Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Merrill Lynch - Assessing Cost of Capital and Performance 2015Dokument16 SeitenMerrill Lynch - Assessing Cost of Capital and Performance 2015CommodityNoch keine Bewertungen

- The Sagicor Sigma Global Funds Salary Deduction FormDokument1 SeiteThe Sagicor Sigma Global Funds Salary Deduction FormRobyn MacNoch keine Bewertungen

- Bernanke - 1983 - Non-Monetary Effects of The Financial Crisis in The Propagation of The Great DepressionDokument21 SeitenBernanke - 1983 - Non-Monetary Effects of The Financial Crisis in The Propagation of The Great Depressionyezuh077Noch keine Bewertungen

- AS310 Midterm Test Sep Dec2021 PDFDokument1 SeiteAS310 Midterm Test Sep Dec2021 PDFGhetu MbiseNoch keine Bewertungen

- Formation of Joint Stock CompanyDokument5 SeitenFormation of Joint Stock CompanyHemchandra PatilNoch keine Bewertungen

- Scope of Livestock InsuranceDokument16 SeitenScope of Livestock InsuranceAjaz HussainNoch keine Bewertungen

- PRACTICAL ACCOUNTING 1 Part 2Dokument9 SeitenPRACTICAL ACCOUNTING 1 Part 2Sophia Christina BalagNoch keine Bewertungen

- Assignment On Financial StatementDokument11 SeitenAssignment On Financial StatementHamza IqbalNoch keine Bewertungen

- The Garden PlaceDokument2 SeitenThe Garden Placeaayushi dubeyNoch keine Bewertungen

- Mirae Asset Equity Allocator Fund of FundDokument26 SeitenMirae Asset Equity Allocator Fund of FundAdityaNarayanSinghNoch keine Bewertungen

- The Red-Bearded BaronDokument6 SeitenThe Red-Bearded BaronSarith Sagar100% (2)

- Chapter 9 Accounting Cycle of A Service BusinessDokument59 SeitenChapter 9 Accounting Cycle of A Service BusinessArlyn Ragudos BSA1Noch keine Bewertungen

- Fake - Fake Money Fake Teachers Fake Assets Robert Kiyosaki Book Novel by WWW - Indianpdf.com - Download PDF Online Free 21 30Dokument10 SeitenFake - Fake Money Fake Teachers Fake Assets Robert Kiyosaki Book Novel by WWW - Indianpdf.com - Download PDF Online Free 21 30hfxNoch keine Bewertungen

- Lia Lafico Laico ZawyaDokument4 SeitenLia Lafico Laico Zawyaapi-13892656Noch keine Bewertungen

- Great Canadian Debt Relief Inc - GCDR - GC DebtDokument4 SeitenGreat Canadian Debt Relief Inc - GCDR - GC DebtGC DebtNoch keine Bewertungen

- Abm 12 Fabm2 q1 Clas1 Elements of Sci v8 - Rhea Ann NavillaDokument13 SeitenAbm 12 Fabm2 q1 Clas1 Elements of Sci v8 - Rhea Ann NavillaKim Yessamin MadarcosNoch keine Bewertungen

- Anti-Money Laundering Disclosures and Banks' PerformanceDokument14 SeitenAnti-Money Laundering Disclosures and Banks' PerformanceLondonNoch keine Bewertungen

- RCA Study - Wilbur Smith Traffic & Revenue Forecasts - 012712Dokument103 SeitenRCA Study - Wilbur Smith Traffic & Revenue Forecasts - 012712Terry MaynardNoch keine Bewertungen

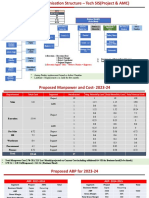

- Proposed Org Chart - Tech SIS.Dokument5 SeitenProposed Org Chart - Tech SIS.Santosh KumarNoch keine Bewertungen

- Your Serene Air Receipt - ZFZQU8Dokument3 SeitenYour Serene Air Receipt - ZFZQU8Farrukh Jamil0% (1)

- The Guide To Worry Free Investing VectorvestDokument10 SeitenThe Guide To Worry Free Investing VectorvestDdasfda DsafasdfNoch keine Bewertungen

- Bill Ackman's Letter On General GrowthDokument8 SeitenBill Ackman's Letter On General GrowthZoe GallandNoch keine Bewertungen

- Tata Motors Abridged LOF - Vfinal PDFDokument88 SeitenTata Motors Abridged LOF - Vfinal PDFdhanoj6522100% (1)

- LIberty Power Tech - RR - 74 - 10861 - 10-Nov-22Dokument5 SeitenLIberty Power Tech - RR - 74 - 10861 - 10-Nov-22Kristian MacariolaNoch keine Bewertungen

- Appoinment Letter Gram Sevika 0Dokument6 SeitenAppoinment Letter Gram Sevika 0Deepak PatelNoch keine Bewertungen

- What Is BudgetDokument4 SeitenWhat Is BudgetDhanvanthNoch keine Bewertungen

- Products of H&M, GE and Even Samsung Are "Made in Ethiopia"Dokument10 SeitenProducts of H&M, GE and Even Samsung Are "Made in Ethiopia"FuadNoch keine Bewertungen

- Sn53sup 20170430 001 2200147134Dokument2 SeitenSn53sup 20170430 001 2200147134Henry LowNoch keine Bewertungen

- Analysis of Annual Report:: AbstractDokument6 SeitenAnalysis of Annual Report:: Abstractapi-301617324Noch keine Bewertungen