine Bewertungen

- IntroductionDokument28 SeitenIntroductionKai JieNoch keine Bewertungen

- Brilliants' ConventDokument9 SeitenBrilliants' ConventMayank GoelNoch keine Bewertungen

- 480505965study MaterialDokument162 Seiten480505965study Materialvishaljalan100% (1)

- 1-WK 04 - Lect 10 - LFA - IIDokument46 Seiten1-WK 04 - Lect 10 - LFA - IIguessNoch keine Bewertungen

- Property, Plant and Equipment - Wasting AssetsDokument42 SeitenProperty, Plant and Equipment - Wasting Assetstopakin09Noch keine Bewertungen

- Trimester 3Dokument14 SeitenTrimester 3Tanya MalikNoch keine Bewertungen

- Mefa Mid1 and Obj1 QP 1 Mar2022Dokument3 SeitenMefa Mid1 and Obj1 QP 1 Mar2022KishoreReddyNoch keine Bewertungen

- Planificación Minera: Introduction and Planning ProcessDokument35 SeitenPlanificación Minera: Introduction and Planning ProcessGustavo Salazar Fernandez100% (1)

- KV Guwahati Study MaterialDokument117 SeitenKV Guwahati Study MaterialSankar RanjanNoch keine Bewertungen

- CBSE Important QuestionsDokument87 SeitenCBSE Important QuestionsPrithvi ranaNoch keine Bewertungen

- Optimum Application of Geosciences in The Search For Hydrocarbon in Frontier Basins, Examples From SudanDokument23 SeitenOptimum Application of Geosciences in The Search For Hydrocarbon in Frontier Basins, Examples From SudanAnyak2014Noch keine Bewertungen

- Valuation of E&P Using Real Option ModelDokument22 SeitenValuation of E&P Using Real Option Modelsgabong100% (1)

- Managerial Economics and Financial AnalysisDokument53 SeitenManagerial Economics and Financial AnalysisManda Ramesh BabuNoch keine Bewertungen

- FR SD20 Examiner's ReportDokument21 SeitenFR SD20 Examiner's Reportngoba_cuongNoch keine Bewertungen

- Chapter 10Dokument36 SeitenChapter 10chiny0% (1)

- Dwnload Full Microeconomics Canadian 2nd Edition Hubbard Test Bank PDFDokument36 SeitenDwnload Full Microeconomics Canadian 2nd Edition Hubbard Test Bank PDFgoiteredumbonate.pykks100% (11)

- TTA2 Strategy Rev 1 Nov 2011Dokument28 SeitenTTA2 Strategy Rev 1 Nov 2011Eyoma EtimNoch keine Bewertungen

- Final Proposal 4Dokument15 SeitenFinal Proposal 4eyob yohannesNoch keine Bewertungen

- BBM 1121 Final Exam 2022 S1Dokument6 SeitenBBM 1121 Final Exam 2022 S1bonaventure chipetaNoch keine Bewertungen

- Chapter 18Dokument27 SeitenChapter 18jimmy_chou1314100% (1)

- 3 - Reserve Concepts & Field DevDokument67 Seiten3 - Reserve Concepts & Field DevMygroup 5544100% (2)

- Advanced Capital Budgeting-RawDokument34 SeitenAdvanced Capital Budgeting-Rawjohn3dNoch keine Bewertungen

- Test Bank For Intermediate Accounting 12th Edition Donald e KiesoDokument36 SeitenTest Bank For Intermediate Accounting 12th Edition Donald e Kiesoheatingbultow.ji9fo100% (46)

- Intermediate May 2011Dokument109 SeitenIntermediate May 2011Adesoye AyodejiNoch keine Bewertungen

- Economicsproject 180215173919Dokument28 SeitenEconomicsproject 180215173919Bhavya GoelNoch keine Bewertungen

- Overview: Production and Cost II: - Opportunity Costs in Practice - Example: Valuing A 1998 Boeing 737-700Dokument12 SeitenOverview: Production and Cost II: - Opportunity Costs in Practice - Example: Valuing A 1998 Boeing 737-700venuputtamrajuNoch keine Bewertungen

- Capital Budgeting For The Multinational CorporationDokument18 SeitenCapital Budgeting For The Multinational CorporationManish MahajanNoch keine Bewertungen

- CBSE Important Questions Class-11 Economics Chapter-1 Introduction To EconomicsDokument4 SeitenCBSE Important Questions Class-11 Economics Chapter-1 Introduction To EconomicsShraddha BansalNoch keine Bewertungen

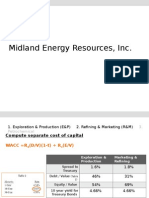

- Midland Energy Resources, IncDokument10 SeitenMidland Energy Resources, IncAnshulSharmaNoch keine Bewertungen

- Chapter 1Dokument25 SeitenChapter 1ebrahimnejad64Noch keine Bewertungen

- Test Bank For Macroeconomics Canadian 1St Edition Hubbard 0137022107 9780137022106 Full Chapter PDFDokument36 SeitenTest Bank For Macroeconomics Canadian 1St Edition Hubbard 0137022107 9780137022106 Full Chapter PDFwilliam.ortiz812100% (9)

- 3 - Mining Revenues and CostsDokument77 Seiten3 - Mining Revenues and CostsMayaraCarvalho100% (1)

- Present Worth Analysis: Gra W HillDokument25 SeitenPresent Worth Analysis: Gra W HillTarek TarekNoch keine Bewertungen

- Review Session - 28/04/2017: Question 2: The Following Information Is Available On A New Piece of EquipmentDokument4 SeitenReview Session - 28/04/2017: Question 2: The Following Information Is Available On A New Piece of Equipmentafsdasdf3qf4341f4asDNoch keine Bewertungen

- QM Session 4Dokument44 SeitenQM Session 4harherron123Noch keine Bewertungen

- CFA Secret Sauce QuintedgeDokument23 SeitenCFA Secret Sauce QuintedgejagjitbhaimbbsNoch keine Bewertungen

- 4 Days Exercises - Solutions - Ver 2.0Dokument13 Seiten4 Days Exercises - Solutions - Ver 2.0pranjal92pandeyNoch keine Bewertungen

- Quantitative StatisticsDokument40 SeitenQuantitative StatisticsUjjval YadavNoch keine Bewertungen

- B74 - Off Campus Assignment Schedule - Post C1Dokument5 SeitenB74 - Off Campus Assignment Schedule - Post C1Raja RajanNoch keine Bewertungen

- PGE 543 - Advanced Petroleum EconomicsDokument1 SeitePGE 543 - Advanced Petroleum Economicsمحمد بن اسحإقNoch keine Bewertungen

- NPV Irr MirrDokument7 SeitenNPV Irr MirrAida PekicNoch keine Bewertungen

- Thesis 1984R F928rDokument59 SeitenThesis 1984R F928rCindy Faye CrusanteNoch keine Bewertungen

- Gitman Test Bank CH - 12Dokument36 SeitenGitman Test Bank CH - 12Hazem TharwatNoch keine Bewertungen

- University of Calgary Haskayne School of BusinessDokument5 SeitenUniversity of Calgary Haskayne School of BusinessSisaxNoch keine Bewertungen

- The Investing Oasis: Contrarian Treasure in the Capital Markets DesertVon EverandThe Investing Oasis: Contrarian Treasure in the Capital Markets DesertNoch keine Bewertungen