Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Deutsche Bank QP1 InternshipsDokument20 SeitenDeutsche Bank QP1 Internshipszubezub100% (1)

- How To Identify Wide MoatsDokument18 SeitenHow To Identify Wide MoatsInnerScorecardNoch keine Bewertungen

- PNB v. GARCIA (2014) PDFDokument2 SeitenPNB v. GARCIA (2014) PDFcorky01Noch keine Bewertungen

- Dassault Systemes Vs DepDokument5 SeitenDassault Systemes Vs Depbharath289Noch keine Bewertungen

- Why Did ABC Fail at The Bank of ChinaDokument9 SeitenWhy Did ABC Fail at The Bank of ChinaZhang JieNoch keine Bewertungen

- Resulting TrustDokument34 SeitenResulting TrustAnonymous Azxx3Kp9Noch keine Bewertungen

- VP0630Dokument16 SeitenVP0630Anonymous 9eadjPSJNgNoch keine Bewertungen

- Peng - FM 1.Dokument28 SeitenPeng - FM 1.Aliya JamesNoch keine Bewertungen

- Commission on Elections QualificationsDokument197 SeitenCommission on Elections QualificationssamanthaNoch keine Bewertungen

- NKT/KS/17/4468: NXO-21328 1 (Contd.)Dokument3 SeitenNKT/KS/17/4468: NXO-21328 1 (Contd.)Namrata RamgadeNoch keine Bewertungen

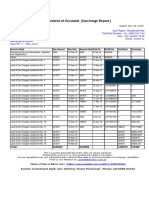

- Surcharge Report BTKSC-P05164Dokument1 SeiteSurcharge Report BTKSC-P05164Nasir Badshah AfridiNoch keine Bewertungen

- USD Credit Sensitive Rates For LIBOR Replacement Libor Sofr Bsby Crits Ameribor Bank Yield IndexDokument6 SeitenUSD Credit Sensitive Rates For LIBOR Replacement Libor Sofr Bsby Crits Ameribor Bank Yield IndexMohammad Abdul Latif TanveerNoch keine Bewertungen

- South Asialink Finance Corporation (Credit Union)Dokument1 SeiteSouth Asialink Finance Corporation (Credit Union)Charish Kaye Radana100% (1)

- Valuation Practices Survey 2013 v3Dokument36 SeitenValuation Practices Survey 2013 v3Deagle_zeroNoch keine Bewertungen

- 019 NEBOSH International General Certificate Course UK - Application FormDokument2 Seiten019 NEBOSH International General Certificate Course UK - Application FormArman Ul NasarNoch keine Bewertungen

- Budgeting, Standard Costing & Variance AnalysisDokument3 SeitenBudgeting, Standard Costing & Variance AnalysisHassanAbsarQaimkhaniNoch keine Bewertungen

- Scholtz 2016 AIChE - Journal PDFDokument12 SeitenScholtz 2016 AIChE - Journal PDFYaqoob AliNoch keine Bewertungen

- D3s3-Types of EnterprisesDokument35 SeitenD3s3-Types of Enterprisesrakesh19865Noch keine Bewertungen

- Tax Policy Assessment and Design in Support of Direct InvestmentDokument226 SeitenTax Policy Assessment and Design in Support of Direct InvestmentKate EloshviliNoch keine Bewertungen

- BAAE 12-BSAC 1B AssignmentDokument2 SeitenBAAE 12-BSAC 1B AssignmentjepsyutNoch keine Bewertungen

- DHFL Annual Report 2019-20Dokument292 SeitenDHFL Annual Report 2019-20hyenadogNoch keine Bewertungen

- REFUND DENIED FOR NON-REFUNDABLE TICKETSDokument12 SeitenREFUND DENIED FOR NON-REFUNDABLE TICKETSEzekiel Japhet Cedillo EsguerraNoch keine Bewertungen

- IFT Question Bank With Answer (Reading Wise) 2017Dokument848 SeitenIFT Question Bank With Answer (Reading Wise) 2017Michael Vilchez100% (10)

- TSDBF Answering Affidavit (Signed) 020919-OCRDokument147 SeitenTSDBF Answering Affidavit (Signed) 020919-OCRjillianNoch keine Bewertungen

- Quiz 1 CANVAS MANACCDokument26 SeitenQuiz 1 CANVAS MANACCMj GalangNoch keine Bewertungen

- Ficha 2Dokument4 SeitenFicha 2Elsa MachadoNoch keine Bewertungen

- BootcampX Day 2Dokument31 SeitenBootcampX Day 2Vivek LasunaNoch keine Bewertungen

- Combined Final VersionDokument84 SeitenCombined Final VersionDanudear DanielNoch keine Bewertungen

- Head of Finance Operations JD 130416Dokument4 SeitenHead of Finance Operations JD 130416Janani ParameswaranNoch keine Bewertungen

- Remittance Form for Overseas TransferDokument5 SeitenRemittance Form for Overseas TransferPrabhu KnNoch keine Bewertungen