Das könnte Ihnen auch gefallen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Sffli®: IlftsfDokument136 SeitenSffli®: Ilftsftakne_007Noch keine Bewertungen

- Qdoc - Tips - Sankaran Element of HomeopathyDokument546 SeitenQdoc - Tips - Sankaran Element of Homeopathytakne_007Noch keine Bewertungen

- A Case OF Cervical Spine InjuryDokument127 SeitenA Case OF Cervical Spine Injurytakne_007Noch keine Bewertungen

- Repertorization of The Totality of The SymptomsDokument3 SeitenRepertorization of The Totality of The Symptomstakne_007Noch keine Bewertungen

- Messages To AspirantsDokument123 SeitenMessages To Aspirantstakne_007Noch keine Bewertungen

- Venous Ulcer and Stasis Dermatitis Case SeriesDokument11 SeitenVenous Ulcer and Stasis Dermatitis Case Seriestakne_007Noch keine Bewertungen

- Nature: The " Electronic Reactions of Abrams."Dokument2 SeitenNature: The " Electronic Reactions of Abrams."takne_007Noch keine Bewertungen

- Mahatma Letters Volume IDokument213 SeitenMahatma Letters Volume Itakne_007Noch keine Bewertungen

- Chelidonim VS NuxvomDokument3 SeitenChelidonim VS Nuxvomtakne_007Noch keine Bewertungen

- StaphylococcinumDokument11 SeitenStaphylococcinumtakne_007Noch keine Bewertungen

- AyurvedaDokument67 SeitenAyurvedatakne_007Noch keine Bewertungen

- Advanced Case Taking in HomeopathyDokument11 SeitenAdvanced Case Taking in Homeopathytakne_007Noch keine Bewertungen

- Ayurvedamlo Sulabha Chickitsalu by DR GV PurnachanduDokument119 SeitenAyurvedamlo Sulabha Chickitsalu by DR GV Purnachandutakne_007Noch keine Bewertungen

- Quarterly Homoeopathic Digest Vol - Iii No - 3 September 1986 1. 2. 3Dokument17 SeitenQuarterly Homoeopathic Digest Vol - Iii No - 3 September 1986 1. 2. 3takne_007Noch keine Bewertungen

- Elia Kim - Organon OutlineDokument16 SeitenElia Kim - Organon Outlinetakne_007Noch keine Bewertungen

- Quarterly Homoeopathic DigestDokument15 SeitenQuarterly Homoeopathic Digesttakne_007Noch keine Bewertungen

- How Can Healthier Children Be BornDokument9 SeitenHow Can Healthier Children Be Borntakne_007Noch keine Bewertungen

- Dunham Taking The CaseDokument18 SeitenDunham Taking The Casetakne_007Noch keine Bewertungen

- Lung Exam DetailsDokument3 SeitenLung Exam Detailsdidutza91Noch keine Bewertungen

- Quarterly Homeopathic JournalDokument16 SeitenQuarterly Homeopathic Journaltakne_007100% (1)

- Registration1 PDFDokument1 SeiteRegistration1 PDFtakne_007Noch keine Bewertungen

- Geukens A. - 5000 Repertory Additions For SynthesisDokument9 SeitenGeukens A. - 5000 Repertory Additions For Synthesistakne_007Noch keine Bewertungen

- RADAR 10.x Update To 10.0.012Dokument6 SeitenRADAR 10.x Update To 10.0.012takne_007Noch keine Bewertungen

- Occult Significance HypnosisDokument53 SeitenOccult Significance Hypnosispresttige100% (4)

- Bonsai For Part Shade: Japanese Cedar. This Conifer Has TightDokument2 SeitenBonsai For Part Shade: Japanese Cedar. This Conifer Has Tighttakne_007Noch keine Bewertungen

- Mcgee-Vodou and Voodoo in SR PDFDokument28 SeitenMcgee-Vodou and Voodoo in SR PDFtakne_007Noch keine Bewertungen

- Ayurveda Panchakarma Keraleeya Panchakarmapdf PDFDokument9 SeitenAyurveda Panchakarma Keraleeya Panchakarmapdf PDFtakne_007Noch keine Bewertungen

- Bonsai by Brent WaltsonDokument5 SeitenBonsai by Brent WaltsonartlinefoxNoch keine Bewertungen

- Bonsai Winter Care in New EnglandDokument2 SeitenBonsai Winter Care in New Englandtakne_007Noch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Risk Latte - RAROC of A Corporate Loan - "Back of The Envelope" CalculationsDokument3 SeitenRisk Latte - RAROC of A Corporate Loan - "Back of The Envelope" CalculationsAshley JomyNoch keine Bewertungen

- HRM Strategies of SCBDokument52 SeitenHRM Strategies of SCBajish808Noch keine Bewertungen

- Monetary Policy & Its ImpactDokument23 SeitenMonetary Policy & Its ImpactHrishikesh DargeNoch keine Bewertungen

- Ferro Scrap Nigam LimitedDokument46 SeitenFerro Scrap Nigam LimitedIyyappadasan SubramanianNoch keine Bewertungen

- Solution Manual Financial Institution Management 3rd Edition by Helen Lange SLM1085Dokument8 SeitenSolution Manual Financial Institution Management 3rd Edition by Helen Lange SLM1085thar adelei100% (1)

- Retail Banking: by Prof Santosh KumarDokument30 SeitenRetail Banking: by Prof Santosh KumarSuraj KumarNoch keine Bewertungen

- Icici Bank Noc FormatDokument1 SeiteIcici Bank Noc Formatguiness_joe915463% (8)

- Contract To Sell Revised Feb 2022Dokument9 SeitenContract To Sell Revised Feb 2022Darwin LasinNoch keine Bewertungen

- New SFS Marketing Presentation SlidesDokument20 SeitenNew SFS Marketing Presentation SlidessarahNoch keine Bewertungen

- Cap 8Dokument26 SeitenCap 8Uver Jhon Terrones LeonNoch keine Bewertungen

- Anti-Money Laundering ActDokument8 SeitenAnti-Money Laundering ActKriztel CuñadoNoch keine Bewertungen

- Investigation Report TP017356Dokument41 SeitenInvestigation Report TP017356Bk Charles Ruppy100% (1)

- Barbara Etzel - Webster's Finance and Investment Dictionary-Wiley (2003)Dokument388 SeitenBarbara Etzel - Webster's Finance and Investment Dictionary-Wiley (2003)wayawid760Noch keine Bewertungen

- Administered Interest Rates in IndiaDokument17 SeitenAdministered Interest Rates in IndiatNoch keine Bewertungen

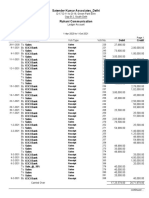

- Satender Kumar Associates - DelhiDokument7 SeitenSatender Kumar Associates - DelhiAVS & AssociatesNoch keine Bewertungen

- Materi Binal 6 The Global Capital MarketDokument27 SeitenMateri Binal 6 The Global Capital MarketNicholas ZiaNoch keine Bewertungen

- KOFAX - Five Case Studies To Inspire Your Intelligent Automation StrategyDokument22 SeitenKOFAX - Five Case Studies To Inspire Your Intelligent Automation StrategyShirinda PradeeptiNoch keine Bewertungen

- TD Bank Payment ContracDokument2 SeitenTD Bank Payment Contracshafa anisa ramadhaniNoch keine Bewertungen

- Cryptoassets: The Financial MetaverseDokument125 SeitenCryptoassets: The Financial MetaverseTom ChoiNoch keine Bewertungen

- Conceptual Frame WorkDokument62 SeitenConceptual Frame WorkKavyaNoch keine Bewertungen

- Q&aDokument70 SeitenQ&apaulosejgNoch keine Bewertungen

- Lapu-Lapu Foundation V CADokument2 SeitenLapu-Lapu Foundation V CAjasminealmiraNoch keine Bewertungen

- Gmail - Contact The BankDokument1 SeiteGmail - Contact The BankFira tubeNoch keine Bewertungen

- Artifact 5a - Guidelines For Filling PF Withdrawal Form TCS PDFDokument3 SeitenArtifact 5a - Guidelines For Filling PF Withdrawal Form TCS PDFDebmalya DuttaNoch keine Bewertungen

- 2021 Global Islamic Fintech Report 2021Dokument56 Seiten2021 Global Islamic Fintech Report 2021Slamet PrayitnoNoch keine Bewertungen

- PDFDokument386 SeitenPDFVic CajuraoNoch keine Bewertungen

- PS FSCM TablesDokument17 SeitenPS FSCM TablessivanblNoch keine Bewertungen

- Jesus TambuntingDokument5 SeitenJesus TambuntingheinzteinNoch keine Bewertungen

- Financial Acctg & Reporting 1 - CASE ANALYSIS SUMMARYDokument23 SeitenFinancial Acctg & Reporting 1 - CASE ANALYSIS SUMMARYJaquelyn ClataNoch keine Bewertungen

- Call Money Market in IndiaDokument37 SeitenCall Money Market in IndiaDivya71% (7)