Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Sip Project ReportDokument29 SeitenSip Project ReportAAKIB HAMDANINoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- List of Largest Banks in The United States - WikipediaDokument5 SeitenList of Largest Banks in The United States - WikipedialdNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Pakistan's Major Banks and Financial InstitutionsDokument24 SeitenPakistan's Major Banks and Financial Institutionskhizrajamal000Noch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- PassbookDokument128 SeitenPassbookArvind MalviyaNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Expenses Tracker 2022 Peter WafulaDokument50 SeitenExpenses Tracker 2022 Peter Wafulafrank obimoNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Statement 028201000028352Dokument6 SeitenStatement 028201000028352Saravanan 75Noch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Vinayak Pandla Nbs (Bank of Baroda)Dokument19 SeitenVinayak Pandla Nbs (Bank of Baroda)Vinayak PandlaNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Banking Financial Institutions By: Jessica Ong: 1. Define Central BankDokument5 SeitenBanking Financial Institutions By: Jessica Ong: 1. Define Central BankJessica Cabanting OngNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Bank Statement SummaryDokument24 SeitenBank Statement SummaryRanjith Kumar ANoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- Commercial BanksDokument8 SeitenCommercial BanksEdwin NyamohNoch keine Bewertungen

- Evolution of Central Banking in IndiaDokument15 SeitenEvolution of Central Banking in Indiapaisa321Noch keine Bewertungen

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument17 SeitenStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePrasanta BarmanNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- BFSI Sector ReportDokument33 SeitenBFSI Sector ReportSAGAR VAZIRANINoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Oblicon CasesDokument1 SeiteOblicon CasesRenzo JamerNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Complete Banking, Financial & Economic Awareness PDFDokument86 SeitenComplete Banking, Financial & Economic Awareness PDFAbhishek RawatNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Routing CodesDokument14 SeitenRouting CodesParag PenkerNoch keine Bewertungen

- Payment ConfirmationDokument1 SeitePayment ConfirmationsipkatNoch keine Bewertungen

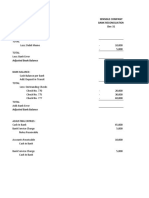

- Sensible Company Bank Reconciliation Dec-31Dokument8 SeitenSensible Company Bank Reconciliation Dec-31OwO OwONoch keine Bewertungen

- Plan Contable EmpresarialDokument432 SeitenPlan Contable EmpresarialJhamil Nirek PascasioNoch keine Bewertungen

- VIJAYA BANK ACCOUNT STATEMENT FOR TECHOPTIONS INFOSOLUTIONS PVT. LTDDokument7 SeitenVIJAYA BANK ACCOUNT STATEMENT FOR TECHOPTIONS INFOSOLUTIONS PVT. LTDVivek PatilNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Allahabad Bank Headquarters and HistoryDokument4 SeitenAllahabad Bank Headquarters and HistoryAmit RanjanNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- 1503XXXXXXXXX006412 12 2022Dokument5 Seiten1503XXXXXXXXX006412 12 2022Prem PanigrahiNoch keine Bewertungen

- Suku Bunga DepositoDokument3 SeitenSuku Bunga DepositoStfs Itu AkuNoch keine Bewertungen

- UAE Banks Swift CodesDokument10 SeitenUAE Banks Swift CodesakatariyaNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- 1542447415479Dokument7 Seiten1542447415479LogeshNoch keine Bewertungen

- Imp Key Indicators of RRBs 2013Dokument6 SeitenImp Key Indicators of RRBs 2013Pankaj SharmaNoch keine Bewertungen

- Nefteft MICR CodesDokument1.192 SeitenNefteft MICR CodesDeepesh DivakaranNoch keine Bewertungen

- Stipulation and Order of Discontinuance by KBC Investments Cayman Islands V Ltd.Dokument5 SeitenStipulation and Order of Discontinuance by KBC Investments Cayman Islands V Ltd.Thierry DebelsNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- N LOcsjr 27 NYUUCobDokument11 SeitenN LOcsjr 27 NYUUCobSANTOSH TRAVELSNoch keine Bewertungen

- Read The Following News Report and Answer Q. 1-4 On The Basis of The Same: (Case Based Question)Dokument4 SeitenRead The Following News Report and Answer Q. 1-4 On The Basis of The Same: (Case Based Question)Aditya BangreNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)