Das könnte Ihnen auch gefallen

- SARFAESI Act Management of NPADokument4 SeitenSARFAESI Act Management of NPAsuchethatiaNoch keine Bewertungen

- BB Loan Classification and ProvisioningDokument16 SeitenBB Loan Classification and ProvisioningMuhammad Ali Jinnah100% (1)

- Loan ProvisioningDokument16 SeitenLoan ProvisioningrajmirakshanNoch keine Bewertungen

- BRPD Circular No. 14-2012 - Master Circular On Loan Classification and ProvisioningDokument16 SeitenBRPD Circular No. 14-2012 - Master Circular On Loan Classification and ProvisioningRifat Hasan Rathi100% (4)

- CCP - RBI - July-Dec 22Dokument19 SeitenCCP - RBI - July-Dec 22P N rajuNoch keine Bewertungen

- 503acf260214f PDFDokument16 Seiten503acf260214f PDFSiddhi KudalkarNoch keine Bewertungen

- Assignment: Export Financing System of BangladeshDokument8 SeitenAssignment: Export Financing System of BangladeshNafiz ImtiazNoch keine Bewertungen

- Understanding Non-Performing Assets in BanksDokument35 SeitenUnderstanding Non-Performing Assets in BanksMaridasrajanNoch keine Bewertungen

- Credit Management Overview and Principles of LendingDokument44 SeitenCredit Management Overview and Principles of LendingTavneet Singh100% (2)

- BRPD Circular No 05Dokument14 SeitenBRPD Circular No 05Iftekhar Ifte100% (1)

- Unit-2 Financial Crdit Risk AnalyticsDokument25 SeitenUnit-2 Financial Crdit Risk AnalyticsAkshitNoch keine Bewertungen

- NPAkjhhkjhkjhjhjDokument54 SeitenNPAkjhhkjhkjhjhjRintu AbrahamNoch keine Bewertungen

- Non Performing AssetsDokument11 SeitenNon Performing AssetssudheerNoch keine Bewertungen

- Indian Banks Cut NPAs to Lowest Since 2016Dokument44 SeitenIndian Banks Cut NPAs to Lowest Since 2016ParthNoch keine Bewertungen

- Non Performing AssetsDokument24 SeitenNon Performing AssetsAmarjeet DhobiNoch keine Bewertungen

- Credit Management Overview and Principles of LendingDokument55 SeitenCredit Management Overview and Principles of LendingShilpa Grover100% (4)

- RBI Guidelines on Joint Lenders' Forum and Corrective Action PlanDokument16 SeitenRBI Guidelines on Joint Lenders' Forum and Corrective Action Planonlynishank1934Noch keine Bewertungen

- Credit Team Report 1Dokument18 SeitenCredit Team Report 1Saugat DangalNoch keine Bewertungen

- Various Recovery Measures Adopted by Banks and Financial InstitutionsDokument19 SeitenVarious Recovery Measures Adopted by Banks and Financial InstitutionsjasmeetNoch keine Bewertungen

- Assignment of Management of Working Capital On Chore CommitteeDokument4 SeitenAssignment of Management of Working Capital On Chore CommitteeShubhamNoch keine Bewertungen

- Semester-III Comprehensive Examinations Class of 2009 SLBK605 - Overview of Banking Part-ADokument22 SeitenSemester-III Comprehensive Examinations Class of 2009 SLBK605 - Overview of Banking Part-AChandni BhargavaNoch keine Bewertungen

- BANKING ISSUESDokument17 SeitenBANKING ISSUESbhavyaNoch keine Bewertungen

- Presentation On NPA Problem: by Anshika AditiDokument18 SeitenPresentation On NPA Problem: by Anshika AditiAnshika SharmaNoch keine Bewertungen

- Impact of nationalisation on Indian banking sectorDokument4 SeitenImpact of nationalisation on Indian banking sectorAryan DevNoch keine Bewertungen

- Bank Assurance and Letter of CreditDokument4 SeitenBank Assurance and Letter of CreditRahul Kumar TantwarNoch keine Bewertungen

- Cbi So Model Paper 2022Dokument37 SeitenCbi So Model Paper 2022himanshu agrawalNoch keine Bewertungen

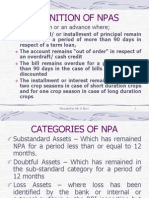

- Definition of Npas: A NPA Is A Loan or An Advance WhereDokument30 SeitenDefinition of Npas: A NPA Is A Loan or An Advance WheremulchandranaNoch keine Bewertungen

- Management of Non-Performing Assets: Presentation by Mr. S. RaviDokument29 SeitenManagement of Non-Performing Assets: Presentation by Mr. S. RaviRajesh MaddiNoch keine Bewertungen

- NPADokument6 SeitenNPA76-Gunika MahindraNoch keine Bewertungen

- Banking policy and structural changes e-magazineDokument22 SeitenBanking policy and structural changes e-magazineApurva JhaNoch keine Bewertungen

- File BRPD Circular No 05Dokument3 SeitenFile BRPD Circular No 05Arifur RahmanNoch keine Bewertungen

- Study on Factors Driving Non-Performing Assets in Indian BanksDokument85 SeitenStudy on Factors Driving Non-Performing Assets in Indian BanksAbhishek EraiahNoch keine Bewertungen

- RBI Master Circular Lending To Micro Small Medium Enterprises MSME Sector 2nd July 2012KALE LAW OFFICE CORPORATE LAWYER LAW FIR TAX CONSULTANTS COMPANY LAWYER 1Dokument7 SeitenRBI Master Circular Lending To Micro Small Medium Enterprises MSME Sector 2nd July 2012KALE LAW OFFICE CORPORATE LAWYER LAW FIR TAX CONSULTANTS COMPANY LAWYER 1Divya MewaraNoch keine Bewertungen

- RBI Governor On IBCDokument15 SeitenRBI Governor On IBCyashs-pgdm-2022-24Noch keine Bewertungen

- At Last Asset Management CompanyDokument3 SeitenAt Last Asset Management CompanyMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Plutus Ias Current Affairs Eng Med 25 Sep 2023Dokument7 SeitenPlutus Ias Current Affairs Eng Med 25 Sep 2023VikasNoch keine Bewertungen

- Mrunal Sir Latest 2020 Handout 3 PDFDokument19 SeitenMrunal Sir Latest 2020 Handout 3 PDFdaljit singhNoch keine Bewertungen

- 3EF1B - HDT - RBI3 - Burning - Issues - Banking - 2020B @ PDFDokument19 Seiten3EF1B - HDT - RBI3 - Burning - Issues - Banking - 2020B @ PDFMohan DNoch keine Bewertungen

- Summer Project Report: Loan AppraisalDokument36 SeitenSummer Project Report: Loan Appraisalchirag_ismNoch keine Bewertungen

- CCP Rbi Jul-Dec'23Dokument21 SeitenCCP Rbi Jul-Dec'23RaviTuduNoch keine Bewertungen

- Module-III Banking Regulation: Course OutlineDokument36 SeitenModule-III Banking Regulation: Course OutlineSanjay ParidaNoch keine Bewertungen

- Credit Report On MCBDokument16 SeitenCredit Report On MCBuzmabhatti34Noch keine Bewertungen

- What Are Non Performing Assets?Dokument9 SeitenWhat Are Non Performing Assets?Rizul96 GuptaNoch keine Bewertungen

- Dec 242015 FSD 01 eDokument3 SeitenDec 242015 FSD 01 eRaquibul HasanNoch keine Bewertungen

- Short Term LoansDokument4 SeitenShort Term LoansHarsh MehtaNoch keine Bewertungen

- Common Guidelines For Priority Sector AdvancesDokument43 SeitenCommon Guidelines For Priority Sector AdvancesKeval PatelNoch keine Bewertungen

- NPA Recovery ManagementDokument31 SeitenNPA Recovery ManagementSantoshi AravindNoch keine Bewertungen

- Bangladesh's Financial System and Central Banking PoliciesDokument10 SeitenBangladesh's Financial System and Central Banking PoliciesMohammad ShoaibNoch keine Bewertungen

- Sap Id: Roll No: Open Book - Through Blackboard Learning Management SystemDokument4 SeitenSap Id: Roll No: Open Book - Through Blackboard Learning Management SystemAkshita ShrivastavaNoch keine Bewertungen

- Guidelines for settling bank dues through Lok AdalatsDokument3 SeitenGuidelines for settling bank dues through Lok AdalatsMahesh Prasad PandeyNoch keine Bewertungen

- CMPCir1656 12Dokument95 SeitenCMPCir1656 12sunilNoch keine Bewertungen

- Financial Statements-2021Dokument137 SeitenFinancial Statements-2021Fakhrul AlamNoch keine Bewertungen

- Banking RegulationsDokument44 SeitenBanking RegulationsAnkith BNoch keine Bewertungen

- Weekly Economic Round Up 37Dokument11 SeitenWeekly Economic Round Up 37Mana PlanetNoch keine Bewertungen

- 2631IIBF Vision January 2013Dokument8 Seiten2631IIBF Vision January 2013Sukanta DasNoch keine Bewertungen

- 22MC894E2203DDDF4E0ABCA714DCE21F8F6CDokument63 Seiten22MC894E2203DDDF4E0ABCA714DCE21F8F6Caspimpale1999Noch keine Bewertungen

- Bank Promotion Interview - 2023Dokument79 SeitenBank Promotion Interview - 2023kumar Raushan RatneshNoch keine Bewertungen

- Public Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesVon EverandPublic Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesNoch keine Bewertungen

- Financing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesVon EverandFinancing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesNoch keine Bewertungen

- WSO 2022 IB Working Conditions SurveyDokument42 SeitenWSO 2022 IB Working Conditions SurveyPhạm Hồng HuếNoch keine Bewertungen

- Poverty and Crime PDFDokument17 SeitenPoverty and Crime PDFLudwigNoch keine Bewertungen

- Notice: Use of Segways® and Similar Devices by Individuals With A Mobility Impairment in GSA-Controlled Federal FacilitiesDokument2 SeitenNotice: Use of Segways® and Similar Devices by Individuals With A Mobility Impairment in GSA-Controlled Federal FacilitiesJustia.comNoch keine Bewertungen

- Immune System Quiz ResultsDokument6 SeitenImmune System Quiz ResultsShafeeq ZamanNoch keine Bewertungen

- HVDC BasicDokument36 SeitenHVDC BasicAshok KumarNoch keine Bewertungen

- SVIMS-No Que-2Dokument1 SeiteSVIMS-No Que-2LikhithaReddy100% (1)

- Workplace Hazard Analysis ProcedureDokument12 SeitenWorkplace Hazard Analysis ProcedureKent Nabz60% (5)

- Chemical and Physical Properties of Refined Petroleum ProductsDokument36 SeitenChemical and Physical Properties of Refined Petroleum Productskanakarao1Noch keine Bewertungen

- Perforamance Based AssessmentDokument2 SeitenPerforamance Based AssessmentJocelyn Acog Bisas MestizoNoch keine Bewertungen

- Abortion and UtilitarianismDokument4 SeitenAbortion and UtilitarianismBrent Harvey Soriano JimenezNoch keine Bewertungen

- SCE Research Paper PDFDokument12 SeitenSCE Research Paper PDFmuoi2002Noch keine Bewertungen

- Material Handling EquipmentsDokument12 SeitenMaterial Handling EquipmentsRahul SheelavantarNoch keine Bewertungen

- Space Analysis in Orthodontic: University of GlasgowDokument16 SeitenSpace Analysis in Orthodontic: University of GlasgowNizam Muhamad100% (1)

- LPBP HPSU Document PDFDokument131 SeitenLPBP HPSU Document PDFGanga PrasadNoch keine Bewertungen

- EP Series User Manual PDFDokument40 SeitenEP Series User Manual PDFa.elwahabNoch keine Bewertungen

- Model Fs CatalogDokument4 SeitenModel Fs CatalogThomas StempienNoch keine Bewertungen

- Life Overseas 7 ThesisDokument20 SeitenLife Overseas 7 ThesisRene Jr MalangNoch keine Bewertungen

- Philippines implements external quality assessment for clinical labsDokument2 SeitenPhilippines implements external quality assessment for clinical labsKimberly PeranteNoch keine Bewertungen

- Request For Review FormDokument11 SeitenRequest For Review FormJoel MillerNoch keine Bewertungen

- Formularium ApotekDokument12 SeitenFormularium ApotekNurul Evi kurniatiNoch keine Bewertungen

- Chapter 5Dokument16 SeitenChapter 5Ankit GuptaNoch keine Bewertungen

- Stress and FilipinosDokument28 SeitenStress and FilipinosDaniel John Arboleda100% (2)

- TS4-F - Fire SafetyDokument2 SeitenTS4-F - Fire SafetyDominic SantiagoNoch keine Bewertungen

- Week 6 Blood and Tissue FlagellatesDokument7 SeitenWeek 6 Blood and Tissue FlagellatesaemancarpioNoch keine Bewertungen

- Health and Safety Awareness For Flower Farm WorkersDokument1 SeiteHealth and Safety Awareness For Flower Farm WorkersGerald GwambaNoch keine Bewertungen

- Cellular Basis of HeredityDokument12 SeitenCellular Basis of HeredityLadyvirdi CarbonellNoch keine Bewertungen

- C. Drug Action 1Dokument28 SeitenC. Drug Action 1Jay Eamon Reyes MendrosNoch keine Bewertungen

- Insects, Stings and BitesDokument5 SeitenInsects, Stings and BitesHans Alfonso ThioritzNoch keine Bewertungen

- HTM 2025 2 (New) Ventilation in HospitalsDokument123 SeitenHTM 2025 2 (New) Ventilation in HospitalsArvish RamseebaluckNoch keine Bewertungen

- 2.assessment of Dental Crowding in Mandibular Anterior Region by Three Different MethodsDokument3 Seiten2.assessment of Dental Crowding in Mandibular Anterior Region by Three Different MethodsJennifer Abella Brown0% (1)